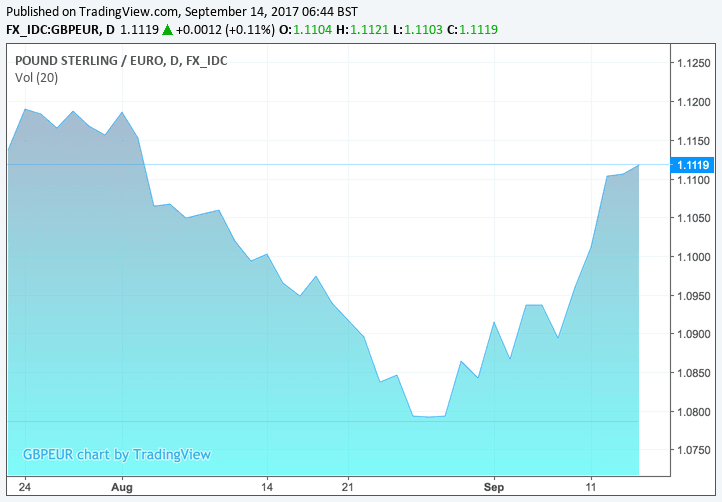

Pound Sterling's August recovery is likely to be short-lived as the Bank of England will be unable to provide any lasting long-term impetus. But, should gains extend above 1.11, a fall to parity in the GBP/EUR exchange rate becomes increasingly unlikely.

There is understandably a plethora of views regarding the Pound-to-Euro conversion's outlook; be it that the exchange rate will fall to parity, or make a sustained recovery into 2018.

However, the most popular view is Sterling will experience a near-term rally only to return to its losing ways over subsequent months.

The narrative is supported by ongoing price action which has seen the Pound rally from August lows amidst expectations surrounding future Bank of England polict moves.

The Bank is a key driver of Sterling value at present, alongside expectations regarding Brexit.

The Pound rallied into mid-year when markets thought the Bank was becoming increasingly open to raising interest rates by 0.25%, but subsequently reversed direction and hit fresh eight-year lows when those assumptions were dashed.

The pendulum has swung in the other direction once more with September’s release of inflation data from the Office for National Statistics triggering heightened bets that the Bank will bring forward their next rate rise.

Sterling has obliged these expectations and gone higher but the final verdict on this dynamic will be delivered on September 14 when the Bank briefs markets on their latest assessment and decision.

Rising inflation in the UK, combined with evidence that wages are rising, "will be music to the ears of BoE hawks looking for inflation evidence to justify a removal of the post-Brexit emergency monetary stimulus," says Viraj Patel at ING Bank N.V. in London.

ING argue the risks of a "hawkish hold" this week – and a third rate hike dissenter joining the ranks – have increased.

“In the scenario of a 6-3 MPC vote split, the initial knee-jerk market reaction could see odds of a November BoE rate hike rise to 50%,” says Patel, which if correct we believe will in turn consolidate Sterling’s recent gains, or even extend them and set the Pound up for a decent September.

But with the UK political environment over next three months being “anyone's guess,” ING believe such hawkish BoE steps, “if anything, should be viewed as teeing up markets for a 1H18 rate hike.”

Moreover, ING believe any hawkish re-pricing in the UK rate curve "is only likely to offer the Pound a one-time boost; we would expect Brexit to once again recapture the narrative for GBP price action in Oct ahead of key political events.

Analyst Kamal Sharma at Bank of America Merrill Lynch agrees saying he is looking for near-term Sterling strength to give way into year-end.

"We reiterate our current call for a weaker GBP heading into a series of political events that we think will test the market's belief that a transition agreement will be announced sooner rather than later," says Sharma in a note published September 12.

There are other fundamental reasons to bearish Sterling long-term, apart from Brexit and the Bank of England.

"Long EUR/GBP has been one of our top macro trades for 2017 and we remain bearish GBP," says John Wraith, a strategist with UBS in London.

Wraith cites the UK's current account imbalances (the country imports more than it exports) remain the main medium-term driver for Sterling as opposed to the Bank of England.

"Increasingly complex Brexit negotiations also pose downside risks for GBP and we see EUR/GBP at 0.97 by end-2018," says Wraith. EUR/GBP at 0.97 gives a GBP/EUR rate at 1.03.

Indeed, it is the current account imbalance that largely underpins HSBC's forecast for Sterling and Euro to reach parity in early-2018.

But ING - like consensus in the analyst community - are more constructive saying a sustained move in EUR/GBP below 0.90 this week (GBP/EUR above 1.11) "will almost certainly shelve any parity fears for now."

Above: Sterling has put the multi-year August lows behind it, but has been unable to break and sustain levels above the magic 1.11 level.

ING officially forecast EUR/GBP at 0.90 in three months and 0.88 in six and twelve months. This gives a GBP/EUR rate at 1.11 and 1.1360.

BAML officially forecast the Pound-to-Dollar exchange rate to end 2017 at 1.25, and end 2018 at 1.27.

The Euro-to-Pound Sterling exchange rate is forecast to end 2017 at 0.92 and end 2018 at 0.94.

This gives us a Pound-to-Euro rate at 1.09 and 1.06.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Employment Data Caps the GBP/EUR Advance but Majority of Gains Held

Halting Sterling's against the Euro mid-week, and ahead of the all-important Bank of England event, is the release of labour market data from the Office for National Statistics.

The data confirmed the UK economy continues to offer more jobs with the unemployment rate dipping down to 4.3%.

But Pound Sterling eased off recent highs on news that UK wage growth read at 2.1% in July, unchanged on the previous month's figure.

Markets had forecast 2.3% growth, and it is because of this miss on expectations that the Pound has edged lower.

With wage growth at 2.3%, and inflation at 2.9%, it is clear the average citizen is getting poorer.

"Sterling traders didn’t know what card to play. Sterling lost a few ticks after the release, but maintained most of its recent gains," says Piet Lammens at KBC Markets in Brussels.

Rising inflation and stalled wage growth will have a knock-on effect on spending elsewhere in the economy and might help explain why the UK's economic growth rate has come off the boil in 2017.

"While the continued strength of employment will be welcomed by the MPC, the continued absence of a pick-up in wage growth is likely to keep the doves in the majority. And with inflation reaching 2.9% in August, the squeeze on households’ real incomes probably intensified. That would make the risk of a sharper downturn in consumer spending the overwhelming concern to the majority of the MPC members," says Andrew Wishart, UK Economist at Capital Economics.

The Bank of England will therefore surely mention unease with the ongoing inflationary pressures which are now exceeding the forecasts laid out by the Bank in their August Inflation Report.

Any such mention would be beneficial for the Pound and could cement the recent recovery.