- GBP/EUR forecasts raised at Goldman Sachs

- Likely to stick to confined ranges short-term

- German election outcome to attract attention early on

- Watch broader market sentiment too

Image © Pound Sterling Live

- GBP/EUR reference rates at publication:

- Spot: 1.1664

- Bank transfers (indicative guide): 1.1346-1.1428

- Money transfer specialist rates (indicative): 1.1550-1.1590

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

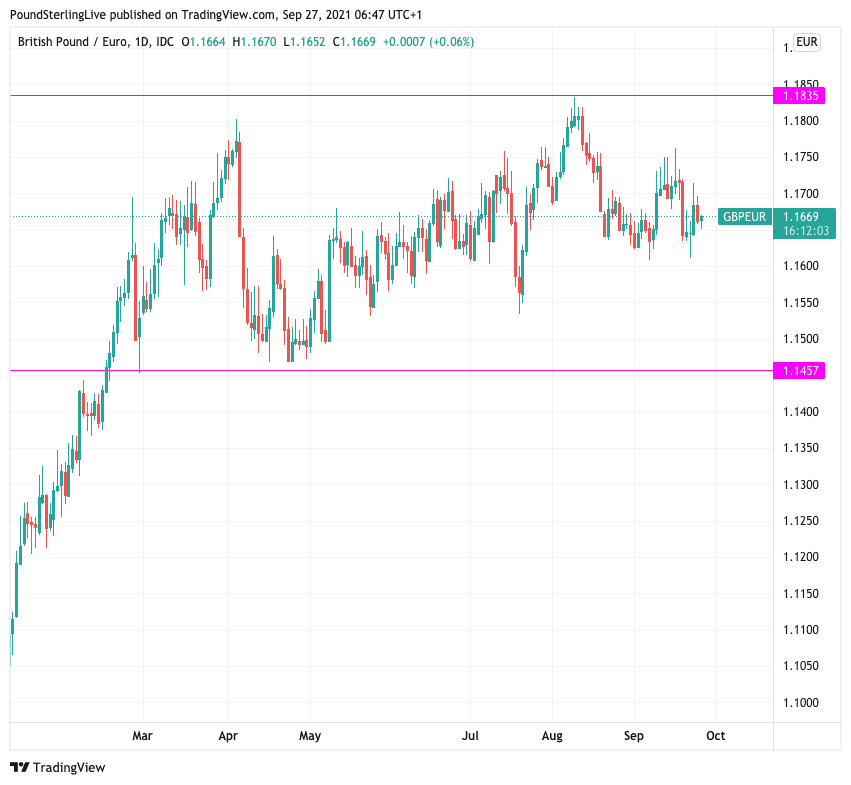

The Pound-to-Euro exchange rate starts the new week at 1.1660 which places it towards the middle of a range that it actually entered back in February and further moves sideways are likely in a week devoid of major economic data releases, although Germany's election will provide some initial talking points.

For the short-term, moves within this range are therefore likely to continue and only a decisive break of 1.1835 to the top or 1.1457 to the bottom would indicate a major shift is underway.

If anything, the below chart reveals price action is becoming more constrictive with weakness finding bids below 1.16 but a post-August 10 downtrend suggests strength will be limited towards 1.17.

Nevertheless, foreign exchange analysts at Goldman Sachs have notified clients recently they have revised higher their GBP/EUR forecasts and see 1.19 being possible by the end of the first quarter of 2022.

The decision rests to a great degree with expectations for a Bank of England interest rate hike to take place in the early part of 2020.

Ahead of the Bank's September 23 policy update, Goldman Sachs economists pulled forward their forecast for a lift-off in interest rates to May 2022 (the third quarter of 2023), which they expect to be followed by hikes every two quarters thereafter through the third quarter of 2024.

The decision reflects broader market expectations built during the course of recent months that rising UK inflation levels and a stronger-than-expected labour market would induce the Bank into a rate rise in 2022.

But market expectations have firmed further for an early 2022 hike after the Bank said last Thursday that "some modest tightening of monetary policy over the forecast period was likely to be necessary to be consistent with meeting the inflation target sustainably in the medium term."

"Some developments during the intervening period appear to have strengthened that case," the Bank said in a Statement.

The Pound rose on the day as UK bond yields rose to reflect expectations for interest rate rises, but the rub for Sterling bulls is that yields also rose in Germany and the U.S. at the end of the previous week as investors saw higher central bank interest rates elsewhere too.

This diminished any Bank of England fuelled boost to UK yields and Pound exchange rates.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

"We recently revised up our Sterling forecasts after our economists brought forward their projection for rate hikes following firmer inflation prints and strong labor demand, as well as some more hawkish BoE rhetoric about how to respond to those economic developments," says Michael Cahill, an analyst with Goldman Sachs.

The Bank of England went so far as to say that raising interest rates in 2021 was still not out of the question as they felt ending quantitative easing was not a requisite before interest rates can start.

The quantitative easing programme is expected to end in December.

"The BoE meeting this week confirmed that change in outlook, and if anything the risks to the first hike now appear to be skewed even earlier, with the MPC explicitly “ruling in” rate hikes this year, even if that seems fairly unlikely," says Cahill.

"Sterling should perform well against this backdrop," he adds.

Cahill does caution on expecting significant upside, however.

"We see three reasons to limit the enthusiasm on the currency’s upside," he says, "the BoE’s plan to more actively use its balance sheet in the normalization process will likely weaken the link between the policy outlook and currency performance somewhat."

The balance sheet utilisation referred to above is the plan set out by the Bank of England to ultimately reduce the stock of bonds it has brought up during its quantitative easing era.

This limits the need to raise interest rates, thereby denting some support the Pound might have expected from this avenue.

Goldman Sachs also observe the move higher in GBP/EUR over the last few months "has been largely a function of broad EUR weakness, which we expect to reverse as growth steadies".

"And third, Sterling remains a fairly cyclical currency, so we would be cautious on fresh long positioning while China worries are driving risk sentiment," says Cahill.

This final point is particularly relevant in the short-term: the Pound tends to underperform when global stock markets are struggling, as was the case last Friday.

A sell-off in global stock markets linked to a surge in global financing conditions was seen to be dictating currency moves ahead of the weekend.

Most major indices were in the red and 'risk off' or 'safe haven' currencies were benefiting as a result.

As mentioned earlier in this piece, UK, US and German yields all rose as markets priced in higher central bank interest rates in coming months.

This raises the cost of financing, with investors anticipating it to act as a headwind to growth and stocks suffered accordingly.

For foreign exchange markets currencies such as the Yen, Dollar, Franc and to a lesser extent the Euro, would tend to benefit against the Pound.

Goldman Sachs have nevertheless raised their Pound-Euro forecasts in anticipation of higher Bank of England rates to 1.19, in a six to twelve month forecast horizon, up from 1.1765 and 1.15 respectively.

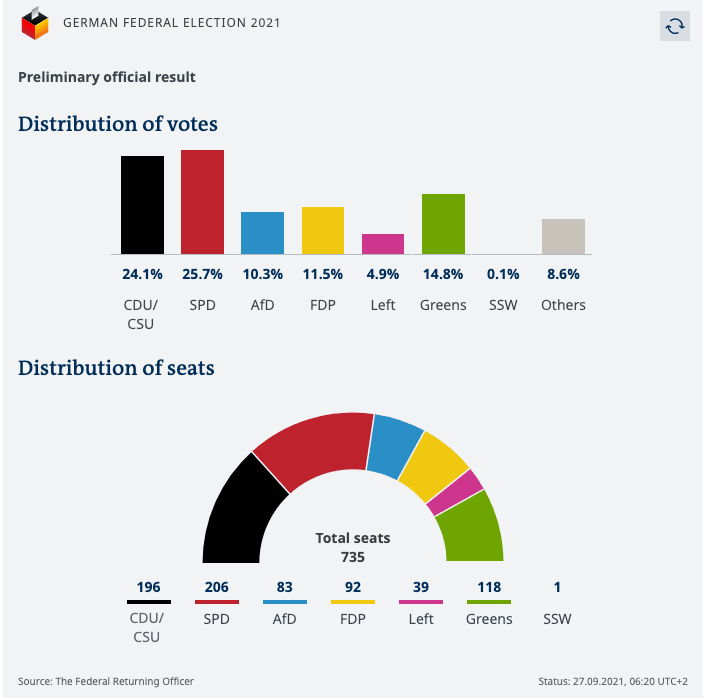

There is little on the calendar that is likely to bother the Euro and Pound this week, although Monday morning sees political commentators obsessing over the outcome of the German elections.

Media reports show the centre-left Social Democrats are ahead of the conservative CDU/CSU bloc by almost 2%, according to preliminary election results.

In such a tight race, the possibilities for a coalition are still unclear.

Preliminary results from Germany's federal election commissioner show the centre-left Social Democrats (SPD) at 25.7%, narrowly ahead of the centre-right Christian Democrats and their Bavarian sister party (CDU/CSU) at 24.1%,

Both blocs have said they want to lead the next government, and mathematically, either party could if they secure the necessary allies.

"A difficult government formation process will now start. Both SPD and CDU/CSU will try to lure over the Greens and FDP to their side. Although far from clear, SPD is expected to take the lead in negotiations as the they gained in the election to become the largest party," says Daniel Bergvall, Economist at SEB.

The foreign exchange market looks to be holding a relatively benign view of the event, as the result is largely consistent with pre-vote polling and now major surprise has been delivered.

"Naturally, the German election will take some headlines over the week, also for EUR/USD. That said, we do not expect a large and/or persistent market reaction in the spot," says Kristoffer Kjær Lomholt, Chief Analyst at Danske Bank.

Danske Bank last week updated their major foreign exchange forecast profiles and revealed they are opting to stick with a constructive view on Sterling.

They forecast the Pound-Euro exchange rate to be at 1.2050 by this time next year.