Pound Sterling should stabilise around current levels ahead of a recovery into 2017 according to forecasts contained in Lloyds Bank's latest International Financial Outlook.

Another week, another worst-performer gong for GBP.

While the country's athlete's are picking up gold in Rio, the currency is quite content to snatch the wooden spoon in the G10 standings.

"Sterling was weighed down at the start of the weak by dovish commentary from MPC member McCafferty, and later as the BoE QE programme was restarted, which drove Gilt yields to record lows," explains Kit Juckes, analyst with Societe Generale in London.

However, the under-performance cannot continue forever according to projections released by the UK's high-street giant, Lloyds Bank.

Yes, Lloyds Bank Commercial Banking have released their latest International Financial Outlook publication.

The report contains the bank’s latest thinking on the direction of global interest rates, yields, central bank actions and exchange rates.

The report comes after markets and analysts have had the chance to gauge the UK economy following the Brexit vote of June 23rd.

While no major economic data releases concerning the post-referendum economy are yet available, there have been a good amount of leading indicators to grab onto.

Data has certainly been mixed, and while there is certainly a consensus for lower economic growth and a lower Sterling, there are some who hold a more constructive view.

We reported this week that analysts at Intesa Sanpaolo are holding onto forecasts that see the GBP/EUR exchange rate hovering around current levels for much of the coming year.

This is juxtaposed against a broader consensus for deeper falls held by other major institutions.

Latest Pound/Euro Exchange Rates

| Live: 1.1709▲ + 0.05%12 Month Best:1.1712 |

*Your Bank's Retail Rate

| 1.1311 - 1.1358 |

**Independent Specialist | 1.1545 - 1.1592 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

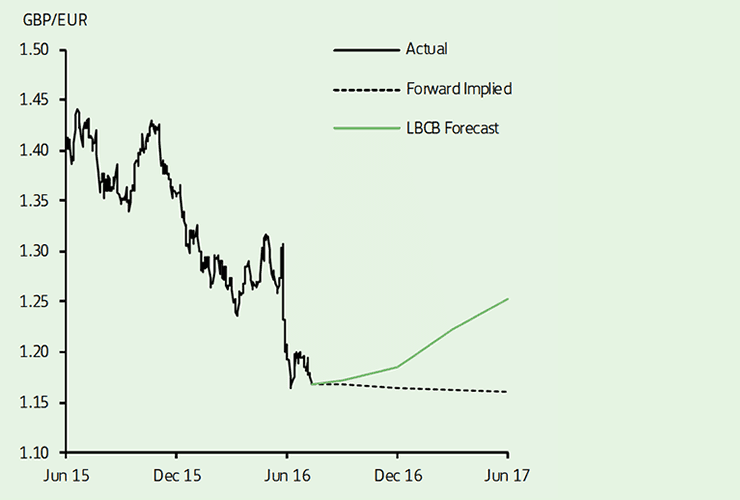

Lloyds Bank: Back Towards 1.30, Pound Undervalued

Like Intesa Sanpaolo, Lloyds Bank have released forecasts that place them at the upper end of the spectrum.

“Our estimates suggest that the decline in GBP/EUR since the UK’s EU referendum has left GBP approximately 10% undervalued,” note Lloyds.

In part, this divergence reflects the rise in political uncertainty and the associated increase in risk premia since the referendum.

“While GBP/EUR pulled away from its recent low below 1.16, following Theresa May’s appointment as prime minister, the overarching uncertainty over the domestic political outlook leaves sterling susceptible to bouts of volatility,” say Lloyds.

Indeed, we have noted that these 1.16 lows look vulnerable to a break. However, it would seem Lloyds have this eventuality covered in their “susceptible to bouts of volatility” clause.

Lloyds believe that markets will have to soon focus on the impact of the referendum on the rest of Europe, given forthcoming elections in the year ahead, which suggests to them that that the euro is also vulnerable.

Furthermore, the European Central Bank (ECB) will continue to outstrip the Bank of England in terms of the size of its quantitative easing programme, which should see the EUR underperform the GBP eventually.

“While the recently announced policy measures from the Bank of England argue for a weaker sterling, the strong likelihood of an extension to the ECB’s QE programme suggests that the ECB’s balance sheet will continue to expand at a more rapid pace than that of the Bank of England, which on a relative basis argues for higher GBP/EUR,” say Lloyds.

Overall, Lloyds expect GBP/EUR to drift gradually higher towards 1.19 by year end, rising to 1.27 by the end of 2017.

Another Bank of England Interest Rate Cut Coming

In August the Bank of England delivered a 25bp cut in Bank Rate – alongside an extension of its quantitative easing programme and a new Term Funding Scheme.

The aim is to suppress UK lending costs in order to oil investment spending by British businesses.

The Bank Rate is not expected to return to its previous level of 0.50% until around 2022, on prevailing market pricing.

This has seen the GBP decline back towards the early July lows against the Euro and US Dollar, while it has surpassed these lows against others, notably the Australian Dollar.

Near term, Lloyds believe a further cut in Bank Rate is likely, with the Bank of England indicating that a majority on the MPC was in favour of cutting the rate to its ‘effective’ zero bound at the August meeting.

“While the BoE has so far carefully avoided specifying the precise level of this lower bound – beyond indicating that it judges it to be “close to, but a little above, zero” – our base scenario sees Bank Rate being eased to 10bp at November’s policy meeting, alongside the next update of the Inflation Report projections,” say Lloyds.

The Risks: No Real Data for Forecasters to Grapple With

It will only be in September when the first concrete statistics concerning the post-referendum economy are released by the official statistics body.

Until then we have to rely on forecasts and projections being based on assumptions regards the underlying economy.

Even the Bank of England has not had the luxury of awaiting official statistics from which to base their projections and policy changes.

In short, a lot could change over coming months.

There is certainly a lot of negativity written into the GBP and interest rate expectations, based on the assumption the Brexit vote has hit UK economic activity hard.

The risks are therefore to the upside in my view, and with markets so heavily biased against Sterling, the chances for a stronger-than-expected performance in GBP should be something those watching the market are wary of over coming months.