Image © Pound Sterling Live.

The Dollar is forecast to make further gains against the Euro by two leading Scandinavian banking names, which if correct suggests a recent fall below 1.15 in EUR/USD will be an enduring one.

Both Danske Bank and Swedbank have this week updated clients with their predictions for the Euro to Dollar exchange rate (EUR/USD) and they share a consensus view held by foreign exchange analysts that the Dollar's run of strength can extend further.

Swedbank strategist Anders Eklöf says the Dollar is to appreciate in value on solid economic growth as the drag from the delta variant fades and positive yield differentials vs. many G10 peers offer support.

DNB's FX Analyst Ingvild Borgen says "the spread between USD and EUR interest rates could continue to rise, favouring a further drop in the EURUSD going forward."

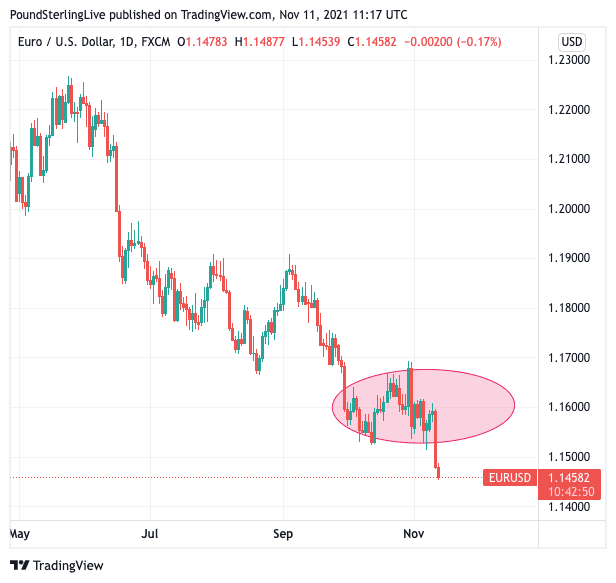

The calls come amidst another leg lower in the EUR/USD to 1.1466 on Thursday, November 11, which represents the exchange rate's lowest level since July 21, 2020.

The decline keeps alive a downtrend that has been intact since May and undermines suggestions that the pair was setting itself up for a rebound having consolidated around the 1.1550-1.1650 level during October and through to early November.

Above: Recent consolidation annotated on the EUR/USD daily chart.

- EUR/USD reference rates at publication:

Spot: 1.1458 - High street bank rates (indicative band): 1.1057-1.1137

- Payment specialist rates (indicative band): 1.1355-1.1400

- Find out about specialist rates, here

- Or, set up an exchange rate alert, here

The Dollar brought an end to this consolidation on November 10 when data showed U.S. inflation for September was much higher than anticipated, placing renewed pressure on the Federal Reserve to consider speeding up the pace at which it ends quantitative easing.

Expectations for a rate hike in the first half of 2022 have only been emboldened by the data, and this is reflected in a stronger Dollar.

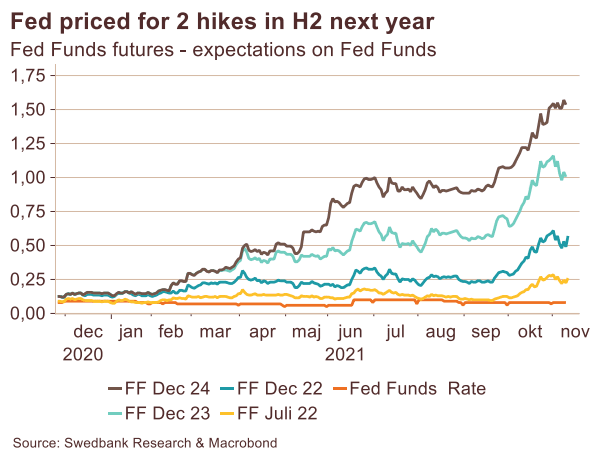

"Net bond buying finishes in June but it could go faster if needed. Fed chair Powell has not pushed back at market rate expectation of a hike already next summer followed by another hike in Q4. Our guess is that median dots in December will reflect 2 hikes next year rather than the current one," says Eklöf.

Swedbank's economists anticipate the maximum employment and slack in the U.S. labour market is lower than Fed has anticipated.

"If so, rates will need to be raised sooner rather than later and USD will benefit," says Eklöf.

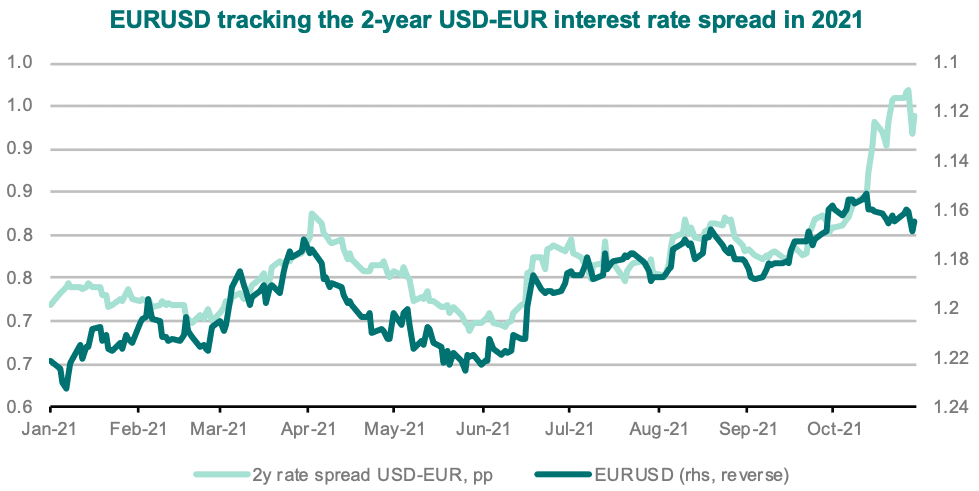

"Unlike in 2020, differences in interest rates have become a more forceful driver of currency markets in 2021," says Borgen. "We expect them to remain important going forward."

DNB Markets find the spread between 2-year USD swap rates and equivalent EUR rates have risen by around 20 basis points.

They find EUR/USD has tracked the moves in the 2-year interest rate spread closely for most of the year.

"We think the spread between USD and EUR interest rates could continue to widen," says Borgen.

Image courtesy of DNB Markets.

"The main reason we think the USD/EUR rate spread should continue to widen is that we see very limited room for EUR rates to rise," says DNB's Borgen. "We think investors have gone too far in pricing in that the ECB will hike interest rates next year".

Swedbank says the European Central Bank (ECB) is unlikely to be a source of support in the near- and medium-term, amidst evidence interest rates will remain near record lows for a protracted period.

Furthermore, the Eurozone looks particularly vulnerable to energy price squeezes as well as a slowdown in China, meanwhile a surge in coronavirus cases in Western Europe poses near-term headwinds.

Swedbank say they expect "the EUR to remain an underperformer in G10" as a result.

Key headwinds to the single-currency include:

1) supply disruptions in the manufacturing sector

2) weaker export demand from China

3) the rise in energy prices

4) rising Covid cases and the introduction of partial restrictions (Germany is seeing new records in daily cases).

DNB's new Euro to Dollar forecast sees a fall to 1.15 in 3 months and to 1.13 in 12 months (previous forecasts were 1.17 and 1.16, respectively).

Swedbank forecast a a move to 1.14 in 3 months, 1.12 in 6 months and 1.12 in 12 months.