It would be a mistake to doubt the Bank of England's ability to push yields, and therefore the Pound Sterling, even lower argue Morgan Stanley.

- Pound to Euro exchange rate today: 1 GBP = 1.1621 EUR

- Euro to Pound Sterling exchange rate today: 1 EUR = 0.8603 GBP

- Morgan Stanley argue the ECB and BoE can expect differing returns on further monetary policy

- Lloyds Bank take a different stance, arguing the ECB will push the Euro yet lower

The Pound is threatening to break below its post-referendum lows as we enter a new phase of British Pound weakness - one that is driven by the actions of the Bank of England on UK bond markets.

The Bank has pledged to buy up to £60BN worth of UK government bonds (Gilts) from the markets over the next six months in order to try and force down the yield paid by those bonds.

The effectiveness of these reverse-auctions will ultimately decide how low the Pound can go.

A further £10BN worth of corporate debt is to be purchased in order to directly force down the borrowing costs at companies that are seeking to borrow in excess of £100BN from the markets.

The flood of fresh Pounds onto the market will ultimately devalue the currency on a unit basis.

We heard that on Monday bond buy-backs had forced ten-year and five-year yields to hit new record lows of 0.603 percent and 0.152 percent respectively.

The successful move was repeated on Wednesday the 10th when the Bank bought £1.17BN worth of Gilts with maturities of between 2023 and 2030.

The reverse-auction was oversubscribed 4.7 times.

This has opened the gap between the yields paid by Eurozone and US bonds on the one hand, and UK bonds on the other.

The opening of this gap against UK yields provides the downforce acting on the value of the Pound as foreign investors opt against investing in UK assets.

When the effectiveness of this policy of lowering yields through buy-backs is questioned, as was the case on Wednesday the 10th of August when the Bank announced it was unable to find enough sellers of bonds, the Pound moved higher alongside improved yields.

Therefore we will continue to watch the success of the reverse-auctions.

The Bank itself will be happy with the falling in yields as it lowers borrowing costs while the weaker currency will prove helpful in stimulating exports.

In their August Inflation Report the Bank also said the weaker exchange rate will boost the country's income from the return on foreign-owned assets which have risen in Sterling-terms.

Latest Pound/Euro Exchange Rates

| Live: 1.1674▼ -0.01%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1277 - 1.1324 |

**Independent Specialist | 1.1511 - 1.1557 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Quantitative Easing is a Powerful Weapon in the Hands of the Bank of England

If the Bank of England is aiming for a weaker exchange rate to stabilise the UK economy in a post-referendum world, then it can consider itself lucky.

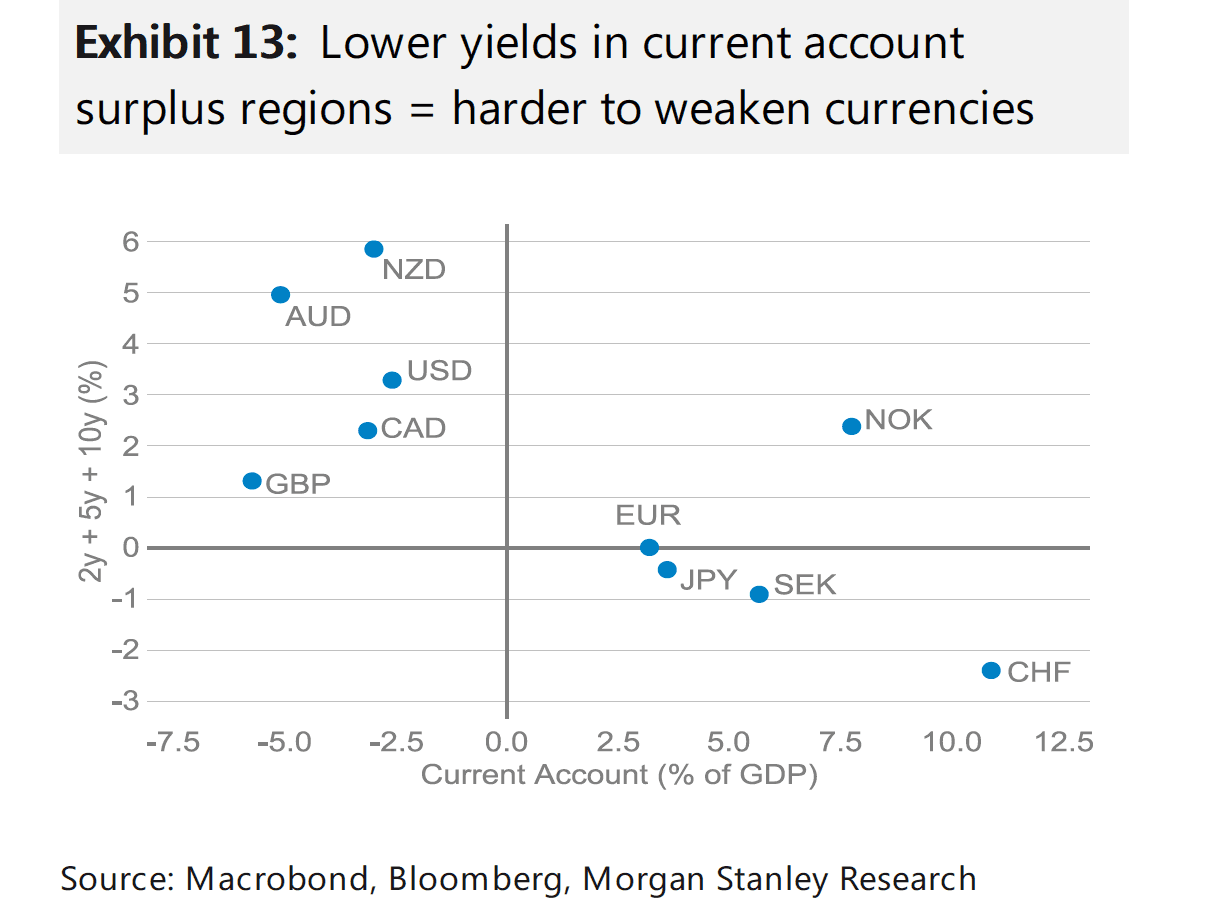

Analysts at Morgan Stanley believe that there is still sufficient space for the currency to be forced lower as the Bank has the room required to further pressure Gilt yields through their market actions.

This is something that the likes of the Bank of Japan, European Central Bank and Swiss National Bank are no longer able to achieve thanks to years of aggressive rate cuts and quantitative easing.

In effect, these Banks have exhausted their ability to lower their currencies through monetary policy easing.

Morgan Stanley describes this phenomenon as ‘exhaustion of the yield curve’.

As can be seen, GBP stands apart from the likes of EUR, JPY, CHF and SEK in that it has further to fall:

It is this observation that has seen Morgan Stanley call a Buy on the EUR/GBP exchange rate, in anticipation of further falls in the Pound Sterling on the back of Bank of England action.

“UK bond yields being higher than those in the Eurozone, means that UK bond yields have further to fall, supporting our long EUR/GBP trade,” says a strategy note from Morgan Stanley.

Analysts will be watching out for any weakness in hard UK data to suggest how much more easing the BoE could do.

The markets will also be watching for signs of further Bank action over coming months from the Bank itself.

This helps explain why the GBP fell on comments by the Bank’s Ian McCafferty that further easing remains a possibility.

ECB to Prove Ineffective in Weakening the Euro

Further weakness in the Pound to Euro exchange rate will likely be derived from the observation that the Euro will remain sticky to further weakness.

Recall that the European Central Bank has apparently reached its limit in prompting further currency devaluations?

Even if the ECB cuts rates by 10bps in September, as Morgan Stanley’s economists expect, this is unlikely to do much for EUR given the bank balance sheet constraints and the already depressed level of yields

“While the Brexit outcome is negative for euro area growth, we see no immediate channel that is likely to drive EUR weakening,” say Morgan Stanley. “The Euroarea runs a current account surplus, which would need to be recycled elsewhere to drive EUR weakness - a tall order in an environment of declining risk appetite and returns.”

Furthermore, it is observed that the economy is simply in no position to deliver the upside surprises required to stimulate a GBP recovery while the country's deficit in goods and services with the rest of the world remains another area of vulnerability.

Indeed, on the 9th of August the ONS reported that the UK's trade balance remains deep in deficit as record imports outstrip exports.

"The UK's 7% of GDP current account deficit requires inflows to balance the balance of payments. Declining relative investment return expectations make it more difficult for the UK to attract sufficient funds at current GBP levels," say Morgan Stanley.

Buy the Euro Using the Pound

Morgan Stanley strategists entered a Long EUR/GBP trade on the 14th of July at 0.8334; the target is 0.9000 with a stop-loss seen at 0.8340.

From a GBP into EUR perspective, this translates as follows: 0.8334 = 1.1999, 0.9000 = 1.1111, 0.8340 = 1.1990.

The risks to this trade are better-than-expected UK data and a subsequent view taken by markets that the Bank of England could comfortably step back from easing stimulus further.

The forecasts are published days after we reported that Intesa Sanpaolo see limited downside available in the currency pair.

Intesa believe that the BoE simply doesn't have the firepower, or willingness, to trigger a major fall in Sterling.

Lloyds: Pound now Undervalued, And the ECB DOES Retain Ability to Force EZ Yields, Euro Lower

An interesting point to consider has been provided by Lloyds Bank who have over recent hours released their latest August International Financial Outlook.

In the research paper analysts say that the recent declines in Sterling now leave it overvalued against its Eurozone peer.

"Our estimates suggest that the decline in GBP/EUR since the UK’s EU referendum has left GBP approximately 10% undervalued. In part, this divergence reflects the rise in political uncertainty and the associated increase in risk premia since the referendum," say Lloyds.

Lloyds warn the currency is likely to remain vulnerable while the impact of the referendum on the rest of Europe, given forthcoming elections in the year ahead, suggests that the euro is also vulnerable.

Lloyds expect GBP/EUR to drift gradually higher towards 1.19 by year-end, rising to 1.27 by the end of 2017.

Furthermore, Lloyds disagree with Morgan Stanley on the potential effectiveness of further ECB action.

Recall that Morgan Stanley believe the ECB, like the BoJ suffers from 'exhaustion of the yield curve' and therfore further policy actions may be in effect useless?

Not so suggest Lloyds: "The strong likelihood of an extension to the ECB’s QE programme suggests that the ECB’s balance sheet will continue to expand at a more rapid pace than that of the Bank of England, which on a relative basis argues for higher GBP/EUR."

Eurozone GDP Data Sends Mixed Signals

Whether or not the ECB acts again on interest rates and their quantitative easing programme will of course depend on the trajectory of Eurozone data going forward.

Germany reported a better-than-anticipated 0.4% rise in GDP on the 12th August, economists had forecast growth of 0.2%.

This compares favourably to Italy’s figure which was at 0%, growth of 0.2% had been forecast.

The Eurozone flash reading was as expected at 0.3%, meaning the Eurozone halved its growth between Q1 and Q2.

This suggests growth is slowing, particularly in the periphery, something that could prompt more EUR-negative action at the ECB.

However, the Germans have long expressed opposition to the ECB's policies, and with their growth looking robust, one would expect any changes to be hard-fought.