The Pound to Australian Dollar is biased lower on both fundamental and technical observations, but there is the prospect for consolidation in the GBP/AUD exchange rate over the near-term.

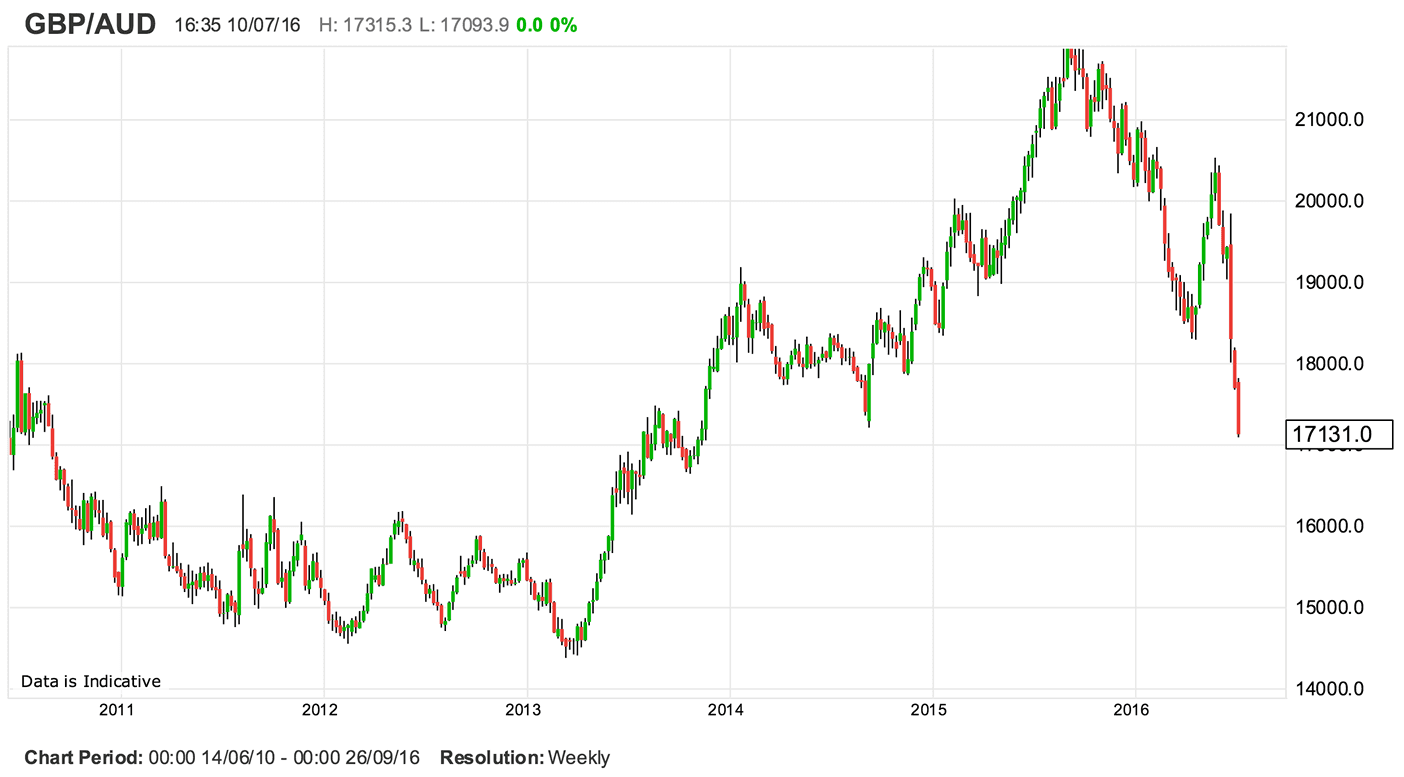

GBP/AUD is presently seen trading at 1.7226 with the pair having largely failed to bounce by the same margin as seen in other GBP pairs following the ascension of Theresa May to head of the Conservative party.

May takes the reins to the country on Wednesday ensuring one cloud of uncertainty hanging over the UK political-economic outlook is lifted.

Nevertheless, the Australian dollar was also boosted courtesy of a resolution to the Australian election.

It must however be noted that GBP/AUD could consolidate following the break-neck pace of recent declines.

In fact, we have observed the majority of key GBP-based pairs are now in oversold territory, largely owing to expectations of further Bank of England policy action being announced at their meeting due on Thursday.

Analyst Valentin Marinov at Credit Agricole says his sense is that the BoE will reiterate its readiness to smooth the market correction by providing liquidity but they maybe less likely to prop up asset prices via quantitative easing.

“We also expect the MPC to signal that the lower bound for rates will likely remain non-negative. Any BoE message that does not signal additional, aggressive easing would disappoint the dovish market expectations and may help GBP consolidate,” says Marinov.

There are therefore risks that the market has over-committed itself to further GBP/AUD weakness.

Latest Pound / Australian Dollar Exchange Rates

| Live: 1.9156▲ + 0.08%12 Month Best:2.1005 |

*Your Bank's Retail Rate

| 1.8504 - 1.8581 |

**Independent Specialist | 1.8887 - 1.8964 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

This could help the Pound to Australian Dollar exchange rate consolidate further with the obvious area for such a consolidation, from a technical perspective, being the 1.72 area.

This was the September 2014 low.

The pair also spent a considerable period around this area from July 2013 to September 2013.

Should a break of the lower-bound of the 2013 consolidation point transpire then a run towards 1-45-1.60 is invited.

We look at the 1.45-1.60 area as the long-term support that is likely to arrest the post-Brexit fall noting that it provided solid support to Sterling from 2010 right through to 2013.

The market is therefore structurally supportive to Sterling at these multi-year lows.

Bank of England Tipped to Provide Next Big Move

Sterling has been sold heavily since the EU referendum results were announced and analysts continue to advocate for further declines based on the observation that the Bank of England is likely to cut interest rates, perhaps as soon as Thursday the 14th of July.

Governor Mark Carney has suggested that in his opinion the deterioration in economic confidence following the UK’s decision to exit the European Union in the June 23rd referendum warrants a policy response over the course of the summer.

The most obvious policy response would be a cut in the Bank’s base rate from 0.5% to 0.25%. A potential cut to 0% before the year ends is also possible.

"The drop in the pound has been driven by a substantial shift in expectations for UK interest rates. We expect Bank Rate to be cut by 25 basis points in next week’s MPC announcement (14th July) and wouldn’t rule out a further cut to zero or a ramping up of the Banks’ quantitative easing in subsequent meetings," says Scott Bowman, UK Economist at Capital Economics.

Lower interest rates imply lower returns to international investors, who pare back their supply of money into the UK economy.

This in turn undermines support for the British Pound against the Australian dollar.

Consider that the UK could soon face a basic interest rate of 0.25%, or below. Consider too that Australia currently has a 2% rate of return.

The prospect for huge GBP into AUD flows on this basis alone remains elevated and should keep the exchange rate under considerable pressure going forward.

Arguably, a 0.25% cut has already been absorbed by the GBP, therefore any further weakness will have to emanate from a surprise announcement, either on Thursday or coming months.

The questions are, essentially, will the Bank cut rates below 0.25%, and will the Bank expand quantitative easing?

“In our base case scenario, we expect the BoE to cut the Bank Rate to zero (currently 50bp) and to deploy a new quantitative easing program: our baseline is for the BoE to aim at an increase in the stock of the Asset Purchase Facility (APF) programme by £100-150bn from the current

£375bn,” say Barclays in an economic briefing to clients.

Barclays expect the rate cut to be announced at the August meeting alongside the Inflation Report, while a decision of a potential APF addition could take longer.

The BoE has been fast to react to the vote outcome, having already reversed its earlier decision to raise the counter-cyclical capital buffer to 0.5% of risk-weighted assets by March next year.

This macro-prudential measure should further help support credit

from the supply side which should in turn keep the economy moving forward as firms are able to grow on the basis of lowered borrowing costs.

In addition, Barclays reckon the BoE could potentially deploy targeted funding for lending schemes, if credit supply was to freeze up in the coming months.

The future path of policies would then be heavily dependent on ongoing levels of uncertainty, data responses, financial stability concerns and the behaviour of the exchange rate.

The mix of the above will determine just how far the GBP falls.

An August Interest Rate Cut at the RBA?

We have mentioned that AUD should remain supported by demand for exposure to the country’s superior 2% interest rate at the Reserve Bank of Australia (RBA).

But, what if this rate were to be cut in the near future?

The implications for the Australian Dollar’s outlook are notable as a cut would presumably limit downside, but not reverse, GBP/AUD.

It would certainly prompt the AUD/USD to decline, particularly if we consider the US Federal Reserve may be looking to raise interest rates again before the end of 2016.

At their July policy meeting the Reserve Bank left the cash rate unchanged at 1.75% and reinstated an explicit easing bias in its post-meeting press release.

The Bank noted, “over the period ahead, further information should allow the Board to refine its assessment of the outlook for growth and inflation and to make any adjustment to the stance of policy that may be appropriate”.

“Although this stopped short of the language previously used by the Bank when signalling a rate cut at the next meeting, we still expect a 25bp rate cut to 1.5% on 2 August,” say ANZ Research in a client briefing.

This is when Bank staff will present an updated economic outlook to the Board in the wake of the Q2 CPI on 27 July (the outlook will then be published in the Statement on Monetary Policy on 5 August).

Notwithstanding stronger-than-expected growth in GDP in Q1, we think that the updated outlook will continue to show underlying inflation remaining below the 2-3% target band for an extended period.

“With inflation remaining persistently low, we think that the recent spike in uncertainty will push the RBA over the line to cut rates in August,” say ANZ.