© kasto, Adobe Stock

The South African Rand looks poised to make more gains against the Pound in coming week as a compelling bearish pattern forms on the weekly chart.

The Pound-to-Rand exchange rate has been moving roughly sideways over recent weeks but we expect it to resume its bearish sell-off eventually and retouch the March 2017 lows at 15.50.

The pair was in a rising channel until it broke down in December and since then the outlook has turned significantly more bearish.

According to technical analysis, when prices break out of channels they are expected to fall as far as the height of the channel extrapolated lower (or higher as the case may be). This distance has not yet been achieved, however, so we see the potential for more downside until it is.

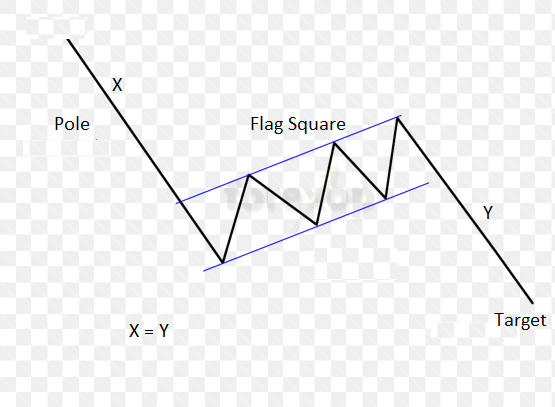

Further bearish indications come from the patterning of the move down since the November 2017 highs, which looks very much like a bearish flag.

Flags, as shown in the diagram below, are signs of continuation and we foresee this flag leading to a lower exchange rate eventually.

The usual method for forecasting how far a flag will unfold is to take the length of the move prior to the formation of the flag square, also known as the 'pole', and to extrapolate it lower.

However, in this case, the major March 2017 lows at 15.50 provide a more reliable, closer target, since major highs or lows act as significant support and resistance zones due to increased supply or demand.

The reason is psychological: traders who may have sold close to major lows, like the March 2017 low, but where then proven wrong when the market recovered, are normally so relieved at a second visitation and, therefore, the prospect of breaking even, (after having been in the red for so long) that they liquidate immediately rather than risk holding on in the hope of lower prices, and possibly being proven wrong a second time.

A further consideration is the bearish MACD which is fallking below the zero-line, signalling the pair is now in an established downtrend.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

Data and Events for the Rand

Politics and the US Dollar continue to be the two main factors influencing the direction of the Rand.

The currency gained at the end of last week after the opposition threatened to oust President Zuma on allegations of corruption.

A vote of no-confidence is scheduled to be held on February 22 to decide the matter, but if Zuma fails to win enough votes he will lose his job as head of state.

Analysts point out that Zuma has faced similar challenges in the past but has always somehow managed to survive, however, this time may be different as he has lost the support of several key allies within the government since Cyril Ramaphosa's victory at the

ANC leadership elections in January, and so he may be more vulnerable than usual to a challenge.

There are a growing number of politicians who now want to see Ramaphosa replace Zuma as soon as possible - and before his official tenure runs out in mid-2019.

Although the deciding vote is not until the 22nd news of maneuverings affecting Zuma's fate could impact on the Rand in the coming week with the usual negative correlation as previously.

The Rand is also inversely correlated to the US Dollar which rose strongly on Friday and appears to be benefiting from positive sentiment.

Expectations of higher interest rates in the US may impact on the Rand given the outsized proportion of debt either denominated in Dollars or originating from the US.

Clearly, a rise in interest rates or the value of the Dollar, therefore, is not in South African debtors best interests.

Data and Events to Watch for the Pound

Sterling's week got off to a soft start in the wake of the release of below-consensus data concerning the all-important services sector.

The IHS Markit service PMI number for January read at 53, down from 54.2 in December and below the 54.1 expected by economists.

The disappointing reading was primarily the result of a slowdown in the number of new work orders which, marking the slowest increase in services output for 16 months, completes a hat trick of disappointing surveys for the start of 2018.

This comes after both earlier surveys of the construction and manufacturing industries pointed toward slower activity for the month of January.

"This meant that the all-sector PMI dropped from 54.7 to 53.2 and on the basis of past form, points to quarterly GDP growth of about 0.3%, much lower than Q4’s 0.5% outturn," says Paul Hollingsworth, a senior UK economist at Capital Economics.

However, the main event in the week ahead for the Pound is the Bank of England (BOE) rate meeting on Thursday, Feb 8 at 12.00 GMT.

Analysts do not expect a change in interest rates so the focus instead will be on attempting to guess when the next change will come by analysing voting patterns, the wording of the statement and governor Carney's verbal responses to questions in the press conference after.

If the evidence points to a rate rise getting more likely then the Pound will rise; if not then it will fall.

Brexit risks continue to cause uncertainty about the outlook and weigh on the BOE's reaction function, and given those risks have not changed substantially, little change is expected, and possibly a muted response from Sterling.

The other main event is the release of the BOE's Quarterly Inflation Report at the same times as the meeting, and given inflation is one of the main factors which lead to higher interest rates, and interest rates are positively correlated to the Pound this too could impact on Sterling.

If economic growth and inflation forecasts are revised higher expect Sterling to catch a bid.

"We have long-argued that interest rates would rise somewhat faster, and sooner than markets expecting. Recent comments by Governor Carney offer tentative support to this view and suggest that February’s Inflation Report could strike a more hawkish tone than is anticipated," says Paul Hollingsworth economist at Capital Economics.

Inflation is currently 3.0% and has been caused mainly by the depreciation of Sterling since the EU vote in June 2016. The BoE has said it is willing to allow inflation to overshoot for a limited period before tackling it, however, Hollingsworth thinks they may start to show an impatience, given the stronger-than-expected performance of the economy. Such a change would be expected to lead to a modest rise in Sterling.

Other significant data in the coming week includes Halifax house price data for January out at 8.30 on Tuesday and industrial, manufacturing and trade data to round off the week.

Markets are expecting a reading of 54.3 from Monday's service sector PMI - anything better will likely set Sterling on a strong footing at the start of the new week, while disappointment could add to the bearish tone.

"While most of the early data was suggesting we could see the services sector run flat, the weak prints on both the manufacturing and construction PMIs last week now points to the Services PMI declining from 54.2 to 53.2, versus a consensus of 54.0, though we suspect that may likely drift lower by the time of release. The January PMIs so far suggest the adjustment in the housing sector persisted into January while more of the demand was coming from external sources rather than domestic, all suggesting no reason the Services PMI should outperform the softer January data," says a note on the matter from TD Securities.

The Halifax data may garner interest because last week's Nationwide data showed an unexpected surge in house prices in January, which lifted Sterling, and the market will be looking to the Halifax data to corroborate it.

Friday, meanwhile, sees the release of manufacturing and industrial production and the trade balance for December, all out at 9.30.

Markets are eyeing monthly industrial production to have slid 0.9% in December with the manufacturing production number showing an increase of 1.2%.

Trade data should show a balance of -£11.60BN as the UK continues to import more than it exports.

With regards to the above, the manufacturing data is expected to have the most impact on Sterling.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here