- Rand could take a hit from worsening geopolitical situation and rising oil prices

- High foreign ownership of South African debt makes it sensitive to global forces

- Rising oil prices also present risk to South African unit

© moonrise, Adobe Stock

The threat of deepening geopolitical tensions in the middle east after Trump's decision to pull out of the Iran deal has led to a rise in oil prices and widespread financial market risk aversion.

Both these factors are potentially negative for the South African (SA) Rand, according to Zaakirah Ismail, fixed income strategist for South Africa at Standard Bank.

Rising oil prices make petrol more expensive which pushes up inflation.

High inflation expectations then reduce demand for SA bonds because of the higher inflation erosion, and since a large portion of the SA bond market is foreign, a reduction of the outside demand for SA Bonds also equals a reduction in demand for the SA Rand.

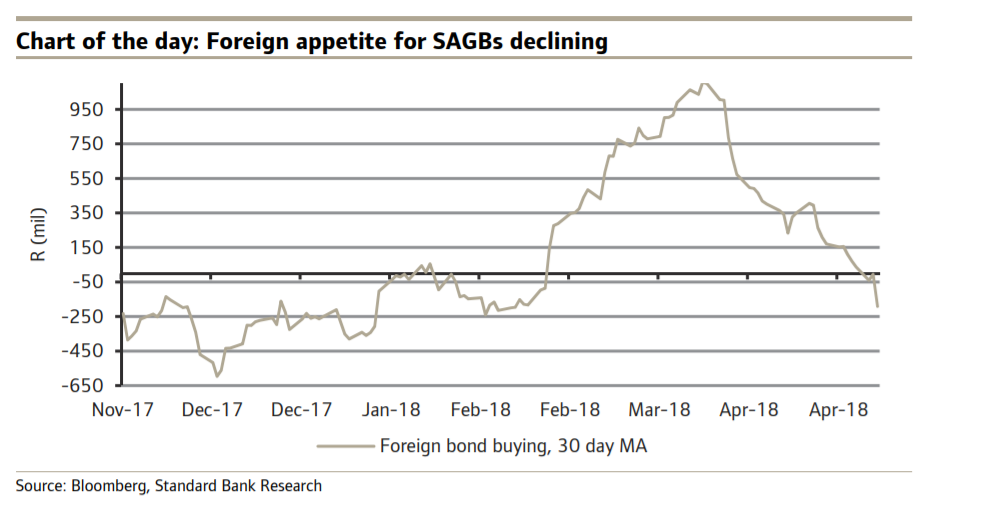

"Foreign holdings of SA’s government bonds (SAGBs) account for over 40% of SA’s total bonds," says Ismail.

"Therefore, a flight of foreign capital, out of SA, puts upward pressure on bond yields – and leads to rand weakness," adds the strategist.

"Given the current volatility in the market, foreign appetite for SAGBs has been waning," she says, adding, "foreign bond buying this week has declined at the fastest pace since October 2017, with R9.4bn worth of SAGBs sold by foreigners this week alone."

But higher oil prices are not just a dampener for the bond market, they are also a problem for the trade deficit as SA has to import most of its oil.

A major exporter of other commodities including precious metals, this is especially true if the price of oil is rising unilaterally.

"Higher oil, in the long run, is negative for the rand from a trade balance perspective – unless it goes alongside a rise in other commodity prices. However, commodity prices have come under pressure, as the dollar’s broad-based strength has been dominant," says Ismail.

The price of oil could push even higher amidst ongoing conflict in the middle east.

"There’s potential for prices to push through US$80/bbl in the short term, but this hinges on Europe and Iran’s stance on the nuclear deal as well as any secondary penalties imposed by the US," Mpho Tsebe Rand Merchant Bank (RMB).

The latest news is that tensions with Iran have reached a new peak after Israel and Syria started trading missiles, and the missiles from Syria appear to be Iranian.

If geopolitical tensions continue ratcheting up it could have longer-term negative consequences for market risk sentiment which could also weigh on the Rand, regardless of the impact from oil prices.

The Rand, like most emerging market currencies, is seen as a risky asset so when risk aversion sets in it tends to weaken because investors pull out and seek safer positions.

This is especially pertinent to SA bonds which have a high foreign ownership component.

"A key risk for local bond yields (in terms of what is priced, or not) is a broad EM sell-off, similar to what we are seeing now. We still think, however, that SA is well placed to withstand foreign selling of assets – but not sustainably so, if it continued," says Ismail.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.