Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

Image © Adobe Images

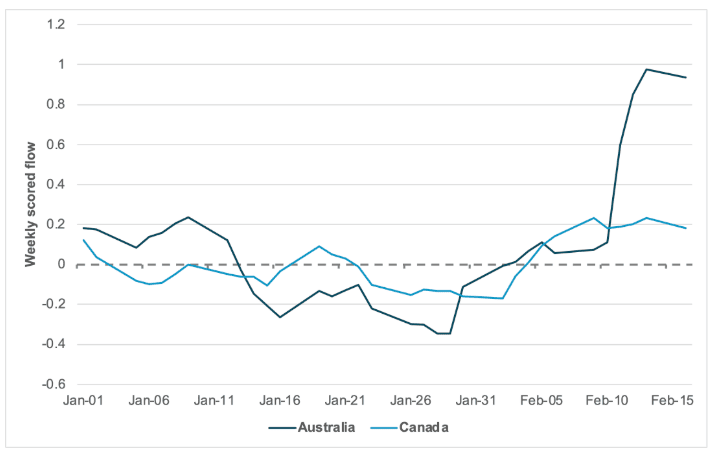

The Australian Dollar is drawing fresh support from a surge in demand for cash and short-term instruments, according to new flow analysis from BNY Mellon, which shows statistically rare inflows into Australia’s front-end rates market.

BNY Mellon’s proprietary iFlow data indicates that weekly flows into Australia’s CAST segment – cash and short-term instruments – have reached magnitudes typically associated with event risk or structural re-pricing, suggesting investors are actively reallocating capital toward Australian short-duration assets.

"FX markets are showing little reluctance to price in policy pivots where justified by inflation. Flows are even more forceful when hawkish expectations are endorsed by the relevant policymakers. Presently, Australia is the clearest case of G10 tightening," says Geoff Yu, EMEA Macro Strategist at BNY Markets.

CAST refers to institutional allocations into highly liquid, short-dated instruments such as Treasury bills, money market paper and other cash equivalents, which large global investors use to park capital while earning yield and maintaining flexibility.

Unlike longer-dated bonds, CAST instruments carry minimal duration risk, meaning they are less sensitive to moves in long-term yields, making them attractive when yield curves are steepening or volatility is elevated.

BNY Mellon’s iFlow system tracks actual cross-border transactions passing through its custody and settlement network, offering insight into real money flows rather than survey data or speculative positioning.

When iFlow's CAST reports a flow magnitude of 1.0 or higher on a standardised basis, as it has for Australia, it signals a statistical surge in capital movement, typically reflecting either a major macro event or a meaningful shift in rate expectations.

Image courtesy of BNY.

"CAST flows tend to be highly sensitive to G10 rate differentials. We have identified several candidates already, but only Australia is responding forcefully," says Yu.

In Australia’s case, BNY Mellon says the inflow reflects a re-rating of the country’s interest rate outlook, with markets increasingly pricing the possibility of further policy tightening if inflation remains persistent.

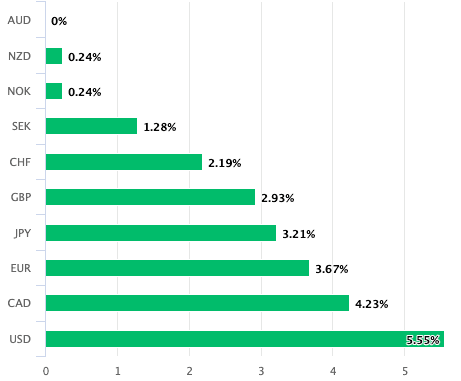

The RBA raised interest rates on February 03 and Governor Michele Bullock verified market expectations that further hikes are possible. The move helped the currency extend its outperformance, keeping it firmly anchored at the top of the G10 leaderboard for 2026.

She warned Australia may face structurally higher inflation and therefore higher-for-longer policy settings.

That surety matters for global capital.

"After Governor Bullock’s recent speeches and testimony, Australia’s cash and cash equivalents market appears to have received the message on interest rates," says Yu.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

Short-term flows are particularly sensitive to interest rate differentials across the G10, and Australia’s relatively high policy rate, combined with deep liquidity and a well-developed money market, creates an attractive carry profile.

Carry dynamics refer to the strategy of borrowing in lower-yielding currencies and investing in higher-yielding ones, capturing the spread while managing currency risk.

When the yield is available in liquid, short-duration instruments, the trade becomes more appealing because investors can earn income without taking significant bond price risk.

BNY Mellon notes that other G10 candidates, including Japan, Canada and New Zealand, have not attracted comparable cash inflows, reflecting either credibility questions, economic uncertainty or limited market depth.

Above: AUD in 2026.

Australia’s combination of yield, liquidity and policy clarity therefore stands out.

The surge in CAST flows also coincides with a cautious global risk backdrop, where investors have shown a preference for reducing exposure to equities and longer-dated bonds while preserving income.

In such environments, capital may rotate from equities into domestic cash instruments rather than being repatriated, helping to stabilise and support the currency.

For the Australian Dollar, the implication is that institutional demand for high-quality, short-term Australian assets is providing an underlying bid, reinforcing the currency’s resilience even amid broader market volatility.

If inflation data continue to justify a firm policy stance, and the RBA maintains its credibility, the carry advantage embedded in Australia’s front-end rates market could remain a structural tailwind for the AUD.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →