Strong Chinese PMI data and a steady hand being played by the RBA at their November policy meeting have seen the Australian Dollar outperform its rivals at the start of the new month.

The Australian Dollar is the currency to beat at the start of November.

Chinese Caixin Manufacturing and Services PMI data showed improvements in both sectors of the economy.

Manufacturing read at 51.2 in October, the fastest pace of improvement since March 2011 while Services PMI rose to 54.0 confirming growth in Australia's most important export market is picking up speed once more.

Meanwhile the RBA kept rates on hold and gave no hint at any further interest rate cuts which will certainly help cement Australia's superior yield to global investors which should support currency inflows and therefore the AUD.

The Pound to Australian Dollar exchange rate has fallen amidst the ubiquitous Aussie Dollar strength as is quoted at 1.5987.

The pair has been unable to break above a trendline which has kept price action pressured since the day of the flash crash.

The long, exhaustion bar which formed on the day of the flash crash may well have marked the lows of a major bottom:

A break above the 1.6125 highs would probably lead to a move higher to a target at 1.6240.

A break below the exhaustion bar lows would signal a continuation of the downtrend towards a target at 1.5500.

From a fundamental perspective, the Aussie Dollar is one of the currencies will the brightest outlook.

Recent inflation data showed prices rising at a faster pace than economists had foreseen.

This removed any lingering expectations the Reserve Bank of Australia (RBA) would have to cut rates any lower, and higher rates mean a stronger Aussie.

A sudden surge in the price of Iron Ore has also been a supportive driver for the Aussie which is forecast to strengthen in the future.

The main event for the Aussie this week is the RBA interest rate meeting on Tuesday November 1 at 04.30 London Time (GMT), although there is only a small chance of the RBA altering policy.

Retail Sales for September, released on Friday October 4 is expected to remain unchanged at 0.4%.

Latest Pound / Australian Dollar Exchange Rates

| Live: 1.9084▼ -0.13%12 Month Best:2.1005 |

*Your Bank's Retail Rate

| 1.8435 - 1.8511 |

**Independent Specialist | 1.8817 - 1.8893 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

The Pound: PMIs, Bank of England and High Court Challenge to Article 50

The key fundamental for the Pound is whether the Bank Of England (BOE) cuts interest rates any lower at its meeting on Thursday.

Markets appear to be attributing a roughly 50/50 chance to the possibility.

What will also be of interest are the changes made to growth and inflation forecasts in the Bank's Quarterly Inflation Report.

The Bank's forecasts could well hint at future policy decisions, particularly if they believe inflation will rise faster than previously anticipated.

The Bank will not tolerate inflation much higher than 2% and is expected to raise interest rates should this level be threatened.

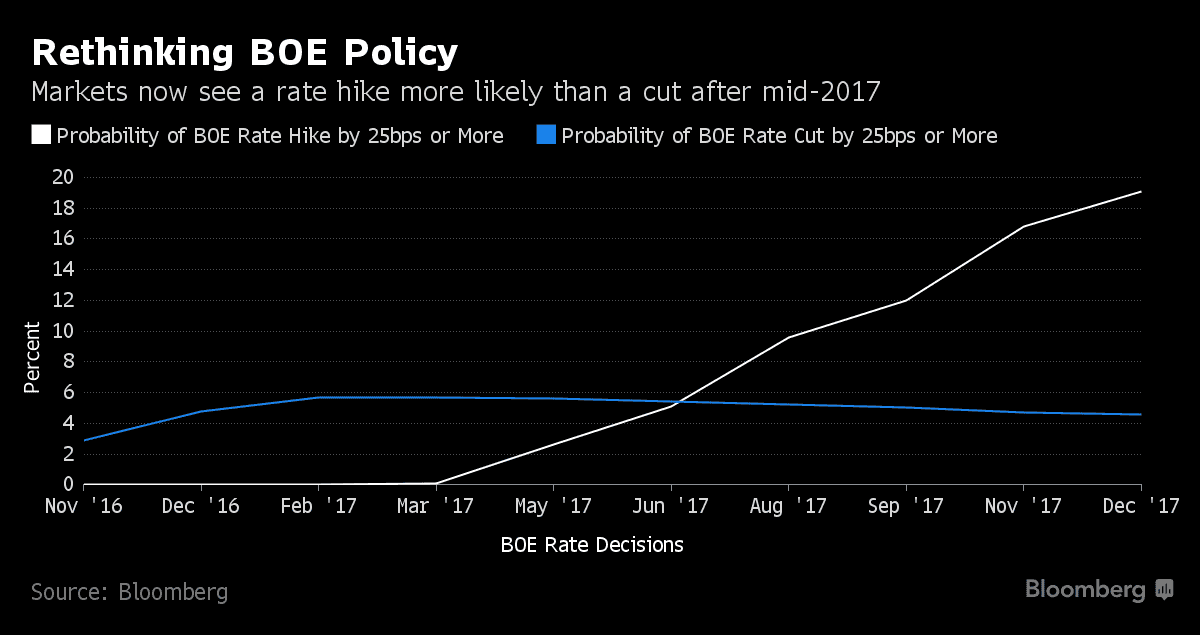

It is because of rising inflation expectations that markets are starting to price in higher interest rates in the future:

Overnight index swaps indicate that there is now more of a chance of an interest rate rise than a rate cut in 2017.

Rising interest rates are deemed to be supportive of a currency in that they attract capital inflows as global investors seek out yield. Clarity on Brexit, combined with rising interest rates, will be the ultimate catalyst for a longer-term and more sustainable Pound recovery.

Traders are re-evaluating how long monetary policy policy will remain accommodative following better-than-forecast economic growth data and BoE Governor Mark Carney’s suggestion two days ago that the prospect of faster inflation is diminishing the case for easing.

Carney also said the Bank would consider the impact of future decisions on the already weak Pound.

This suggests the BoE may hold fire for fear of weakening the Pound, which would make imports more expensive, and risk excessive inflation.

The other major theme for Sterling relates to the current high court challenge to the government’s authority to trigger Article 50 on its own without the agreement of parliament.

The failure of a similar challenge in a high court in Belfast is thought to have set a precedent which the London court is likely to follow.

If the challenge is unsuccessful the pound will fall; if not it will rally strongly.

It is not clear when the London court will make its decision.

The main data releases in the week ahead are the trio of October Purchasing Manager Indices (PMI) releases.

Tuesday, November 1 sees release of the final estimate for Manufacturing PMI for October at 10.30 GMT, which is expected to come out at 54.5 from a preliminary estimate of 55.4.

Construction PMI is out on Wednesday at 10.30 (GMT) and is forecast to moderate to 51.8 from 52.3.

Thursday sees the release of Services PMI at 10.30 (GMT), which is forecast to come out at 52.1 from a preliminary estimate of 52.6.