© DragonImages, Adobe Stock

There are signs the outlook for the Pound against the South African Rand are turning more constructive, are there more gains to come for the exchange rate?

The GBP/ZAR pair has bounced strongly and the young recovery seems to be raising questionmarks over the established downtrend.

The rebound came as a result of the US Dollar rising, since Rand is highly negatively correlated to the US Dollar, due to the high amount of US debt held by South African companies.

The previously bearish chart is looking more neutral now after the exchange rate broke above the major downsloping trendline drawn from the 2017 highs, a sign analysts interpret as particularly bullish.

The four hour chart provides more bullish evidence in the form of a rising sequence of peaks and troughs which confirms the short-term trend has now probably changed to 'up'.

Two major obstacles stand in the way of further gains, however, in the form of the 200-4hr MA at 16.55 and, more importantly, the 50-day MA at 16.63.

Currently we are neutral and waiting for more bullish signals to confirm the change of trend.

GBP/ZAR has been downtrending for a long-time and we require more confirmation to make a bullish forecast.

Data and Events to Watch for the South African Rand

The main data releases for the Rand in the week ahead are for manufacturing and mining.

Manufacturing production is forecast to show a 0.2% rise month-on-month in February from 1.1% in the previous month, when it is released at 11am on Tuesday, March 13.

Mining Production is forecast to show a 1.0% rise in January compared to the previous year when it is released on Wednesday at 9.30. This would compare favourably to the 0.1% rise in January 2017.

Gold Production for January is also released at the same time, as is Business Confidence.

Of the outlook for the week ahead, Rand Merchant Bank analyst Isaah Mhlanga and Mpho Tsebe, say the following:

"Locally, the focus will be on mining and manufacturing data this week, as well as the business confidence index. Markets expect production data to show an upward trajectory and for sentiment data to align with hard data. This comes after fourth-quarter consumer and business confidence tracked sideways; while national accounts data showed a strong recovery in consumption and investment growth."

Data and Events to Watch for the Pound

The main event for the Pound in the week ahead is probably the Chancellors’ Spring Statement, this is a new initiative brought in by Philip Hammond to provide an update on the economic and fiscal outlook.

No changes to the budget are expected and the statement is only scheduled to last 15-20mins, according to media reports, which is only a rump compared to the Autumn statement.

Budget's do not often move currencies so the Pound may not react, however, alongside the statement are revised forecasts from the Office of Budgetary Responsibility (OBR) which if substantially altered may impact on growth prospects and therefore Sterling.

The OBR has, on balance, been overly pessimistic in the past, generally undershooting with its forecasts and leading some commentators to expect it to revise up its forecasts on Tuesday.

"It is always difficult to predict other institutions’ forecasts. However in terms of the Spring Statement, we would expect the GDP growth projections to be a little more upbeat," says Ryan Djajasaputra, analyst at Investec.

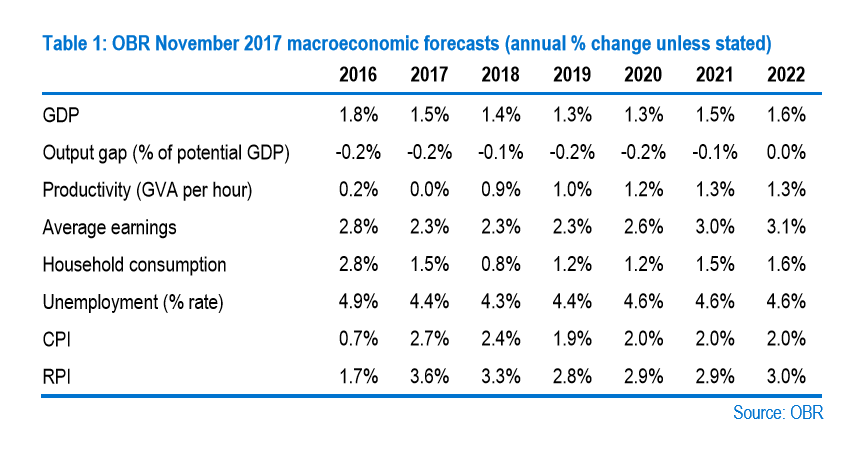

The OBR's most recent forecasts are contained in the table below.

For the sake of context, Investec's own house forecasts is for GDP growth of 1.7% in each year.

The other main event is the Bank of England's (BOE) Financial Policy Committee (FPC) meeting on Monday (statement published Friday 16) to discuss possible changes to capital buffers, introduced after the financial crisis under the Basel 3 regulatory framework.

The focus will be on whether the BOE reviews the size of the "Counter Cyclical Capital Buffer" (CCYB), a piece of regulation which guards against excessive bank-lending during upturns and excessive parsimony during downturns - thus the "counter-cyclical" sobriquet.

In November it was raised to 1%, with the FPC also indicating that it could be increased further in H1 2018 - so there is a possibility of a change at the meeting.

Again, this is unlikely to hit FX markets in any major way, and even if it does the impact may be difficult to gauge beforehand.

The CCYB impacts on the supply of credit, and therefore on inflation and growth, which in turn influence currency value, and it will probably form a part of the bigger picture that currency analysts consider in relation to their forecasts.

Generally increases in the supply of credit are seen as inflationary and likely to increase interest rates, which in turn leads to capital accumulation and a stronger currency.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

rrency