- GBP/EUR has fallen back into the middle of a multi-month range at 1.1350

- Main release for the Pound in week ahead is April PMI data

- Euro could see movment from April Inflation and GDP data

© DragonImages, Adobe Stock

Disappointment with the economy's growth rate impacted negatively on Pound Sterling in the previous week.

After peaking at 1.1599, GBP/EUR pulled back down sharply into the middle of its long-term range where it is currently trading at circa 1.1350.

The descending sequence of peaks and troughs clearly shown on the chart of 4hr time periods below argues that the short-term trend is probably down, and therefore more likely to continue lower than not.

The problem for bears is that there is a lot of chart support lying right under the current spot price which is likely to impede downside progress.

To start with the monthly pivot (PP) at 1.1348 is likely to present a tough obstacle to the downtrend. Pivots are levels on charts where price action often stalls, rotates or even reverses. There is a risk, therefore, that PP might cause the downtrend to reverse.

Another indication that the short-term downtrend may be running out of steam is the shape of the pattern the market has formed since peaking, which looks like an abcd pattern (outlined in red on the chart above).

Usually legs a-b and c-d are of similar length, which means c-d probably does not have much further to go and could end at 1.1295. Once it finishes the market will probably rotate and start moving higher, as shown in the example of an abcd on GBP/JPY below. This suggests the possibility of a reversal occurring at 1.1295, which is not far below the current spot price.

(Image courtesy of DailyFx)

These countertrend indicators make us cautious about expecting further downside even though the short-term trend is technically bearish. We have represented the risks to the downtrend as an orange box with hatching on the 4hr GBP/EUR chart above and labeled it 'support zone'. A further impediment to expecting more downside is the 200-day MA at 1.1260.

Due to the contradiction of the short-term trend and the many obstacles to its extension, we think it on balance prudent to withhold a forecast this week and wait to see how the market evolves.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Data and Events for the Pound

The main data release for the Pound in the week ahead will be the release of April Service and Manufacturing PMIs out at 9.30 on Thursday and Tuesday respectively.

PMI is short for Purchasing Manager Index, and PMIs are survey-based indicators which are seen as useful forward-indicators of economic activity. The market consensus appears to be for expecting a rebound in Services in April after the drop in March, which was put down, mainly to bad weather. Services PMI in April is expected to rise to 53.5 from 51.7 and Manufacturing to 54.8 from 55.1.

The Pound may be especially sensitive to the results this week owing to the lazer-like focus currency markets are currently placing on UK economic data.

Sterling fell by over a percent against both the Euro and US Dollar in the wake of economic growth data which revealed the UK economy grew a mere 0.1% in the first three months of 2018, growth that has virtually killed any prospect of an interest rate rise being delivered by the Bank of England in May.

Will the incoming data surveys point to a pick-up in activity, or will they suggest the economic slowdown is more entrenched?

From the market expecting a hike with almost 100% certainty a few weeks ago, the probabilities have now fallen to circa 50% after comments from the governor of the BoE suggested there might be a delay owing to the downturn in data.

The possibility of a delay in raising rates led to a drop in the Pound which is highly sensitive to interest rate expectations.

Expectations of higher rates tends to lift the Pound and vice versa for the lower rates. This is because higher rates tend to attract greater inflows of foreign capital drawn by the promise of higher returns and this increases demand for the Pound.

"We may see an outsized market reaction from any surprises, as they tilt markets toward or away from a May BoE hike," says Canadian investment bank TD Securities in their note on the week ahead.

The bullish market forecasts for Manufacturing are not shared by some, including Philip Shaw, an analyst at Investec, who sees risks to April's figure both from the sharp appreciation in the Pound and the heightened talk of a trade war in early April.

Shaw does, however, share the market's more upbeat forecast for Services, which he expects to rebound by three points to 54.7 due to the temporary impact of bad weather dissipating.

More generally the lack of market-moving data besides PMIs means the weak could be a slow one for the Pound.

"Domestically, next week may represent a lull before the storm provided by the 10 May Bank of England Inflation Report and MPC announcement," says Shaw. "Bearing in mind Mark Carney’s comments last week about mixed data, the decision may be more finely balanced than we had envisaged."

"But we judge that the MPC will believe that the tight labour market will override the softer than expected short-term inflation environment," concludes the analyst.

The other major event in the week ahead for the Pound is the UK local elections on Thursday, May 3 at 1.00 GMT.

The main way it could impact is via Brexit expectations, such as for example if there is a surprise outsized vote for the anti-Brexit liberal democrats, which might be Sterling positive.

If the Conservatives win a larger-than-expected majority it could impact on Sterling in two ways depending on how investors interpret the result.

It could be negative for Sterling because the Conservative party is probably the party most in favour of the 'harder' forms of Brexit.

At the same time is could be positive for the Pound if it is interpreted as showing increased confidence in Theresa May's leadership, suggesting a reduction in the influence of the far right within the party, and therefore more likely to deliver a pragmatic rather than ideologically driven Brexit solution.

A Labour landslide would be negative for Sterling, according to TD Securities.

"While polls have consistently been pointing toward big Labour wins/Conservative losses at next week's local elections, with GBP being vulnerable to political developments, we may see a negative market reaction to any "Labour landslide" headlines. Vote counting only begins on Friday, so results should trickle out later that day," say TD Securities.

It is not unusual for voters to use the local elections to express dissatisfaction with the reigning government so a labour victory would not be particularly surprising or necessarily especially indicative of future voting patterns.

Data and Events for the Euro

The most important release for the Eurozone in the week ahead is inflation data out at 10.00 GMT on Thursday, May 03.

Core is forecast to slip to 0.9% in April from 1.0% in March, compared to a year ago, whilst headline inflation is expected to remain at 1.3%.

"Base effects (i.e. a sharp increase in April 2017) do not help prospects for a rise towards 2%. Nor does the early timing of Easter, given a possible moderation in travel costs in April," says Philip Shaw, an analyst at Investec.

"Risks appear to lie to the downside with a 0.8% reading instead," adds TD Securities in their briefing.

German inflation data, released on Monday at 13.00, three days before the Eurozone-wide data, can often help predict the Eurozone number. Indeed other state data such as Italian inflation is also out on Monday.

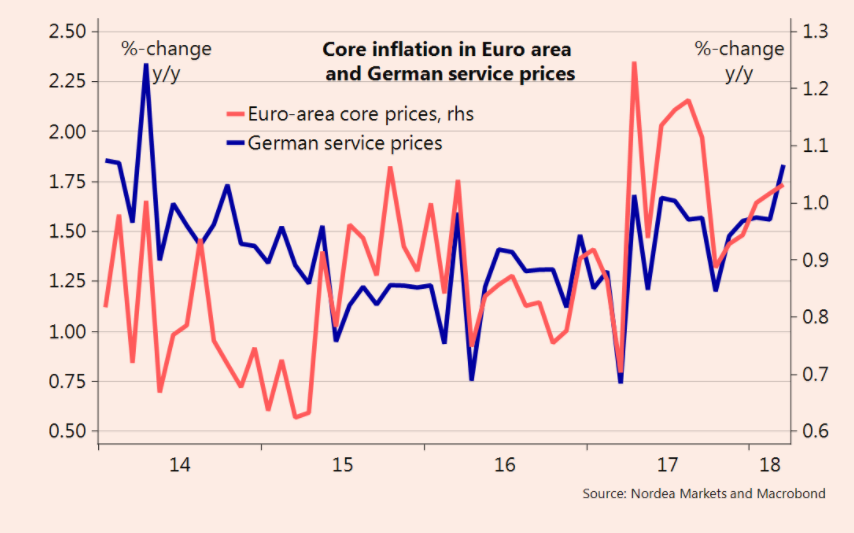

Services industry inflation is an especially useful gauge for general Eurozone inflation, according to Andreas Steno Larsen, FX and FI strategist at Nordea Bank.

"German flash inflation often leads the way for the Eurozone numbers. Especially the service price inflation correlates closely with the Eurozone core inflation," says Steno Larsen.

Inflation is a key influencer of the Euro because they impact on interest rates at the European Central Bank, and higher interest rates in turn drive capital inflows. The ECB is looking to withdraw stimulus and potentially start raising interest rates in 2019; an assumption adopted by markets in 2017 that lead to the Euro outperforming.

However, the ECB will only move if inflation is on track to hit their 2.0% target.

The other major release for the Euro in the coming week is first-quarter GDP data, out on Wednesday, May 2, at 10.00. Fears of a steep decline in the growth rate may be overexaggerated according to some individual state GDP releases already out, such as those for France, Spain, and Austria, where GDP data- though not very good - was 'face-saving'. As such the result is not expected to surprise to the downside and hit the Euro.

Nordea estimates growth to have slowed to 0.5% in the Euroarea in Q1 compared to the previous quarter, based on the results for Spain and France. This is slightly above the market consensus expectation of 0.4%, but slightly below the previous 0.6% result for Q4.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.