- EUR an outperformer following Jackson Hole

- Aided by hawkish comments from ECB governors

- Commerzbank see short-term GBP/EUR weakness

- But NatWest still prefer GBP to EUR

Above: ECB Board Member and Head of the Dutch central bank, Klaas Knot. Image © ECB.

- GBP/EUR reference rates at publication:

- Spot: 1.1644

- Bank transfers (indicative guide): 1.1336-1.1418

- Money transfer specialist rates (indicative): 1.1539-1.1580

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The British Pound fell to a fresh seven-week low against the Euro on the final day of August amidst a broad based rebound for the Eurozone's single currency, but can the new month bring with it a reversal in direction?

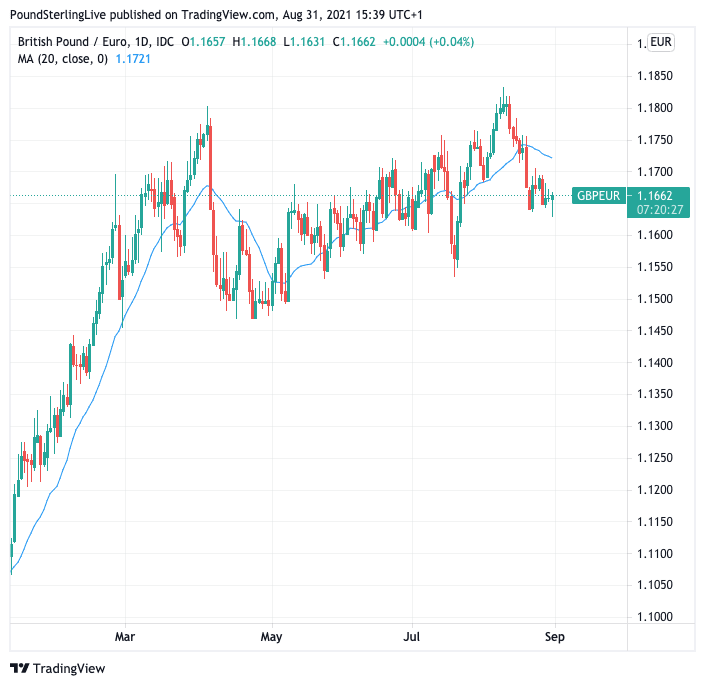

As September gets underway we note short-term trends are set pitted against Sterling: on August 10 the Pound-to-Euro exchange rate peaked at 1.18 where it was swiftly rejected for a second time in 2021, suggesting a significant resistance to levels above here.

The pair fell to 1.1629 on August 31, its lowest level since July 21.

Further downside in the Pound-Euro exchange rate is possible in the short-term says Karen Jones, Head of FICC Technical Analysis at Commerzbank, who notes the Pound-Euro exchange rate to be downside "corrective".

Above: GBP/EUR must break above the 20 day moving average (blue line) to turn positive once more.

Jones says she is maintaining a near-term downside bias and her studies allow for a move to 1.1600 and possibly to 1.1532, the July 2021 low.

The exchange rate is forecast to remain offered while below the 20-day moving average at 1.1724.

But the longer-term picture could yet remain supportive of Pound Sterling says Jones, noting that as long as support at 1.1465/52 holds she will assume a longer term positive bias.

The Euro is one of the better performing currencies in the post-Jackson Hole landscape, jumping against the Dollar and other currencies after Federal Reserve Chairman Jerome Powell stressed there was little need to rush into an interest rate hike once it had completed its quantitative easing programme.

The call caught the market by surprise as the Fed was expected to raise interest rates relatively soon after the completion of quantitative easing, which is expected to end around mid-2022.

Timing on interest rate hikes matters for currency markets, indeed it is arguably the most important driver of FX trends at present.

The European Central Bank (ECB) is expected to raise interest rates well behind the Bank of England and Federal Reserve, perhaps only in 2024, a dynamic that has offered support to the Dollar and Pound against the Euro over the course of the past year.

But signs that the Fed is in fact no rush to raise interest rates following Powell's Jackson Hole speech suggests the rate expectation gap between the ECB and the Fed is maybe not as yawningly large as previously believed.

This has seen some of the Euro selloff unwind, allowing the currency to advance against the Dollar and to a lesser extent, the Pound.

"With Fed officials now appearing to coalesce around a plan for only a slightly more rapid tapering timeline, and Chair Powell emphasising that rate hikes will face a “substantially more stringent test,” the outlook for the Euro now looks more balanced," says Zach Pandl, Co-Head of FX Strategy at Goldman Sachs.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

But it is not just the Fed dominating central bank debate as Tuesday saw two prominent members of the ECB's board saying the time for a reduction in extraordinary monetary support was nearing.

Klaas Knot said inflation levels in the Eurozone had risen to the level that warranted an immediate slowdown to stimulus, preparing a return to pre-crisis policy settings. (Inflation data out Tuesday showed Eurozone inflation had hit a ten-year high).

"I would expect a decision that should not be incompatible" with terminating crisis-era quantitative easing in March, Knot said. "That would imply a reduction in the purchase pace."

Governing Council member Robert Holzmann meanwhile said the ECB should soon start debating how it will phase out its pandemic-era stimulus.

"We are now in a situation where we can think about how to reduce the pandemic special programmes - I think that’s an assessment we share," said Holzmann.

The comments suggest the ECB might be prepared to move away from its ultra-dovish stance, and this can only be supportive of the Euro's outlook.

Foreign exchange analyst Paul Robson at NatWest Markets says he expects the Euro to remain resilient given the Eurozone "suddenly looks better placed than most on Covid trends and exit strategies."

He notes the EUR/USD has tracked relative growth expectations and there’s little for thinking this will change in the near future.

"So EUR/USD feels much better supported than it was at the beginning of the summer, even if a break higher seems unlikely near-term," says Robson.

"The outlook for EUR has clearly improved and will review those positions," he adds.

However, NatWest Markets remain of the view the Pound will also remains supported given the UK has a well-defined exit strategy from the Covid pandemic and the hurdle for another wave of restrictions seems extremely high, "which can play Sterling positive".

"While there will be periodic bouts of worry and hence volatility, we stay short EUR/GBP," says Robson.

NatWest have been backing the Pound against the Euro for the majority of 2021, a stance that has paid off given the 4.20% advance recorded by GBP/EUR since January 01.