New research shows the purchase of European properties by Britons remains steady despite in the decline in value of the GBP to EUR conversion.

While the Pound Sterling has fallen against the Euro over the past 12 months, so too has British buying power in Europe.

The June 23rd EU referendum result saw Sterling lose about 14% of its value against a basket of its major peers.

While some of this value has been subsequently claimed back, the outlook remains challening for those hoping for a stronger Pound as the UK economy faces a prolonged period of uncertainty and record-low interest rates.

The slump comes after a period of strong GBP appreciation which helped fuel a robust demand for European properties by UK residents.

Athena Advisers, an international sales network and property investment advisory firm, reports that 2015 was a good year for British buyers targeting familiar European locations like France, Spain and Portugal, largely thanks to the strength of the UK’s currency.

In July 2015, the pound reached an eight year high on the Euro at 1.441 — the best value British property buyers in Europe had enjoyed since 2007.

Since then, the pound has followed a general downward trend, hovering around the €1.26 to €1.30 range in the lead up to the Brexit referendum.

So, does the decline in GBP spell the end for UK-Eurozone house buying?

Not so, argue Athena Advisers who report that in certain markets, contributing factors have helped reduce the currency effect.

And, in some case, factors have fully negated any loss in currency values.

Latest Pound/Euro Exchange Rates

| Live: 1.1591▼ -0.01%12 Month Best:1.171 |

*Your Bank's Retail Rate

| 1.1197 - 1.1243 |

**Independent Specialist | 1.1429 - 1.1475 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

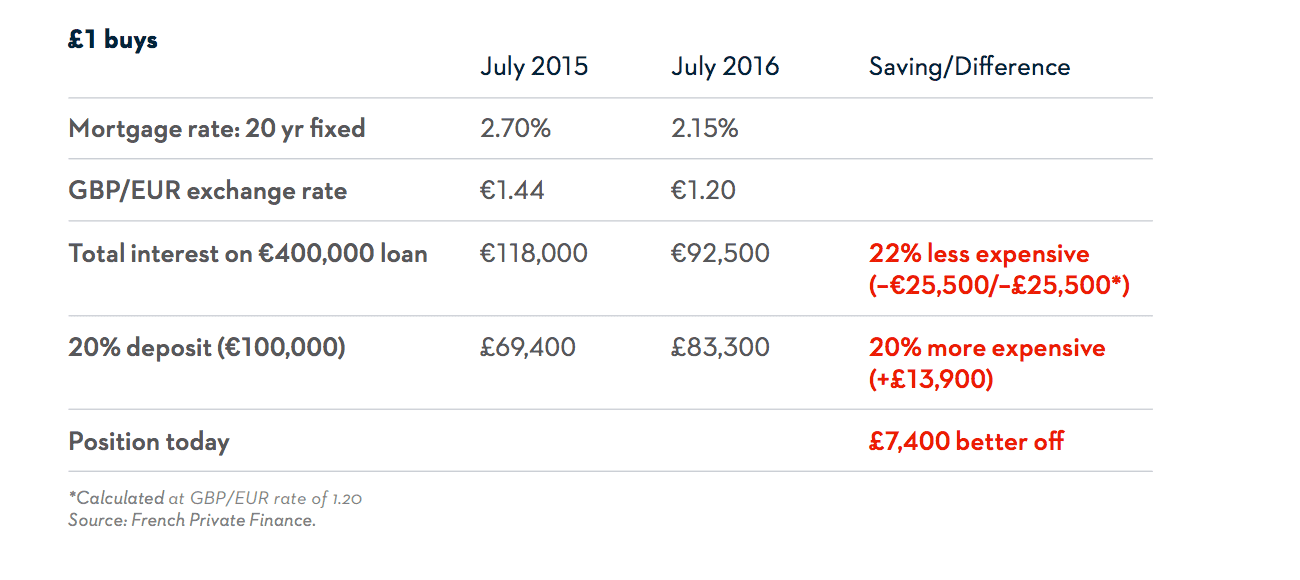

“In France, the continued decrease in mortgage rates available to non-residents has enabled purchasers to retain value in their investments,” says a note from Athen Advisers.

Data on French Private Finance shows that whilst a sterling-powered euro deposit has become 20% more expensive since July 2015 owing to exchange rate moves, the lowering of mortgage rates has reduced the interest payable over a 20-year term by 22%.

The lowering of finance costs comes in the wake of the European Central Bank cutting its rates into negative territory and the Bank of England cutting to just 0.25%.

“Whilst deposits for properties are up-front, cash costs and mortgage interest are paid off over the duration of the loan nullifying lost currency value and enabling British buyers to retain reasonable buying power,” say Athena.

Athena report that those buying second homes with euros now have good room for negotiation, as some foreign purchases halt their search.

“To date, we have had only one withdrawal from a British client on the basis of the Referendum result,” says John Busby, Private Clients Director at French Private Finance.

In a UK market where the average property loan is fixed for 2-3 years, the appeal of fixing a super low rate at 2.15% or lower for 20 years is very strong.

“Mortgage rates, soft prices and the British love affair with France will underpin the market for at least the next six months,” says Busby.

The Outlook Warns of Further GBP Decline

While mortgage financing costs cushion the blow dealt by a weaker currency, it would be argued that the counterbalancing effect can only go so far.

What if the Pound were to keep falling?

Indeed, this could well be the scenario we are faced with over coming months with new research from Scandinavian lender Danske Bank warning that they see further Euro appreciation against Pound Sterling.

The forecast comes in the wake of the Bank of England’s delivery of a substantial easing package on August 4th.

The good news though is that any GBP weakness is likely to be driven by further interest rate cuts at the Bank.

Therefore, a weaker GBP could be accompanied by lower financing costs, which could help Eurozone property buyers.

The move including a 25bp Bank Rate cut to 0.25%, GBP70bn QE (GBP60bn government bond and GBP10bn corporate bond purchases) and a new Term Funding Scheme (TFS).

The BoE maintained a very dovish stance indicating a further rate cut later this year to the effective lower bound at above but close to zero. BoE also stressed that it can do more QE (both gilts and corporate bonds) if needed.

“We expect BoE to cut the Bank Rate by 15bp to 0.10% and to increase its buying of both gilts and corporate bonds at the November meeting,” says Danske Bank in a note to clients.

Analysts expect weak UK GDP growth, monetary policy and flows to weigh on the GBP in the coming quarters.

We forecast EUR/GBP to rise to 0.90 in 6M, this equates to a GBP into EUR rate at 1.110.

Longer term Danske expect EUR/GBP to stabilise to some extent given attractive valuations.

They target 0.88 in 12M, or 1.1363 in GBP/EUR terms.

Bank of England Triggers Next Bout of Sterling Weakness

The major events of the week were the better than expected US employment report and the Bank of England's decision to cut the GBP interest rate by 0.25% and increase the QE by 70 billion pounds.

On Thursday the BOE decided to act for the first time after 2009 and reduce the GBP interest rate.

This was expected by traders but the QE increase was not and as a result the GBP lost notable ground on Thursday.

As the Bank embarks on its purchase of gilts and corporate debt over coming months we would expect the GBP to remain pressured as the unit value of Sterling is devalued by the increased supply of money to the market.

However, the supportive effect this should have on the economy should shield the currency from notable losses.

Of interest will be how inflation moves over coming months. Were it to rise at a faster-than-expected rate then the Bank may have to row back on low rates and look to raise them in order to contain inflation.