The pound to rand exchange rate is tipped to decline over coming weeks as the SARB's fight against surging inflation could spell a stronger ZAR.

- The rand has softened as global commodity prices drift lower

- GBP to ZAR @ 21.7218, EUR to ZAR @ 17.2168, USD to ZAR @ 15.4233

- Inflation data could prompt more ZAR-supportive action at SARB going forward

Officials at the US Federal Reserve have been talking up the dollar this week, some market participants are speculating over whether the effort is coordinated.

Whatever the case, the tough talk has kept the slow and steady dollar rally intact, "commodities and currencies have weakened accordingly. The rand has merely been one of this pack, tracking the dollar step for step," says John Cairns at RMB.

While the ZAR is a slave to commodity price moves at present domestic events will certainly guide ZAR over coming weeks.

Markets were taken aback by data out on Wednesday showed South African inflation rising much more rapidly than expected.

Latest Pound / SA Rand Exchange Rates

| Live: 22.4285▲ + 0.14%12 Month Best:24.1619 |

*Your Bank's Retail Rate

| 21.6659 - 21.7556 |

**Independent Specialist | 22.1145 - 22.2042 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Prices in Pretoria rose 7.0% in February, easily beating the 6.8% analysts had forecast and 80 basis points above the 6.2% rise recorded in January.

The South African rand showed a muted reaction to the news, trading at about the same level at the time of writing as the day’s open price.

However, looking further ahead we believe the inflation data spells notable moves in the currency.

The South African Reserve Bank (SARB) has already raised rates in March in anticipation of rising inflation. The SARB put up interest rates by 0.25% to 7.0% at its March meeting last week with Governor Kganyago citing “mounting inflationary pressure” for the move.

Whenever a central bank raises its interest rates it is positive for the currency, as higher interest rates tend to attract more foreign capital.

The rapid rise in inflation will also have heightened speculation that the SARB will now have to raise interest rates yet further to try to quell inflation.

“It was a smart decision from the SARB as the CPI for February, released earlier this morning, came in well above median forecast, printing at 7% from 6.2% in January, while the market was expecting consumer prices to have risen 6.8%,” says Swissquote Bank’s Arnaud Masset.

“However, it was a close call as a few MPC members expressed concerns about the negative effects of high interest rate on the growth outlook,” says Arnaud.

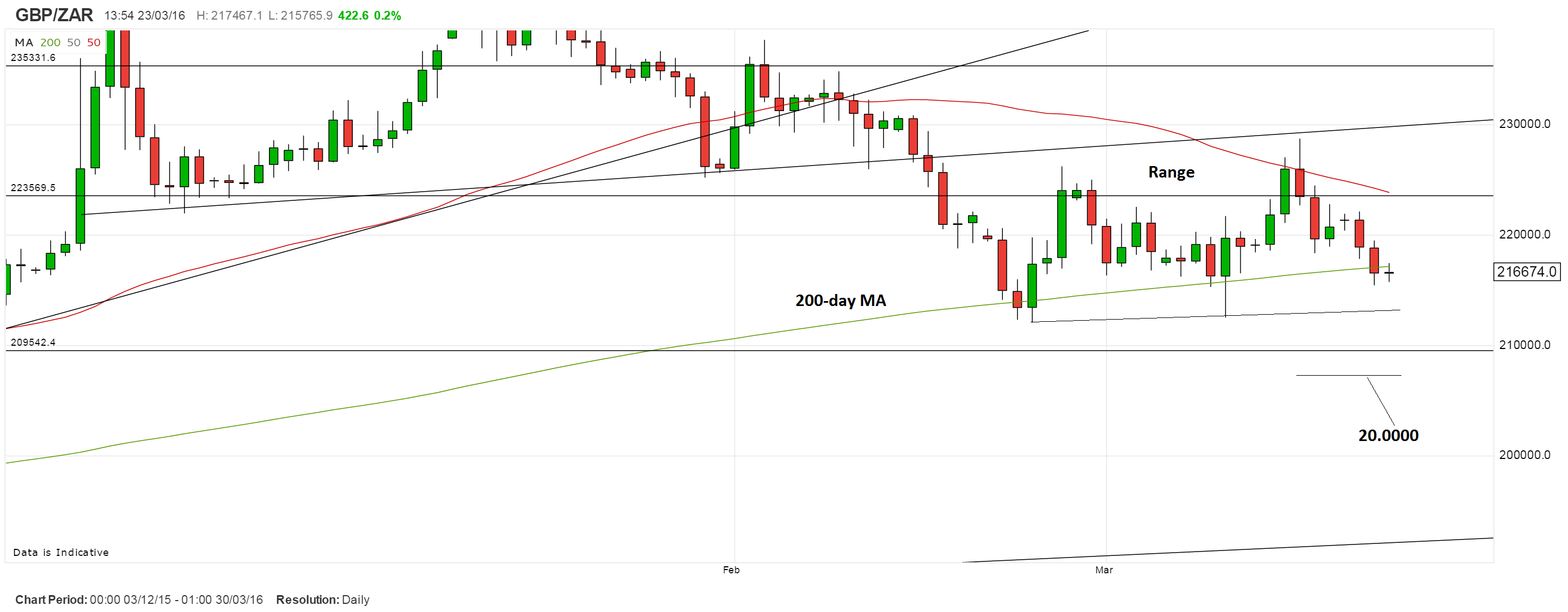

Rand Could Well Push GBP to 20.00

The rand’s rally through January and up until the 22nd of February came to an abrupt end at the 200-day Moving.

Since then it has been moving in a tight sideways range against the pound.

Despite the current sideways move, the structure of GBP/ZAR confirms a negative bias thanks to the sharpness of the sell-off seen at the start of 2016.

Our base case is therefore for a continuation down to 20.0000 as long as ZAR can strengthen sufficiently to break below the confirmation level at 20.7500.

With our view of ZAR-supportive interest rate rises on the horizon there is a good chance that the inflation-SARB dynamic could prompt the rand strength required to push GBP back to 20.00.

South African Bonds on Red Alert

A major concern for South Africa has been the threat of its credit rating being down-graded and its bonds losing investment grade to reach junk status.

We are told that if inflation is not contained the downgrade could occur faster than envisaged.

This would be negative for the rand as it would reduce the demand for SA bonds from foreign investors and so equally reduce demand for the rand.

The threat of a down-grade is never far away as the country remains on an economic knife-edge.

Economic growth is almost at a standstill, GDP grew only 0.6% in Q4 and other indicators suggest that the economy is on the verge of a recession

The Current Account is sporting a 5.1% deficit which is a further weigh on the rand, as it shows importers buy more foreign imports than exporters sell SA goods; the net effect is more rand being sold to buy foreign goods in their currencies.