Image © Pound Sterling Live

The warning from economists is clear: inflation risks remaining stubbornly high in an unreformed economy.

Oxford Economics has just hiked its inflation forecast for 2026, a warning that the current spell of disinflation is not as sustaining as it first appears.

The upgrade, accompanied by the warning "the path for inflation this year is likely to be a little stronger than we previously forecast," follows another undershoot in the official monthly inflation series.

The ONS on Wednesday reported the headline CPI inflation rate fell to 3.0% in January from 3.4%. The trend of late has been undeniably positive for households, businesses and an under-pressure Chancellor, Rachel Reeves.

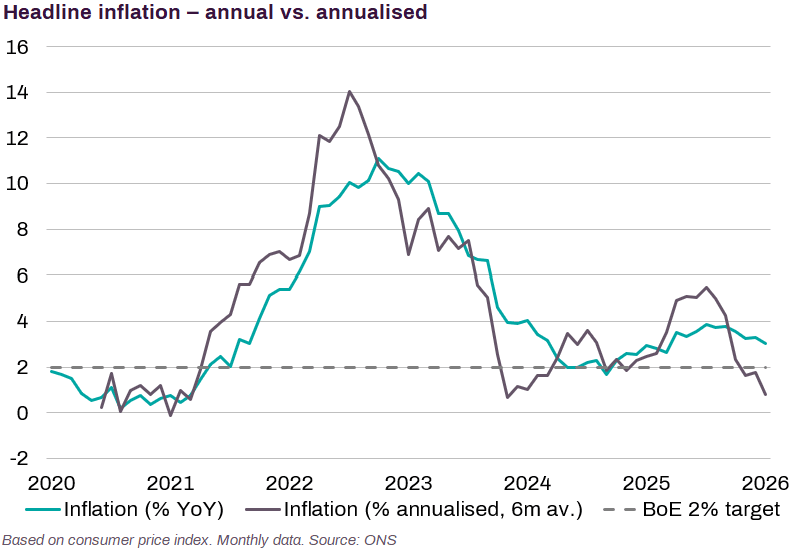

As Kallum Pickering, economist at Peel Hunt, points out, there's been a quickening in the disinflation trend:

"Looking at annualised data, which gives a better measure of current price pressures, the BoE is now undershooting its target. Given known lags with monetary policy, the clear risk now is that the bank has fallen behind the curve and will need to play catch up - skewing risks towards more than the two cuts money markets see for this year," he explains.

Above: When you annualise the inflation data, we see near-term momentum is to the downside. Image: Peel Hunt.

The Bank will play catch-up with the data; markets now see a cut in March and at least one more this year. The odds of a third have risen notably this week.

Economists, and the Bank of England itself, see a big moment for the economy in April when CPI inflation is expected to fall to the 2.0% target.

But for a 'job done' moment at Threadneedle Street, of which the European Central Bank has been enjoying for months now, inflation must stay here.

And it's the sustainability of inflation at 2.0% that has economists nervous.

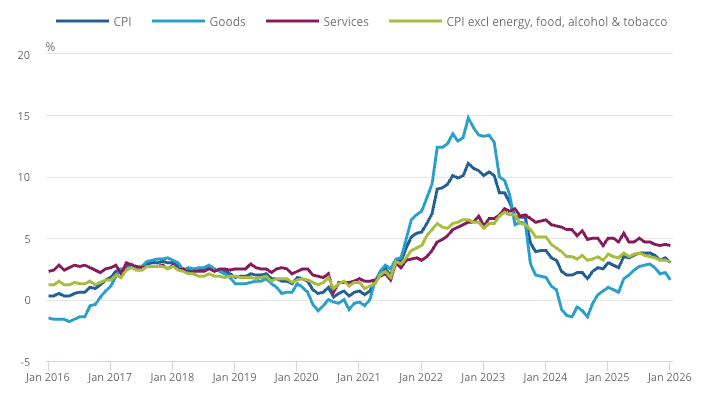

Nikesh Sawjani, Senior UK Economist at Lloyds Bank, says the problem for the Bank of England 'doves' is that core and services inflation both edged lower by just 0.1 percentage point, to 3.1% and 4.4% respectively in January.

This means they are actually tracking 0.2pp and 0.3pp above the Bank of England’s forecasts.

"While we still expect the headline rate of inflation to drop to around 2% in April, stickiness in underlying measures is likely to remain for some time still," says Sawjani.

Above: Unless services inflation falls further, a sustained headline CPI rate at 2.0% is difficult to achieve.

With services inflation stubbornly resistant to decline, it will be difficult for inflation to settle at 2.0% on a sustained basis.

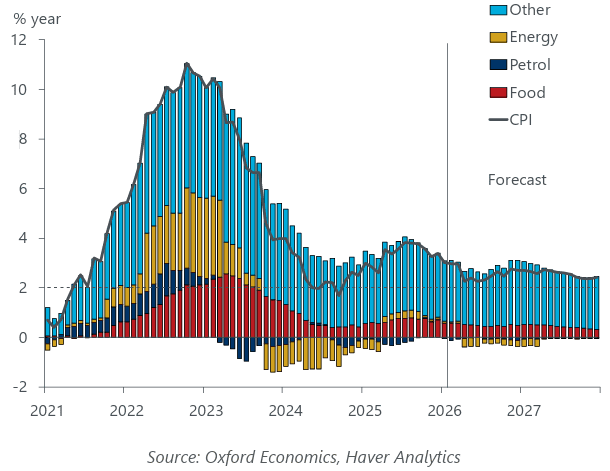

Indeed, there's been a lot of statistical tailwinds behind January's drop to 3.0%, with unfavourable rises a year prior falling out of the comparison. That will happen more as we approach April.

"We expect inflation to fall sharply in April, due to smaller regulatory price rises than last year, a lower energy price cap, and the impact of measures announced in the 2025 Budget," says Edward Allenby, Senior Economist at Oxford Economics.

But there's a risk that the fall turns out to be illusory owing to statistical 'resets'.

In fact, Oxford Economics raised its UK inflation forecasts following Wednesday's figures: "incorporating new 2026 regulatory price announcements made over the past month and the annual update of the weights for the inflation basket means we now forecast CPI inflation to be slightly higher in 2026 and 2027."

"The path for inflation this year is likely to be a little stronger than we previously forecast," he adds.

Oxford Economics now sees CPI inflation averaging 2.6% this year and next, up from 2.3% and 2.5% previously.

If the call is correct, the implication is that the Bank of England has a limited window in which to lower rates, before it confronts upside surprises in the data again.

Tommy von Brömsen, FX Strategist at Handelsbanken, says UK inflation will rise again by the year-end with persistence re-emerging as a challenge for policymakers, meaning the Bank of England is likely to keep policy relatively tight compared with several peers.

"This keeps front-end rate differentials elevated and provides cyclical support for GBP through the carry channel," he explains.

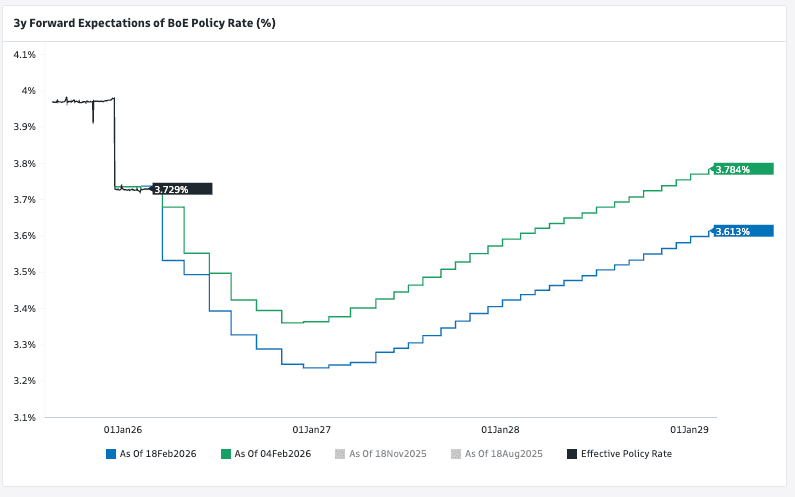

Analysts at JP Morgan see two more rate cuts this year, confirming a limited window for the Bank of England to act.

"Our economist sees a terminal of 3.25% by June, whereas markets price that by year-end. An additional cut could be brought forward into H1, but it will be hard for BoE to ease much more than that with neutral around 3%... This puts a floor under BoE driven GBP weakness in our view," says JP Morgan's FX strategy team in a new note.

Above: There's been a notable fall in expectations for the future path of Bank Rate in February as investors react to 'dovish' data.

The IEA - the independent economic think tank - points out that business surveys suggest that underlying cost pressures remain sticky, and medium-term inflation expectations "are still too high for comfort."

Julian Jessop, Economics Fellow at the Institute of Economic Affairs, says growth in the UK's broad money supply is running at annual rates of around 5%, which is at the upper end of the comfortable range.

"This could mean that inflation just pops up somewhere else in the economy where prices are not being capped," he explains. "There is also danger that inflation does not fall as far as expected, or that it does not remain lower for long."

The IEA says the real problem the UK economy faces is a lack of supply to meet demand. To address this it urges the government to take measures that will allow the private sector to grow and become more productive.

"The government should refocus on getting the supply side of the economy right, freeing up markets to provide goods and services at lower prices across the board. In turn, this should ensure that more of the growth of the money supply is reflected in an increase in economic activity rather than higher inflation," says Jessop.