© Pound Sterling Live

- EUR rises as trade tensions ease following Trump comments.

- Gains come despite German data confirming recession threat.

- Absence of EUR depreciation is a growing headache for ECB.

- Made worse by CNH weakness lifting the trade-weighted EUR.

- All eyes on White House and September ECB rate decision.

The Euro advanced against the Dollar and other rivals Tuesday even after official data confirmed the German economy is at risk of falling into recession, and the resilience of the currency is now a headache that could eventually see the European Central Bank (ECB) attempt to push it lower.

Euro gains were fractional Tuesday and came as investors sold safe-haven assets in favour of riskier alternatives after President Donald Trump claimed on Monday that he's made progress in trade talks with China, which soothed nerves in the market.

Nerves were frayed late last week the trade war between the world's two largest economies escalated again, but China has since disputed that any progress is being made. That could be bad news for the troubled German economy.

"The markets are back in repair mode again after policymakers played nice at the G7. We still think this backdrop relies on sentiment and positioning than any real progress in the trade wars. Given the recent escalation from China, we suspect that the US will need to make concessions to support a meaningful recovery. That's unlikely, increasing the prospects of renewed stress," says Mark McCormick, head of FX strategy at TD Securities.

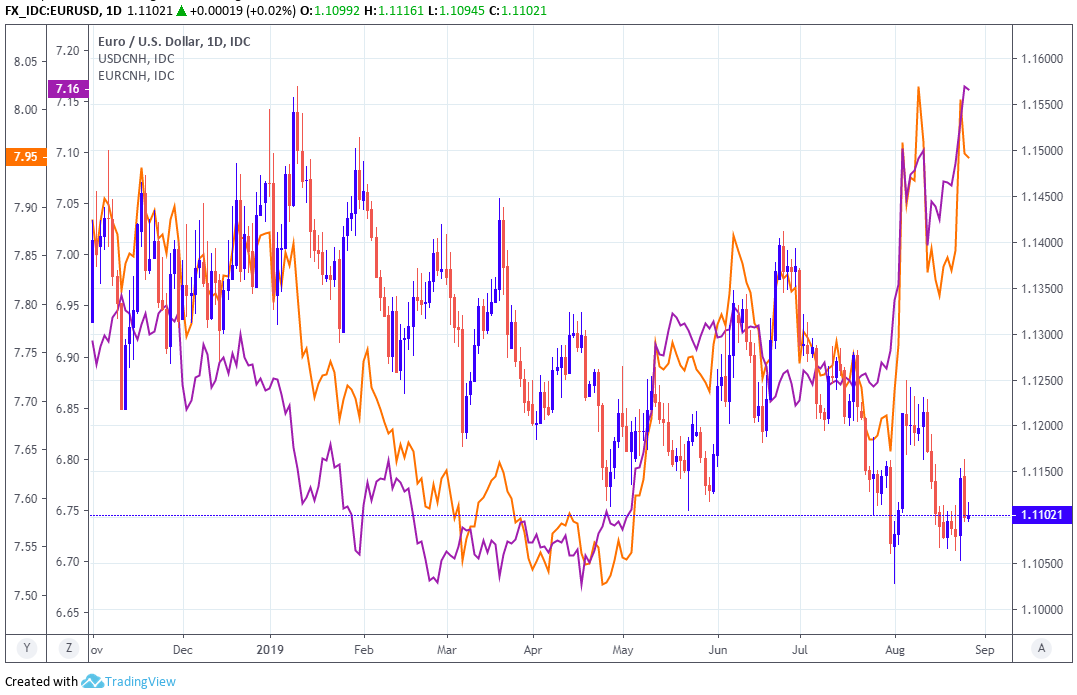

Above: EUR/USD at 4-hour intervals, with EUR/CNH (orange line, left axis) and USD/CNH (purple).

German growth fell by 0.1% in the second quarter due to a steep reduction in exports, according to the first detailed breakdown of preliminary figures released by Destatis. That's down from 0.4% previously and was enough to reduce annual growth in the year to the end of June to just 0.4%.

Exports fell 1.3% while imports declined by a lesser 0.3%, as demand for German products was crimped by the trade war that's hurting both the Chinese and global economies. Tuesday's figures came hard on the heels of the August Ifo survey, which echoed the recent tone of ECB President Mario Draghi when he said in July the outlook for the economy is getting "worse and worse".

The institute said Monday "there are ever more indications of a recession in Germany.". This was after its monthly survey of more than 7,000 companies showed current economic conditions falling to their lowest level since 2012 when represented in numerical format as an index. Companies also became more pessimistic in their outlook for the next six months, which is a similar message to that given off by the ZEW a fortnight earlier.

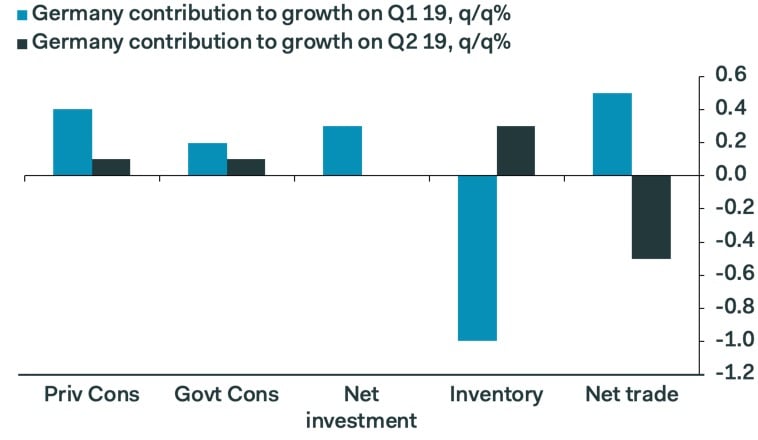

"Sharp slowdowns in investment, consumers’ spending, and a plunge in net exports, were the primary drivers of the hit to Germany’s economy in Q2. Personal consumption rose by just 0.1% quarter-on-quarter, down from revised 0.8% increase in Q1, while capital investment fell outright," says Claus Vistesen, chief Eurozone economist at Pantheon Macroeconomics. "Looking ahead, the IFO suggests that the economy is now in recession."

Above: Pantheon Macroeconomics graph showing positive and negative contributions to growth.

Germany's manufacturers bet big on the Chinese market in a range of areas during recent years, but particularly the luxury car market, and the world's second largest economy is now on its back foot following more than a year of trade conflict with the U.S.

China exports more than $550 bn of goods to the U.S. each year but around half those now incur tariffs of 25% when imported into the country and by December 15, all of them will be subject to at least a 15% tariff and others a 30% levy. U.S. tariffs are hurting China's domestic economy and in turn, crimping demand for German goods.

This is driving a slowdown in growth at a time when the ECB needs a strong economy if it is to see inflation back up at the target of "close to, but below 2%". The bank said last month that it's asked staff to devise a way of cutting interest rates further below zero without hurting an already-weak banking sector.

"Has Germany already fallen into recession?" asks Holger Schmieding, chief economist at Berenberg. "The renewed escalation of the US-Chinese trade war, the Brexit turmoil, declining survey and sentiment indicators and the ongoing drop in manufacturing orders (-6.9% yoy excluding bulk orders in Q2) point to a weaker result for 2H 2019. Abstracting from potential short-term distortions, we thus expect stagnation in quarterly GDP in Q3 and Q4 2019, with an almost 50% risk of a mild contraction."

Above: EUR/USD at daily intervals, with EUR/CNH (orange line, left axis) and USD/CNH (purple).

With Germany's economy already having contracted once in 2019, fears are now that third quarter data due will reveal another contraction for the third quarter, which would put the Eurozone's economic engine into a 'technical recession'. Those fears were already elevated even before the U.S.-China trade war escalated again in August and are now widely expected to draw a significant policy response from the European Central Bank in September.

However, and despite the fire newsflow, the Euro-to-Dollar rate has fallen by less than 1% in the last three months and is down only 3% for 2019, which some say is the bank is close to running out of monetary policy bullets it can fire. The ECB already cut interest rates below zero and has bought nearly a third of the European bond market since 2015 in the hope of lifting inflation by stimulating the economy with lower borrowing costs.

"So far, EUR/USD has barely changed while USD/CNY has risen, the result being that EUR/CNY is going up and the Euro's trade-weighted value likewise. That's just making the ECB's life even more difficult," says Kit Juckes, chief FX strategist at Societe Generale.

Above: Societe Generale graph showing Euro rising in trade-weighted terms, wih key EUR/CNY rate.

Recent price action is now threatening to make the German, Eurozone and ECB's collective headache even worse because the Euro is strengthening against the Chinese currency and has not weakened meaningfully relative to the Dollar. This is making German products more expensive for now-struggling Chinese consumers to buy while reducing the Eurozone's already-weak inflation pulse by making imports less costly for Europeans to buy.

The ECB needs faster growth and higher inflation if it is to deliver on its statutory mandate, but a Euro that's resisting further losses even in the face of an intensifying trade conflict and global economic downturn would only ever deliver the opposite of those things. This is partly why Olli Rehn, head of The Bank of Finland and an influential voice at the ECB, called recently for it bank to deliver a 'shock and awe' style package of stimulus measures in September.

"Our fundamental bias in GBPUSD and EURUSD is still to fade instances of strength, but we'd probably stay away from GBPUSD for now and instead focus solely on the 1.1150/1.1050 range in EURUSD," says Stephen Gallo, European head of FX strategy at BMO Capital Markets.

Above: EUR/USD at weekly intervals, with EUR/CNH (orange line, left axis) and USD/CNH (purple).

The Euro fell nearly 10% between August 2014 and January 2015 as markets ancticipated the stimulus program that saw the ECB begin buying European bonds and eventually took the rate it pays commercial lenders on their reserves below zero, which means it now charges them to park money with it.

Market perceptions that the bank can't physically do any more improve the condition of the economy explain the Euro's resilience this time around, as well as why the ECB might be particularly likely to at least attempt to over-deliver against market expectations when it announces its next monetary policy decision on Thursday, 12 September.

"We expect EURUSD to bottom out despite the escalating trade tensions and rising uncertainty about the global economic outlook. Reasons remain manifold. First, current investor positioning as mentioned above. Second, the Fed can ease policy far more than the ECB. Third, there is always the risk that the US systematically weakens the USD in order to prevent a strong greenback from hurting the domestic economy," says Thomas Flury, a strategist at UBS Global Wealth Management.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement