The Aus Dollar is likely to maintain its advantage against sterling but we hear a number of strategists say they are stepping back from backing the currency against the US dollar.

The latest set of RBA minutes showed policy makers are likely to remain spectators to developments in the Australian economy for months to come allowing the Australian currency to remain dictated to by external drivers.

AUD fell against 7 G10s and slipped 0.39% to 0.7111 against USD, led by broad-based weakness in commodity majors. Strategists tell us they are now cooler on AUD/USD's prospects over coming days, as highlighted further down in this piece.

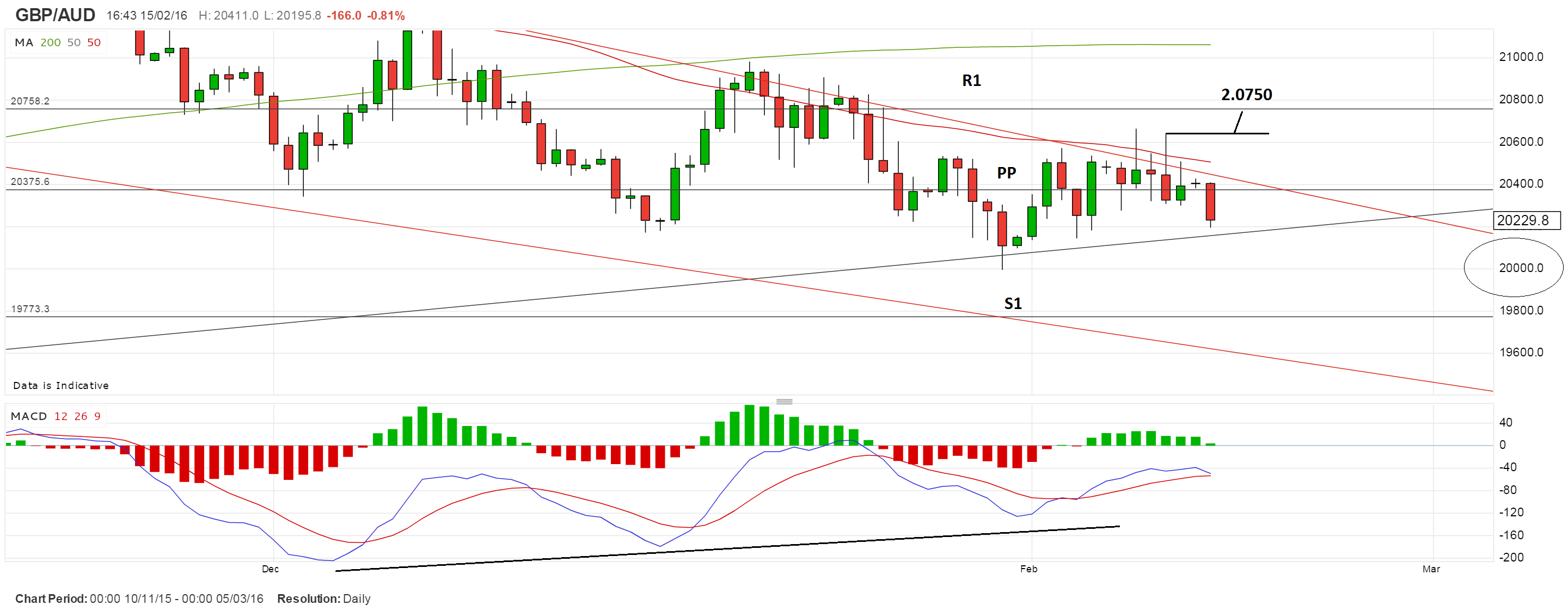

The pound to Australian dollar exchange rate is meanwhile seen trading at 2.0122 and has been in decline since the 9th of February.

Bank transfers are being offered at a rate of around 1.9555 while independent providers are quoting rates higher towards 1.9876.

Société Génerale’s Kit Juckes confirms that when it comes to the central themes influencing GBP/AUD this week, "sterling remains vulnerable to Brexit polls," while for the AUD and NZD are exposed to, "the remorseless slowdown in China, regardless of recent optimism.”

Looking at the charts we see the outlook for the pound to Australian dollar exchange rate is broadly balanced, except for the big bearish candle which formed on Monday 15.

This long red down-day does not bode well for the pound, however, there is a substantial amount of support underpinning the current level, including a major multi-year trend-line at 2.0168, the 2.0000 psychological level and then the S1 monthly pivot at 1.9773.

These all lie in the way of a continuation lower and would need to be clearly broken to expect a continuation.

In addition, the MACD indicator at the bottom of the chart, which is a momentum indicator, has converged on three occasions in a row – a very bullish sign despite the lack of follow-through from price action itself.

A strong break higher, confirmed by a break above the 11 Feb highs at 2.0645 would be likely to confirm a continuation up to a target at 2.0750 where the R1 monthly pivot is situated.

Latest Pound / Australian Dollar Exchange Rates

| Live: 1.9277▼ -0.01%12 Month Best:2.1005 |

*Your Bank's Retail Rate

| 1.8622 - 1.8699 |

**Independent Specialist | 1.9007 - 1.9084 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Fade Aussie v US Dollar Rallies

Strategists have cooled their optimism on the AUD to USD of late having used the pair as a vehicle to express negative sentiment against the US dollar.

"AUD is now bearish against USD as risk-off sentiment continues to dominate the markets. As noted yesterday, failure to close above 0.7156 has opened up a drop back to 0.7072; below this, expect AUDUSD to test 0.70," forecast Hong Leong Bank in a strategy update to clients.

“While the currency has helped to offset falling commodity revenues, until we can confidently call a bottom in the commodity downtrend it remains hard to suggest the AUD has reached a trough," says Jeremy Stretch of CIBC Capital Markets, "For now we would continue to look to fade AUD to USD rallies up to 0.7150.”

Also turning shy on the AUD is professional trader Sean Lee at Forextell. Lee has been a buyer of AUD/USD dips for some time but says he is losing that bullish feeling:

"I’m certainly not bearish, don’t get me wrong, and I do think we are very close to a base, but the price action tells me that we may see a few more nasty clean-outs on the downside, especially if AUD/JPY gets hit hard again.

"Cable still looks to me as if it can quite easily trade below 1.40 and if that happens, it’s hard to imagine the AUD/USD going up in a straight line.

"I reduced my AUD/USD longs on Friday and will sit back and see what the market does early this week."

RBA Minutes: Risks Tilted to Lower Rate

The RBA Minutes released on the 16th of February confirmed that the Bank is watching global developments closely while showing a contentment with the trajectory of the domestic economy.

There is no strong indicator that decision makers will be prompted into another interest rate cut based on Chinese-inspired market tremors.

The Board also seem quite confident in the ability of household consumption to help drive the recovery, noting once again the positives of low interest rates, low petrol prices, and an improving labour market.

"While we also see consumer spending growth improving, we think the Bank’s forecast for household consumption growth to accelerate to 3½% or above seems overly ambitious in an environment of low wage growth, slowing house price growth, and skittish consumer confidence," says Felicity Emmet at ANZ Research.

RBA Governor Stevens used his semi-annual Parliamentary testimony to downplay any domestic bank funding concerns.

In terms of monetary policy he maintained that the Central Bank maintain a bias towards easing, due in large part to a benign inflation backdrop. However, they remain in no rush to cut further, not least as this would merely stoke additional concerns in relation to elevated consumer leverage.”

ANZ say they are biased towards lower interest rates in 2016 as they believe ongoing low inflation and softening demand conditions will force the hand of the Bank.

Striking a more pro-AUD tone are Citibank who note so far the tightening in global financial conditions is consistent with slower global economic growth rather than recession, but the risks are to the downside given the speed of recent moves in financial markets and heightened level of risk aversion.

"Despite this, our measure of Australian financial conditions has been relatively steady as the effects of risk aversion have been matched by lower oil prices, currency stability and low borrowing rates," says a foreign exchange briefing from Citi.

Citi’s Australian FCI is consistent with growth slightly below potential at around 2½%, which will help argue the case for no further RBA rate cut.

Aussie Jobs Data Ahead

Employment, meanwhile has been something of the ‘jewel in the crown’ of the Australian Economy of late, as it has fallen to 5.8% where it has remained in both November and December.

The next set of figures for January is set to be released on Thursday and this will give us a better idea as to where the economy is headed.

Consensus expectations are for figures to remain unchanged at 5.8%.

Trading Economics forecast a drop to 5.7%, if so this may provide support to the Aussie, but it seems that as far as factors shaping monetary policy go, employment is losing its previous influence, given stagnant wage growth.

TD Securities expect jobs data to retract after a strong run in which employment take-up has exceeded vacancies, and they expect a rise in the participation rate to increase unemployment a basis point to 5.9%:

“Employment has overshot job vacancies in recent months, so we expect a small +5k.

“Raw data is a big negative (-215k) but the 6yr ave (sa) is +25k, so +5k is weaker than “average” after a strong 2015, but more consistent with job vacs.

“Assuming a small uptick in the participation rate to 65.2% increases the unemployment rate to 5.9%.”

As far as the RBA is concerned the rate of the Aussie is not something that is targeted, however the central bank retains the flexibility to ease further and indeed Governor Stevens hinted that it may be appropriate.

He added that he anticipated further depreciation of the Aussie as the impact of the CPI figures work their way through.