The Bank of England fired its monetary bazooka on Thursday the 4th August - we cover the event as well as analyst reactions and predictions on where Pound Sterling is headed as a result.

The British Pound fell sharply, and stock markets rose, as the Bank of England (BoE) announced a substantial easing package at their August 4th meeting.

The declines of 1.5% ensured that the UK currency was the worst-performing unit in the G10 exchange rate complex as a result.

Some would argue the declines could have been worse, were it not for the already-exisiting anti-GBP bias preferred by the global trading community.

That everyone is already betting against the currency could have been its saving grace.

Nevertheless, we would hesitate to say we are at the cusp of a notable recovery and would suggest the road lower from here will be a gradual one.

The Bank's Monetary Policy Committee announced a 0.25% cut to the basic interest rate but it was the expansion of the quantitative easing programme by £60bn that really caught attention.

Of note, corporate debt will now be bought in addition to government debt with the Bank citing this route as being that which offers greater policy returns.

About 150 firms are deemed to be eligible at present and minimum investment amounts of £100m will be considered.

The impact on Sterling is negative in that the supply of money into the economy increases, thereby driving down the unit cost of Sterling.

Commentators have described the action as representing one of the boldest package of stimulus we have seen since 2009.

Latest Pound/Euro Exchange Rates

| Live: 1.1708▲ + 0.04%12 Month Best:1.1711 |

*Your Bank's Retail Rate

| 1.131 - 1.1357 |

**Independent Specialist | 1.1544 - 1.1591 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

"For once, the man so often dubbed the unreliable boyfriend has turned up with a bunch of flowers and a box of chocolates. For once he over delivered. If there is anything that markets love, it is QE, as Mario Draghi can certainly attest," says Joshua Mahony, analyst, at IG.

Furthermore, no UK recession is envisaged by the Bank, as per the forecasts contained in the Inflation Report.

Nevertheless, this is a Bank that is not willing to standby and watch growth deteriorate.

The BoE maintained a very dovish stance indicating a further rate cut later this year to the effective lower bound at above but close to zero.

It was also stressed that it can do more quantitative easing, in both gilts and corporate bonds, if needed.

This all played into the hands of a weaker currency and a stronger stock market.

Key Takeaways

The headline policy measures saw a 0.25% rate cut, £70BN increase to the QE programme of which £10BN will involve the purchase of corporate debt.

Commentators believe rates could be as low as 0% by the end of the year based on the dovish tone of the event.

However, Carney has expressed a deep discomfort with pursuing negative interest rates, and we do see a limit to cuts as a result.

Of the policy committee, Weale, McCafferty and Forbes were shown to be resistant to conventional QE (i.e Gilt buying), while Forbes opposes Corporate Bond buying.

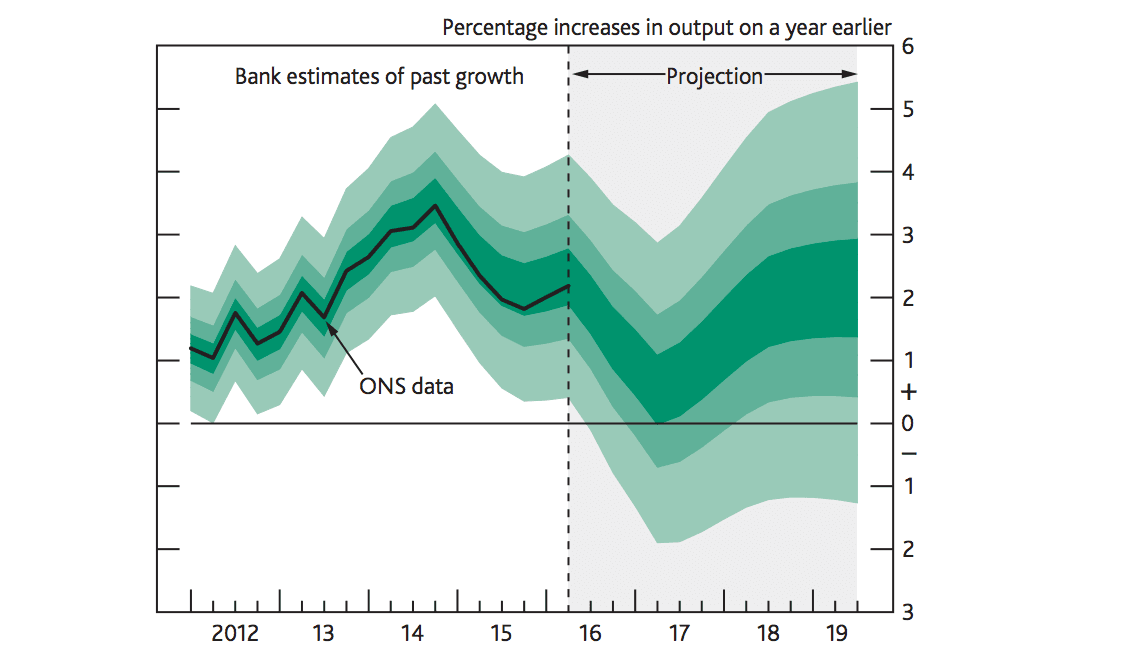

Figures revealed in the quarterly Inflation Report shows inflation to overshoot 2% target on a two year horizon, largely on the back of a weaker Sterling which implies imports will become more expensive.

Economic growth forecasts were downgraded for 2017 from 2.3% to 0.8%.

Growth recovers to 1.8% in 2018, confirming no recession is forecast:

Above: The Bank of England's GDP forecasts based on assumptions that its new measures will behave according to plan.

Immediate Currency Forecasts Suggest a Grind Lower for GBP

Here is a snapshot of the where a handful of leading FX analysts see the UK currency moving in the wake of the event.

TD Securities: The BoE's package of easing measures is enough to reignite sterling's weakening trend. The move below trendline support around 1.3180 in the immediate aftermath of the decision puts support at 1.3058 into view. We do not expect this to hold for very long however, suggesting a challenge of the post-referendum low at 1.2798 may not be too far off.

Over the next 3- to 12-months, Goldman Sachs say they are comfortable with their view that the slowdown in economic activity will drive the currency lower, they forecast £/$ at 1.20 and 1.25 and EUR/£ at 0.9 and 0.80 in 3- and 12-months, respectively.

Andy Scott, Economist at HiFX:

"Against the Bank’s downwardly revised growth forecasts for growth and employment, the outlook for Sterling remains negative with risks to 1.25 versus the US Dollar and 1.10 versus the Euro."

Shaun Osborne at Scotiabank:

"Cable has spent most of July consolidating in a triangular pattern around the 1.31/1.32 range. This morning’s sell-off is pressuring the lower bound of the range and short-term price signals are bearish. A break under 1.3165 intraday should see losses extend near-term and would point to a resumption of the longer-term sell-off in the GBP more broadly."

Viraj Patel at ING: “While we look for more GBP downside against EUR (3m EUR/GBP target: 0.88), we think any weakness will be orderly. To take advantage of this, we propose a EUR/GBP call structure with a reverse knock-out barrier." This implies a downside target in GBP to EUR terms at 1.1363.

Trevor Charsley, Senior Markets Advisor at AFEX, reckons: "The logical conclusion is that we’re likely to see more Sterling weakness in the short and medium term with both GBP/USD and GBP/EUR having the potential to fall further than the lows seen immediately after the Brexit vote."

Positive and Negative Analyst Reactions

Positive Reactions:

The move by the Bank was welcomed by Chancellor Hammond. As we note further down in this piece, the real growth to the UK economy going forward will likely come from what Hammond and his team at the Treasury announce.

Jonathan Loynes at Capital Economics: "There have been some suggestions that a policy loosening will have no impact on the economy and could even adversely affect confidence. But the Committee clearly decided otherwise, wisely in our view. If nothing else, the measures send a strong signal that the MPC is prepared to look through the inflationary consequences of the post-referendum drop in the pound and focus instead on supporting sentiment and activity."

CBI Chief Economist, Rain Newton-Smith: “The combination of a rate cut and more quantitative easing should be a shot-in-the-arm for business and consumer confidence, lowering borrowing costs and keeping liquidity flowing through the economy.

“The Bank’s action will help restore confidence in the UK economy and what’s now most important to businesses is that the Government develops a clear plan and timetable for EU negotiations."

Negative Reactions:

Andrew Sentance, former MPC member, rubbishes the decision to expand Quantitative Easing. The senior economic advisor at PwC says QE:

"Additional Quantitative Easing is unlikely to be effective in the current climate. QE helps to push down bond yields and boost financial confidence - and had a positive effect back in 2009 when the financial system was so weak. But this situation is different, and QE could create unintended consequences - weakening the pound and further undermining the already low rates of return which pension funds and other investors are able to earn."

Holly Mackay, MD at Boring Money: "Anyone with cash savings has to reassess this strategy as interest moves from poor, to dire. Many Brits have an aversion to the stock market but it's time to ask if we're just shooting ourselves in the financial foot."

On the issue of inflation eating into savings accounts, Carney says he is looking at the economy in 'aggregate' - i.e savers must take a backseat in the fight to keep growth and employment propped up. "Should we have more people lose their job, in order to cater to another sector of the economy?" asks Carney.

This was certainly a robust response to the suggestion that he is eating into people's savings.

Nawaz Ali, UK Currency Strategist at Western Union Business Solutions: meanwhile expressed concerns for the squeeze on margins that importers may now start to feel:

"For British importers already trying to come to terms with the Pound’s significant fall since Brexit, I think today’s news will raise fresh concerns about continued weakness and I would expect to see an increase in firms’ hedging activity."

However, the Bank's inflation report believes that the weaker exchange rate provides a good opportunity for demand to switch from foreign markets to the domestic market.

i.e. businesses will be more keen to strike deals with UK-based suppliers going forward, this in turns hould aid the economy.

Quantitative Easing Announcement Hits the Pound

The Bank announced it would buy £60BN worth of gilts and £10BN worth of investment-grade corporate debt, noting that it expects the latter to be particularly effective:

On the issue of the buying of corporate debt, the Bank notes:

"Purchases of corporate bonds could provide somewhat more stimulus than the same amount of gilt purchases. In particular, given that corporate bonds are higher-yielding instruments than government bonds, investors selling corporate debt to the Bank could be more likely to invest the money received in other corporate assets than those selling gilts."

A look at the following suggests why the BoE believes corporate bond yields could come down:

Following the string of ominous UK PMIs between Monday and Wednesday, Mark Carney and co. were guaranteed to do something on the basic interest rate.

The main uncertainty is over quantitative easing and this is where things get lively for the British Pound which has arguably absorbed the impact of a rate cut.

Quantitative Easing & Rate Cuts Will Only Do So Much

Analysis from Bank of America's Robert Wood questions the effectiveness of monetary easing noting that the Bank's policy toolbox will have its limits.

"The fundamental issue with all the monetary policy tools we can think of (see here for a longer note explaining all our thinking) is that they are close to pushing on a string. The central bank can try and incentivise credit supply but credit supply is not the problem," says Wood.

Wood says there is relatively little it can do to boost credit demand given that interest rates cannot fall much further, and cuts from here come with costs as well as benefits.

What is the answer?

"The textbook solution to this issue is fiscal stimulus. And anyway, the case for more government investment was strong even before the vote to “Leave” the EU," says Wood.

This week Pound Sterling Live looked at the potential Pound reactions to Chancellor Hammond's planned stimulus drive due to be launched in the Autumn.

"The government has provided little guidance on its plans so far. If it did unveil a strong package later this year, that could be a reason to become more optimistic about growth," says Wood.

The suggestion comes as Germany announces a massive massive €270BN investment in transport infrastructure and Labour leader Corbyn says he will boost borrowing by £500BN to increase spending.

Indeed, Carney himself noted that there were limits to what the bank could achieve, and it was now up to politicians to guarantee the future prosperity of the UK's citizens.