Image © Adobe Images

- GBP/CAD spot rate at time of writing: 1.7345

- Bank transfer rate (indicative guide): 1.6741-1.6862

- FX specialist providers (indicative guide): 1.7088-1.7227

- More information on FX specialist rates here

- Set an exchange rate alert, here

The Canadian Dollar hit a speed bump Wednesday when lower-than-expected inflation data reinforced a correction against the U.S. Dollar and Pound, leaving the Loonie with a decidedly negative bias ahead of the all-important March Federal Reserve (Fed) decision.

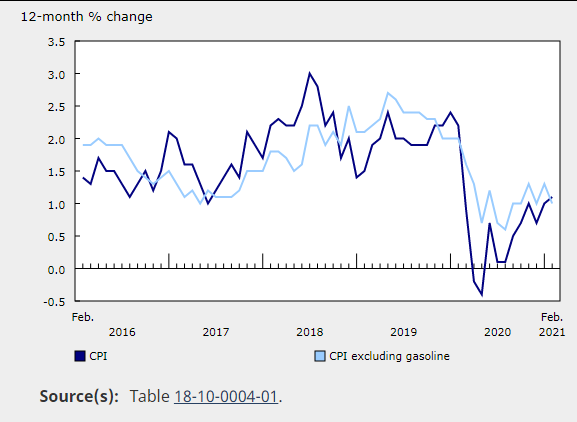

Canadian inflation rose 0.5% last month, Statistics Canada data shows, which less than the 0.7% anticipated by consensus and reflected a decline from the 0.6% increase seen in the New Year.

The year-on-year rate of inflation still edged higher however, from 1% to 1.1%, although this was largely the result of changes in gasoline prices and still left the overall rate of inflation far beneath the 2% target of the Bank of Canada (BoC).

After excluding gasoline prices from the data Statistics Canada says the annual rate of inflation was actually just 1% and down from 1.3% in January, in what could potentially be perceived by some investors as warranting a setback for the recently-outperforming Canadian Dollar.

"Both were slightly below expectations," says Royce Mendes, an economist at CIBC Capital Markets. "The trend in fuel costs should help push total annual inflation above the Bank of Canada's 2% target in March, potentially reaching 3% in April, given that they will be compared to the very weak prices seen in March and April of last year."

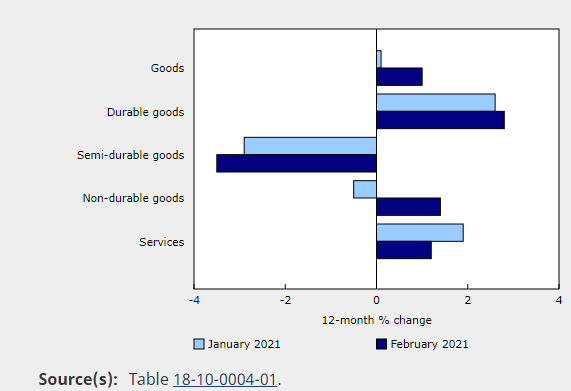

Statistics Canada graphs showing CPI & ex-gasoline CPI (left), and contributions to inflation in February (right)..

Wednesday's inflation data poses on the surface as a setback for the Canadian economic picture given that it's inflation pressures - usually in the order of a steady 2% average in the developed world - which central banks are attempting to cultivate with their monetary policies.

But sharp pandemic-inspired declines last year, supply chain disruptions and demand resulting from extraordinary public financial support for companies and households are all expected to stoke volatility in prices data up ahead. This is why Wednesday's inflation miss is, in the eyes of some economy-watchers, likely to give way to strong gains as soon as next month.

"Outside of energy prices, current inflation trends have been less worrying," says Nathan Janzen, a senior economist at RBC Capital Markets. "Concerns around inflation are less about current trends and more about the potential for a surge in household spending as the economy reopens."

The bottom line for the BoC and Canadian Dollar however is that any above-target inflation seen in the short-term is likely to be described as merely "transitory" and would be overlooked by central bankers rather than perceived as meriting interest rate rises or other moves.

Above: USD/CAD shown at 15-minute intervals with GBP/CAD (purple) and 10-year U.S. government bond yield (blue).

"The Canadian dollar is the best performing G10 currency on a year-to-date basis and the primary catalyst for this is the increasing speculation that the BoC will be perhaps the first major central bank to taper its purchases of assets this year (the BoC did taper last year)," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG. "Canada is also best placed to take advantage of the huge fiscal stimulus about to hit the US."

Canada's Dollar has become an outperformer among major currencies for 2021 and most notably in recent weeks due to expectations of a potentially supportive adjustment by the BoC to what is on at least one measure, the world's largest quantitative easing programme.

The BoC said last Wednesday that the raft of better-than-expected economic figures seen recently is now likely to mean the economy actually grew in the first quarter rather than contracting as it previously assumed. This in turn implies that Canada's economic recovery continued rather than going into reverse.

"We see it now as more likely than not that the BoC cuts the taper rate from CAD 4bn per week to CAD 3bn as a first step. Last week’s very strong jobs market report will be one factor helping encourage the BoC to take that step," says MUFG's Halpenny, who bought the Canadian Dollar this week when selling EUR/CAD. "Aggression by the BoC last year likely means that the reversal of that balance sheet expansion will likely be sooner than elsewhere."

Above: USD/CAD shown at hourly intervals with GBP/CAD (purple) and 10-year U.S. government bond yield (blue).

BoC guidance is that its maiden quantitative programme - which is on course to make the bank owner of nearly half Canada's expanded stock of government debt by year-end - will continue only "until the recovery is well under way." In other words, it could be high time in April for a second downward adjustment to the overall value of the BoC's weekly bond purchases from its current "at least C$4bn per week" to something like "at least C$3bn per week."

The latters is what some investors and analysts are now wagering on and not least because without this change the BoC wouldn't be too far away from a position where it's running out of government bonds to buy. This is the flipside of the BoC's uber aggressive bid to support Canada's government and economy as it grappled with the effects of the pandemic last year. The BoC has already reduced its purchases from an earlier amount of "at least C$5bn per week."

"The market narrative is so overwhelmingly positive that a downside miss was going to be hard-pressed to have much impact," says Andrew Kelvin, chief Canada strategist at TD Securities, who sees buying opportunities in shorter-maturity Canadian government bonds. "We continue to think BoC pricing is veering into the realm of wishful thinking, and we will look to add to our long front-end exposure as markets price an ever more aggressive tightening path."

USD/CAD was already paring earlier declines on Wednesday even before the inflation data hit the wires, along with the Pound-to-Canadian Dollar rate, although both edged higher following the report and were subsequently turning attention to Wednesday's 18:00 Federal Reserve decision.

Above: USD/CAD shown at daily intervals with GBP/CAD (purple) and 10-year U.S. government bond yield (blue).

The Canadian Dollar stalled on Wednesday with 10-year U.S. government yields at new highs above 1.66% ahead of the decision in which investors will be looking to assess the degree to which the Fed is comfortable with higher yields and what the risks are of it taking action if they rise too far.

Bond yields move in the opposite direction of prices so rising yields reflect government bonds being sold and vice versa. Some analysts say that stemming the sell-off in American government bonds could be done through rhetoric alone, although if this failed, the only alternatives would be a BoC-style reorientation of the existing $120bn per month quantitative easing programme so that it picks up more longer-term bonds or an increase in the overall size of it.

The Fed's response to rising yields - which are at least part driven by recently 'hawkish' market expectations that it could raise interest rates as soon as next year and end its quantitative easing programme even earlier - matters to the Canadian Dollar for various reasons including because of the impact that all of the above has had on the U.S. Dollar. The Loonie has risen alongside the greenback itself, against all other major currencies, so might be vulnerable if the Fed takes air out of the Dollar's tyres this week.

"The uptick in long-tenor interest rates is somewhat of a global phenomenon, although it seems to be US-led," says Greg Anderson, global head of FX strategy at BMO Capital Markets. "The yield spike has caused central banks such as the ECB, RBA and RBNZ to express discontent and to either alter their bond purchase programs or declare an intent to do so. Given the actions of those central banks, whether the Fed chooses to follow suit will be critical for EURUSD, AUDUSD and NZDUSD. Those are the pairs where we'd expect to see the most action today."