The Pound to South African Rand exchange rate remains subject to a short-term uptrend having bounced off a low near 16.077 back in June.

The pair has managed to rally above the 50 and 200 day moving averages and broke above a major multi-year trendline at the start of July – in very a bullish sign:

However, after rising only a relatively small distance after the break it subsequently pulled back down to the trendline again.

At the time of writing the exchange rate has fallen back to 16.85, having gone as high as 17.50 in the previous week.

This is quite a common phenomenon in financial markets.

Prices often pull-back after breaking above major trendlines in what are called ‘return moves’ or ‘throwbacks’.

These are normally followed by a resumption of the uptrend.

The probabilities, therefore, still favour a resumption higher, with confirmation of a bullish extension coming from a break above the 17.59 level.

For a general idea of how far such a move might go the usual method is to take the length of the rally prior to the trendline break (A) and extrapolate it the same distance higher (B).

This would lead roughly to establishing a target at 18.00.

Get up to 5% more foreign exchange by using a specialist provider. Get closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Data for the South African Rand

The main event in the week ahead is the rate meeting of the South African Reserve Bank (SARB) on Thursday.

Rand Merchant Bank’s John Cairns thinks there is a risk of SARB cutting interest rates, and that this is, “arguably one of the most difficult MPC decisions this year.”

The risk comes from political pressure to enlarge the SARB’s mandate to include growth and prosperity rather than just currency and inflation targeting, and this may put pressure on the governing council to cut rates.

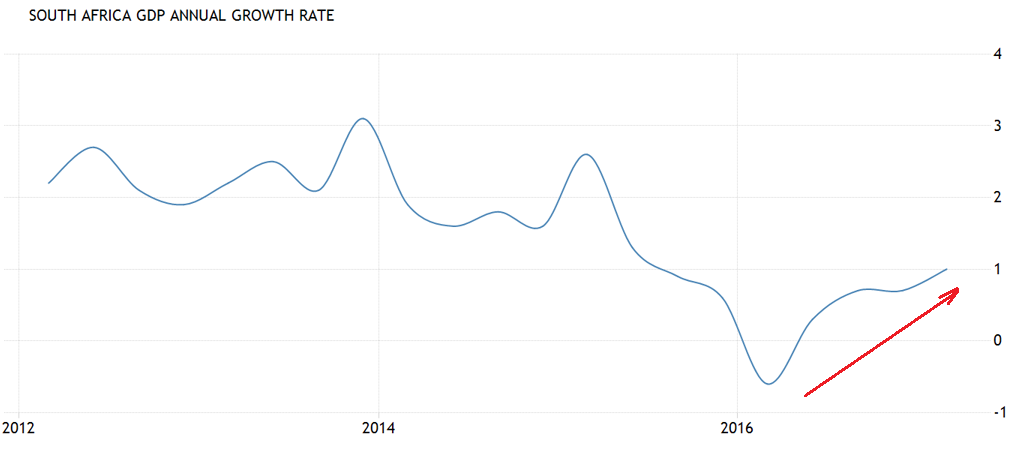

The raw data isn’t necessarily screaming out for a cut.

Although growth is not particularly strong at 1.0% it is trending higher after bottoming at 0.5% at the beginning of 2016.

Inflation is low by the standards of recent times at 5.4% but not according to longer-term history.

Left alone it seems unlikely the SARB would cut, but due to outside influences it may.

The other major release of the week is linked to the decision as it is inflation data out on Wednesday, June 19, at 9.00 BST, which is forecast to rise by 5.2% from 5.4% year-on-year in June (ie compared to June 2016).

Core Inflation, meanwhile, is expected to rise 4.7% from 4.8% previously.

Retail Sales is also released at the same time.

The Rand has received modest support due to the government’s mining charter being “mothballed pending a judicial review”.

The charter was designed to give black workers more of the share of the mining industry, which it was feared would scare away outside investors and thus weighed on the currency.

ZAR has negative feedback from the more positive outlook for developed economy interest rates, especially US rates.

This is due to much South African (SA) debt being dollar denominated or originating in the US and the negative impact on interest rate currency arbitrage or ‘carry’ as it is more commonly known.

Notwithstanding recent poor US data the outlook remains hawkish for US interest rates, which means they are expected to rise.

This will raise interest repayments for the many SA companies owing US debt and since higher US rates will also probably push up the value of the Dollar will increase the cost via currency cost.

Further it will reduce carry trade into ZAR from the US which previously supported the Rand due to the much higher interest rates enjoyed in SA compared to US, which led many investors to seek to park their money in SA.

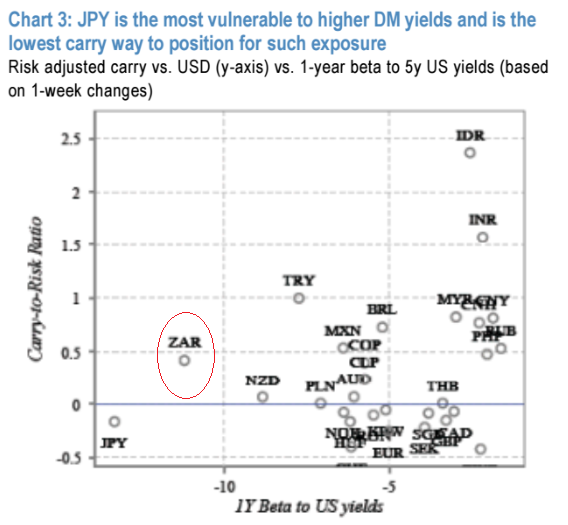

Research by investment bank Morgan Stanley has shown that the Rand is actually one of the most sensitive to rising US rates as measured by 5-year bond yields, which are a useful medium-term proxy.

“In EM, chart 3 also shows that ZAR is vulnerable to higher yields (it has the second highest beta to DM yields). This in combination with several idiosyncratic factors prompts a modest downgrade (USD/ZAR 2Q18 target is raised by 1.5%),” said Morgan Stanley.

We reproduce Chart 3 below; those currencies with coordinates closer to the bottom left hand corner show the closest correlation wit

US interest rates.

The top two are the Japanese Yen and the South African Rand.

Thus assuming higher US rates, the Rand is likely to weaken.

Data for the Pound

The standout release for Sterling in the week ahead is June Inflation data which is out at 9.30 BST on Tuesday July 18.

The release is important because it impacts on the decision making of the Bank of England (BOE), which in turn is a major driver of the Pound.

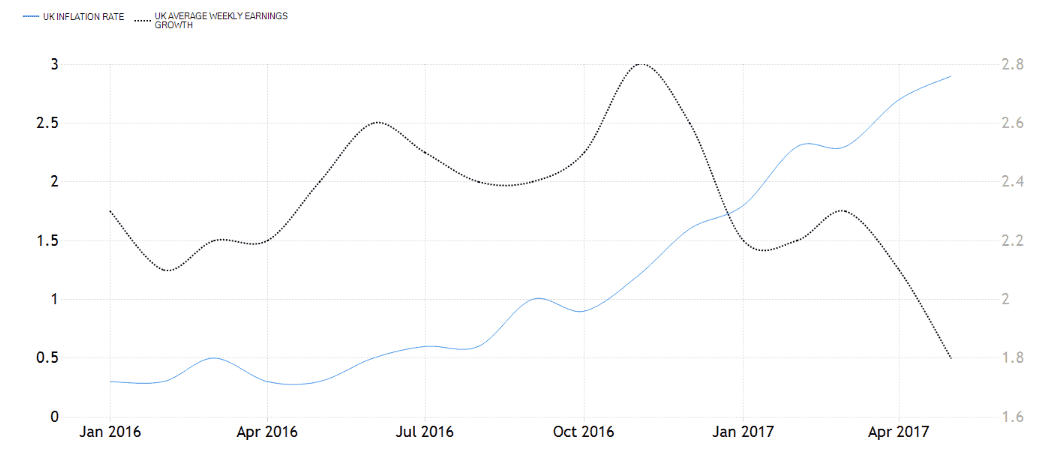

Inflation has risen steeply after the Pound weakened following the referendum, which had the consequence of pushing up the prices of imports.

Inflation in May stood at 2.9% year-on-year (yoy: ie compared to May 2016), and 0.3% month-on-month (mom).

The consensus amongst analysts is that it will remain at 2.9% in June yoy but rise at a lesser 0.2% mom.

However, Canadian Investment Bank TD Securities think the market is being too dovish and forecast a higher 3.0% rise in inflation.

TD expect Core inflation to come out at 2.6% which is the same as the market.

A rise in the cost of utilities is likely to be the driving force behind higher broad inflation and stable core.

“Inflation is likely to have continued its march upward in June, in part due to utility price increases. Core inflation, meanwhile, is likely to have remained stable.”

Nor do TD see this as the “peak for inflation” as core could rise 1 or 2 basis points and headline could rise to the “min-3% range”, which would, “head up the debate about a (single) rate hike later this year.

Incidentally the divergence between slowing average earnings in the UK and rising inflation is probably the root cause of the slowdown in the high street or “consumption” as economists like to call it.

The drag on growth from people spending less money is likely to keep the hawks at the BOE in check and limit any possibility of a rate hike.

We know Carney for one won’t change his view until the “trade-off” facing the MPC “continues to lessen” by which he means the trade-off between slowing growth and rising inflation.

Which brings us on to the other major release of the week for Sterling – Retail Sales on Thursday, July 20 at 9.30.

The market is currently being very optimistic about the gains expected in June.

They see headline Sales rising 2.6% yoy – which is a big jump from the previous 0.9% print; and Core increasing 2.4% from May’s very much lower 0.6% rise.

The market also expects a monthly rise of 0.4% for headline and 0.5% for core from -1.2% and -1.6% respectively in May.

This turnaround appears hugely optimistic from both our and TD Securities perspective, and seems to have little logic backing it up.

TD are of the opinion that Sales will not rise by anything (0.0%) mom in June rather than the 0.4% suggested by the market – we agree.

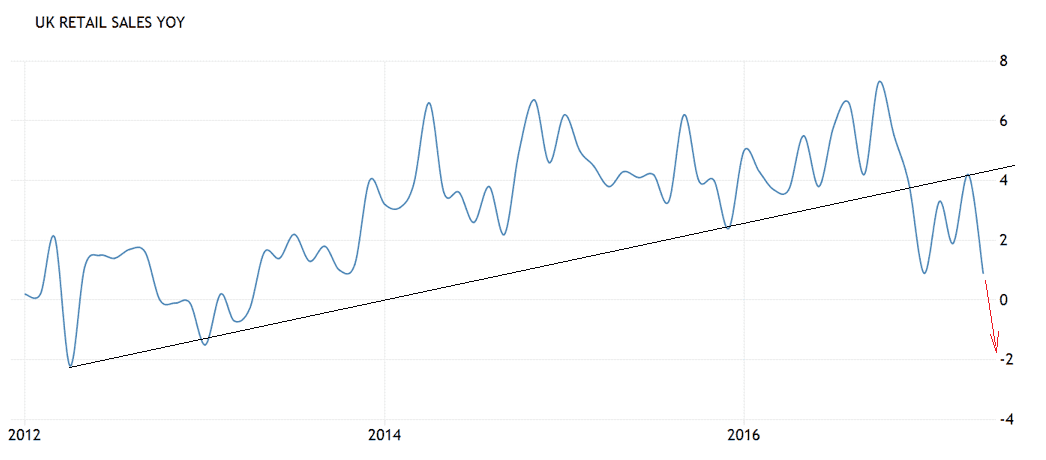

The picture below showing historical Retail Sales data shows a breakdown in the prior up-trend which gives the outlook a definite bearish hue.

The look and feel of the chart betokens a more negative print next Thursday than a more positive, which would also make more sense given the fall in real earnings.

BK Asset Management’s Kathy Lien, however, thinks there is a chance of a better-than-expected print:

“The smaller decline in shop pricesand the uptick in BRC retail sales monitor points to stronger numbers that should help rather than hurt the GBP/USD rally,”

Whilst this fits with the bullish technical outlook we, nevertheless, retain a negative bias.