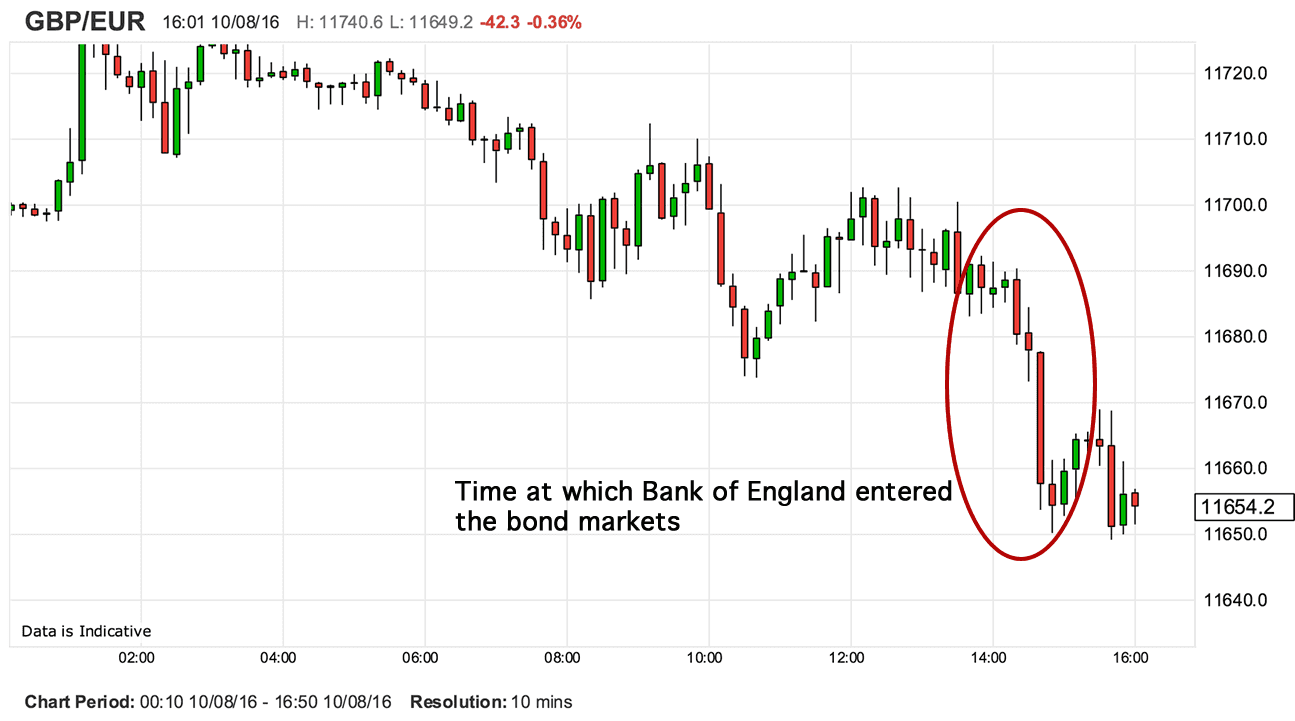

The GBP has fallen once more as the Bank of England successfully hits its Gilt purchase target for Wednesday the 9th, a day after it surprised financial markets by missing its desired target.

- Pound to Euro exchange rate today: 1.1650

- Euro to Pound Sterling exchange rate today: 0.8583

- Pound to Dollar exchange rate today: 1.30

The Pound remains under pressure following the success of the Bank of England's most recent quantitative easing operation.

We have noted over recent days that it is the fall in UK government bond yields that result from the Bank's quantitative easing programme that is the main driver of Sterling weakness at present.

The Bank went to the markets in early afternoon Wednesday with the ambition of buying up to £1.17BN worth of government debt from willing sellers.

It succeeded, with the amount of bonds being offered being 4.7 times the amount that the Bank could purchase.

The result were higher Gilt prices and lower yields which hit Sterling:

The GBP fell sharply on Monday when the initial reverse-auction saw a similar outcome.

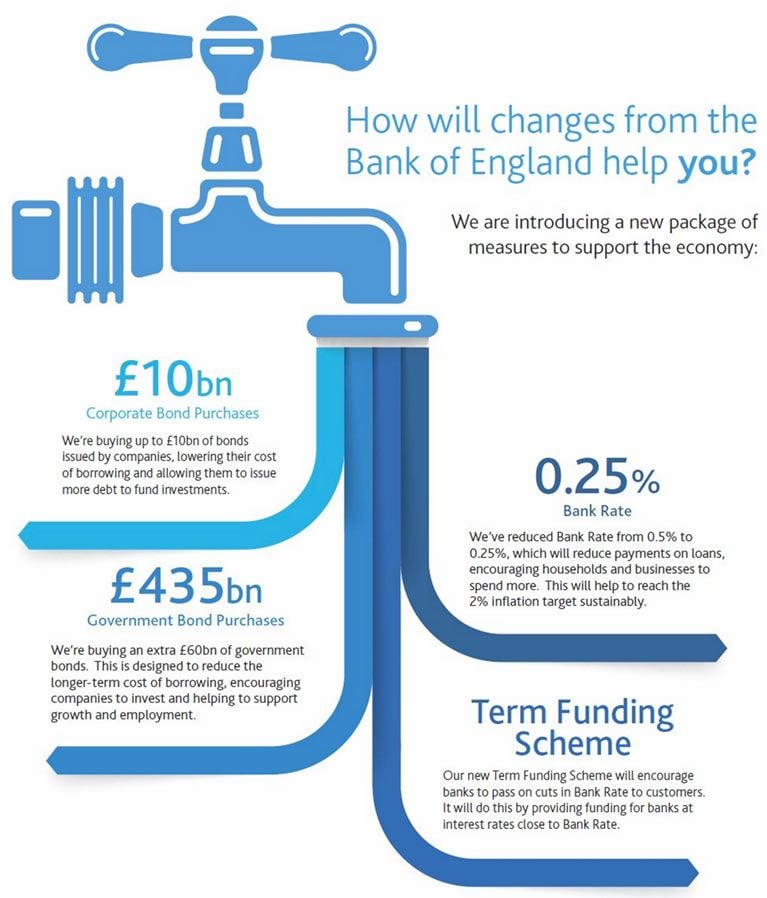

The Bank's expanded quantitative easing programme seeks to buy up to £60BN worth of government bonds using freshly printed money in an attempt to force down yields, and subsequently borrowing costs for UK companies.

A weaker Pound is the necessary side-effect of the process, indeed the Bank believes a weaker GBP will aid economic growth.

Sterling managed to recover above 1.30 against the Dollar on Wednesday morning after the Bank reported that its Tuesday auction saw it struggle to find sellers, suggesting it may not be able to fully meet its QE target.

If this continues to happen then we would assume that future easing, as threatened by the Bank's McCafferty on Tuesday, will be less effective and less likely.

This would see GBP stabilise, and even recover.

The Bank will run the quantitative easing programme over the course of six months, with three auctions a week expected.

The Bank will seek to buy Gilts with a residual maturity of 3-7 years on Mondays; of over 15 years on Tuesdays; and of 7-15 years on Wednesdays.

Latest Pound/Euro Exchange Rates

| Live: 1.1605▼ -0.04%12 Month Best:1.1659 |

*Your Bank's Retail Rate

| 1.121 - 1.1257 |

**Independent Specialist | 1.1443 - 1.1489 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Bank of England: The Driving Force of a Lower Pound

The reason for the GBP exchange rate’s recent decline has more to do with issues surrounding activity at the Bank of England.

Recall that on Thursday the 4th of August the Bank announced a massive stimulus programme:

The big deal for Sterling right now is that the Bank is actually active in the markets for UK government debt (Gilts).

Reports suggest there has been huge demand created by the Bank of England’s entry into the market which has in turn boosted the price of UK Gilt futures.

Simon Peck, rate strategist at RBS, says the market is benefiting from "net negative supply" as the BoE would buy more bonds over the next eight weeks than the British government would issue.

While Gilt prices rise, their yield - the rate paid back to holders of the Gilt - must fall.

And it is yield on government debt that matters for global currencies.

As the UK’s yield falls, and that of the Eurozone and the US stays static, or rises as in the case of the latter, so the downward pressure on Sterling increases.

This dynamic could actually extend, if the words of Bank of England Monetary Policy member Ian McCafferty prove prophetic.

McCafferty wrote in the Times that he sees the potential for further quantitative easing and interest rate cuts in the future.

McCafferty noted:

“More easing is likely to be required” and “easing policy further, until we are more certain of the balance between lower growth and rising inflation, risks pushing inflation yet further above the target.”

This suggests the Bank is willing to overlook inflation above 2% if the ultimate outcome is stronger economic growth.

“The pound sterling resumed its debasement on Tuesday as Ian McCafferty, one of the most hawkish MPC members, declared that the central bank should be ready to deliver more easing in the event that the UK economy slows according to the initial surveys,” notes Arnaud Masset, a market analyst with Swissquote Bank.

GBP/USD fell 0.50% in Tokyo and moved as low as 1.2973. On the downside a key support can be found at 1.2798 (low from July 6th); further south a support lies at 1.20 (low from April/May 1985).

“The Pound should continue to trade with a negative bias as the BoE has opened the road for further monetary stimulus,” says Masset.

GBP Pointed Lower Against Both EUR and USD

The GBP/USD appears intent to trade around the fulcrum at 1.30, with a surprising rally above this level coming on late Tuesday through Wednesday morning.

"The dollar was trampled for the second day in a row declining against all its major trading partners in Asian and early European trade. The selloff has been to yesterday's weak productivity figures which sowed seeds of doubt that the Fed would actually tighten rates despite relatively robust jobs data," notes Boris Schlossberg at BK Asset Management.

Yesterday's Non-Farm Productivity report shocked the market printing at -0.5% versus 0.4% eyed.

"This was the one of the worst readings in years and greatly soured sentiment towards the dollar as traders quickly became skeptical that the Fed will want to tighten against such lackluster productivity growth," says Schlossberg.

The Dollar's woes allowed the GBP to arrrest the five day decline against the US Dollar.

Nevertheless, this bump is not enought to shift analyst expectations to anything other than remaining resolutely bearish on GBP.

"We see support at 1.2818, the early July low, but we think there is immediate risk for GBP/USD to the low 1.27s. We see resistance at 1.30 now – a big psychological resistance point," says Shaun Osborne at Scotiabank.

Osborne notes that the Pound should fall further to below 1.1614 against the Euro which is the 2016 low printed following the EU referendum sell-off.

Jeremy Stretch at CIBC Markets believes that while trade weighted Sterling has some way to fall before re-testing early July lows, it merely seems a matter of time.

"We maintain Q3 GBP/USD targets at 1.25. In the near term look for a test towards 1.2895. In terms of EUR GBP having taken out 0.85 look for the uptrend to extend towards 0.8570/80," says Stretch.

EUR/GBP at 0.8570/80 translates to GBP/EUR at 1.1669/65.

The declines come as a cocktail of data and policy-related events combine to paint a confusing picture with decent data being countered by negative events at the central bank.

UK Data: Better than Many had Expected

The UK data series out on Tuesday the 9th of August was surprisingly good.

Total sales increased by 1.9%, according to the British Retail Consortium and KPMG's latest survey for the month of July. In fact this was the best outturn in 6 months.

The data defies expectations for a post-referendum slump and could well prove many forecasters as having been too pessimistic on the UK economy following the vote.

A separate report, by Barclaycard, found spending in restaurants, pubs and cinemas continued to grow strongly in the month following the vote.

Meanwhile, official UK Manufacturing results came in mixed with Industrial Production bit better at 1.6% vs. 1.3% eyed while Manufacturing Production declined to 0.9% from the 1.4% increase forecast.

Both reports were taken just after the Brexit vote.

“Looking ahead, the strength over the quarter likely presages a softer tone of production activity in Q3. July’s manufacturing PMI fell to the weakest reading since February 2013, in an early sign of the changed economic outlook in the aftermath of the EU referendum result,” says a note on the matter from Lloyds Bank.

It is also noted that the monthly profile of activity through Q2 sets a high hurdle for outturns over Q3 to post any expansion over the quarter overall.

“By implication, a payback in Q3 will follow the outsized strength in Q2 – one that could add to the Bank of England’s inclinations for further policy easing,” say Lloyds.

Indeed, NIESR economic growth data reported GDP grew 0.3% in the three months ending July 2016.

This is down from 0.6% growth for the three months ending in June. July saw -0.2% growth confirming an immediate post-referendum impact and it does suggest a soft start to the new quarter.

There is an evens chance of the UK slipping into recession by the end of 2017.

Meanwhile, analysts at Capital Economics have said they believe recession will be avoided saying they believe the PMI data released in July and June may be exaggerating weakness.

"Like the Bank of England, we envisage broadly stagnant GDP in the second half of this year, rather than a deep recession," says Capital Economics' Ruth Gregory.