Australia is the largest iron ore producer in the world and it should therefore come as no surprise that the economy's wealth and the value of its currency depends heavily on the prospects facing iron ore.

Therefore the the outlook for this commodity could well be taken as a proxy for the outlook facing the Australian Dollar.

The country mined 825 million tonnes or iron ore in 2016; the next biggest producer was Brazil on 351 million – much of Australia’s iron ore is destined for China.

The price of iron ore is a major factor in the determination of the value of the Australian Dollar.

If the price of iron ore goes up as it has done recently the Chinese have to buy more Aussie Dollars to buy the same amount of it from Australia.

This increases aggregate demand for the currency which strengthens AUD.

The outlook for the price of iron ore is dependent on both supply and demand and these factors are constantly changing; a recent note by analyst Sue Trinh from RBC economics investigates some of these changes and attempts to forecast the future of both the commodity and its impact on foreign exchange.

Iron ore prices have rallied spectacularly in the last six months.

Iron ore futures contracts on the Dalian exchange in China, for example, have rallied 85% in six months, to a level of 848 yuan per metric tonne (122 bucks).

This has coincided with a sharp appreciation in the currencies of major producers.

Trinh asks whether these gains are sustainable and what factors if any might impact on them in the future.

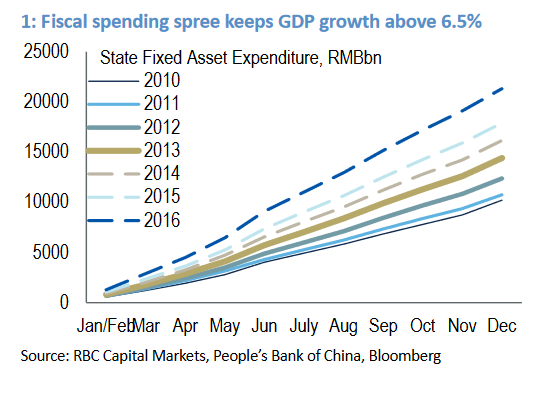

Public Spending Peaking

The resilience in demand for iron has come from China where the government increased public spending on infrastructure in 2016 (by 19.1% yoy) to offset a slowdown in GDP growth.

Trinh, however, is circumspect as to whether this will continue given public spending is already at historically elevated levels and accounts for 8.0% of GDP.

In her opinion this is unsustainable.

Supply and Demand Seesaw

The Chinese government has already tried to cap steel production in an effort to reduce pollution which reached record highs (up 80% yoy) in January, and if anything this push to de-industrialise is set to increase, not fall, limiting demand in its wake.

On the supply side, large producers such as Rio Tinto and vale have, “recently announced capacity additions and increased production levels this year,” said Trinh, suggesting there may be an oversupply problem on the horizon.

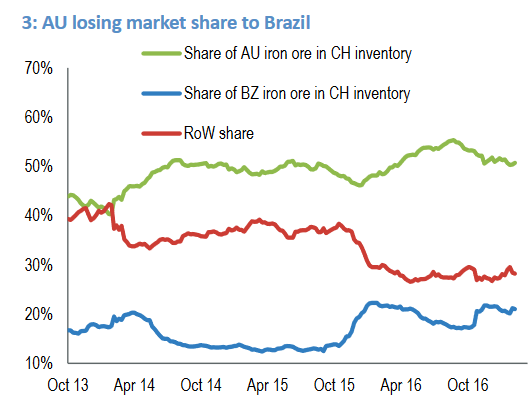

Brazilian Ore Preferable

The pollution problems in Beijing have led to increased demand for Brazilian iron ore over Australian.

This is because the Brazilian ore is higher grade and therefore doesn’t cause as much pollution.

This has already been reflected in recent trade figures showing Brazil’s share of iron ore imports to China rising from 17% to 22% and Australia’s falling from 55% to 51%.

This may also explain the sell-off in AUD/BRL in the last four months.

It does not bode well for the Australian Dollar if demand continues to increase for Brazilian ore over its own stuff.

Stockpiles can be Ignored

One major factor in the support of iron ore prices in general is that much of the inventories China possesses are unfortunately of the lower grade variety which they can’t use.

Normally high inventories mean lower prices as they indicate oversupply, however, this may not be the case for iron ore and is therefore worth considering when trying to anticipate where prices and AUD are headed.

Bursting the Housing Bubble

House prices are still on a tear, especially in Chinese tier one cities, however, they are rising at a slower rate as the authorities take increasingly more punitive measures to burst the bubble.

These are mainly to limit property speculation and involve a tightening of credit conditions as well as higher interest rates.

A huge amount of steel and iron is used in housing and construction and the continued efforts of Beijing to prevent the market from overheating are likely to impact negatively on iron ore demand, prices and therefore AUD.

Rampant Speculation

A part of the rise in iron ore prices have been caused by rampant speculation rather than fundamentals.

Purely speculative positioning is now 170% the size of deliverable future’s contract positioning, a rise from an average of 40%.

This indicates over almost two thirds of buying and selling is for speculative reasons alone.

This level of speculation is dangerous and un sustainable according to Trinh and may lead to a sudden dramatic sell-off if positions are suddenly unwound.

This therefore leaves the Aussie at risk and confirms that markets will continue to keep an eye on the Chinese-iron ore dynamic over coming months.

A notable improvement in this dynamic could well ensure the Australian Dollar continues its run of good form and appreciates further.