Barclays exchange rate forecasts for the South African Rand (ZAR) suggest strength will ultimately return the currency to familiar territory.

The most recent currency forecasts from analysts at investment bank Barclays show the rand will likely recover ground against the pound sterling.

We have witnessed the pound to rand exchange rate break above the 20.00 level and head towards an all-time best at 21.52 on the 23rd of August.

The move higher fits within the context of the uptrend in place since April 2015.

The ZAR and its emerging market and commodity based counterparts are seen struggling; the ZAR in particular weakened by 1.11%/USD, 3.56%/EUR and 1.41%/GBP.

Latest Pound / SA Rand Exchange Rates

| Live: 21.9801▼ -0.19%12 Month Best:24.6167 |

*Your Bank's Retail Rate

| 21.2328 - 21.3207 |

**Independent Specialist | 21.6724 - 21.7603 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Broad-based USD strength owed to stronger-than-expected US data, falling commodity prices, as well as heightened risk aversion associated with Kazakhstan’s central bank widening the KZT’s trading band in relation to the USD (resulting in the KZT depreciating by 20%),” say Barclays in a note to clients.

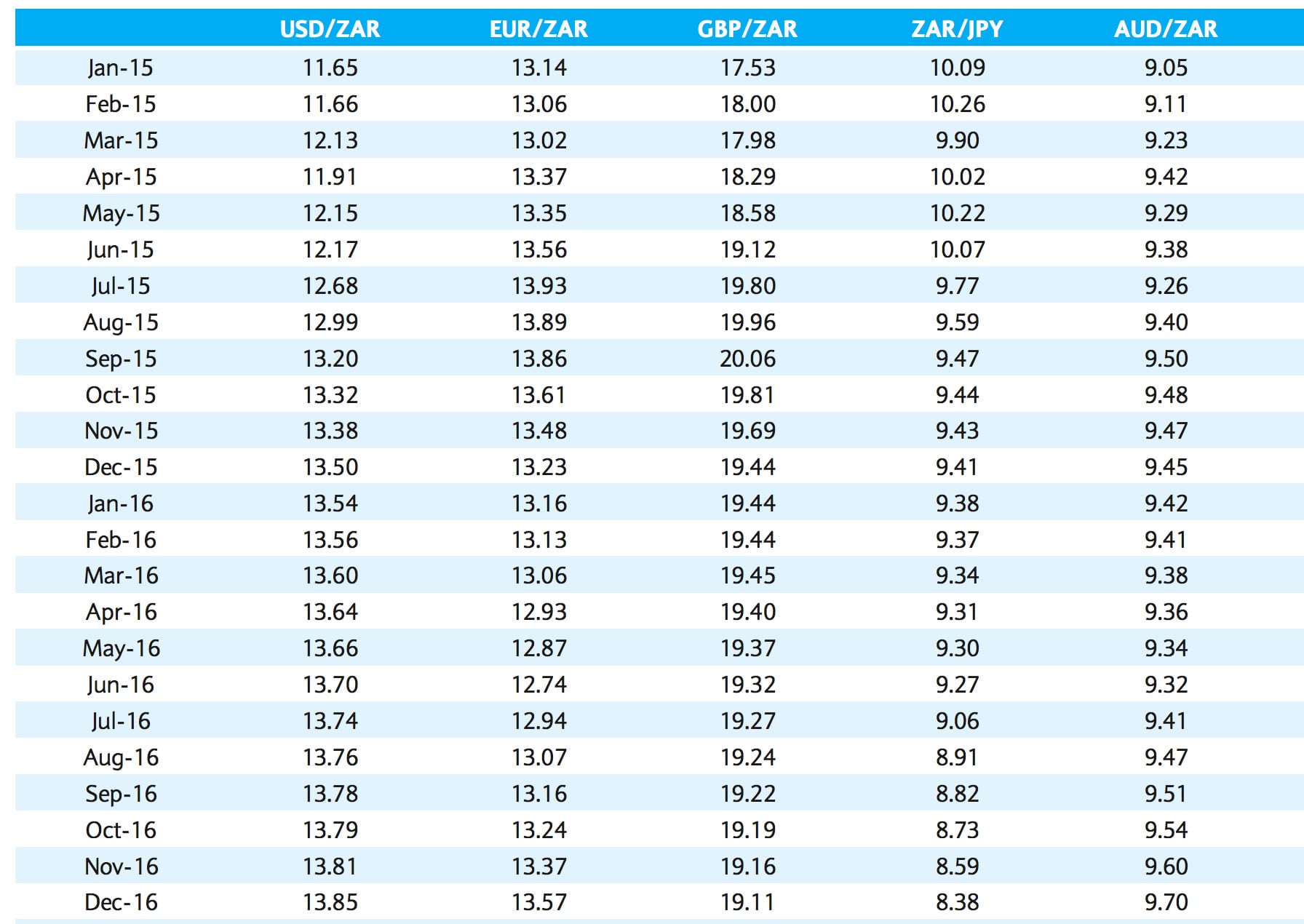

But by December analysts at Barclays are pricing in the exchange rate having fallen to 19.44 as rand strength reasserts.

Indeed, within the two year horizon that incorporates the close of 2015 we do not see the GBP/ZAR printing a figure above 20.00.

Key Points on the Research

The bank has revised their ZAR forecasts in line with changes made to their EURUSD forecasts in the wake of China’s decision to float the yuan and broad-based dollar strength.

“We now expect USDZAR to reach 13.50 by year-end and 13.85 by the end of 2016,” confirm Barclays.

Sentiment to South African government bonds (SAGB) is key - note that although local investors bought SAGBs last week, foreign investors were predominantly sellers of SAGBs. More specifically, foreign investors sold ZAR2.79bn worth of SA paper, obviously this plays on ZAR demand and its value.

The rise in USDZAR and the renewed weakness in oil prices create risks – working in opposite directions – for our existing CPI forecasts.

In terms of inflation:

“Roughly half of the petrol price, which is a significant 5.7% of the CPI basket, moves one-for-one with global gasoline prices (expressed in rand). Our CPI forecasts are based on the expectation of Barclays’ commodities analysts that Brent will recover to average $68/bbl in 2016. Recent market and price developments suggest there are downside risks to that view, and therefore downside risks to our CPI forecasts, which are currently under review.”

On Friday, the National Treasury will publish the July main budget data at 14:00.

Although the data from the first three months of the 2015/16 fiscal year indicate that the National Treasury remains on track to meet its budget deficit targets, Barclays think that a deteriorating growth environment is raising downside risks for revenue collections, and the July data should be a useful early indicator of the manifestation of this risk.

GBP/ZAR Threatens 20.00 Support

The key 20.00 level on the spot market appears to be coming into view as support for the pair.

The rand has strengthened for four days on the march and Thursday appears to be offering more of rthe same; indeed the rand is now at a better position than it was ahead of that massive slump on Monday.

Be aware that the RSI is reading at 51 suggesting we could be about to break into negative momentum territory in GBP/ZAR.

Support at the 20 day moving average (20.1754) is about to be tested; this could arrest the decline. A break would however certainly expose the 20.00 level in our view.

ABN Amro: Rand Weakness Ahead

In their latest foreign exchange forecast note ABN Amro - the Dutch investment bank - has warned they are pricing in a lower Ruble and SA rand from here.

Commenting on the outlook ABN Amro say:

“The Russian ruble and the South African rand also weakened sharply. South Africa’s economy contracted by an annualised 1.3% qoq in Q2.

“While growth is set to return in the second half of the year, it will remain weak on the back of commodity price weakness, high inflation preventing the central bank from loosening policy, and ongoing electrical power shutdowns due to maintenance work. It is likely that the rand will remain under pressure when the Fed starts hiking interest rates.”

Accounting for ZAR weakness USD/ZAR is forecast to rise to 13.50 by year-end ahead of a recovery to 13.25 in the first quarter of 2016.