- USD/ZAR back near July lows after SARB delays rate hikes

- Weakened after forecasts push cash rate lift-off back to Q4

- Virus, economic vulnerabilities, tamer inflation outlook cited

- Investec, Goldman Sachs see lift-off delayed beyond 2021

- USD still road blocked at 13.70/80, GBP struggles at 20.25

Above: File image of SARB Governor Lesetja Kganyago, Image © GovernmentZA

- GBP/ZAR reference rates at publication:

- Spot: 20.25

- Bank transfer rates (indicative guide): 19.54-19.68

- Transfer specialist rates (indicative): 20.07-20.11

- Get a specialist rate quote, here

- Set up an exchange rate alert, here

The Rand was steady but languishing near to three-month lows ahead of the weekend after the South African Reserve Bank (SARB) pushed back the likely timing of any post-crisis interest rate rise, leading economists at Investec and Goldman Sachs to suggest it could be 2022 at the earliest before borrowing costs go up.

Reserve Bank policymakers had inspired a short-lived bout of weakness in Rand exchange rates, lifting USD/ZAR and GBP/ZAR back near the three-month highs established earlier in July after taking a cautious view of the South African economic outlook, downgrading some of its inflation forecasts and revising back into the final quarter the projected timing of any initial interest rate rise from the Monetary Policy Committee.

The Rand had underperformed other emerging market currencies after the SARB's quarterly projection model advocated a 25 basis point increase in the cash rate from 3.5% to 3.75% for the final quarter of 2021, having dropped its earlier advice for a rate rise in each of the second and final quarters.

“The SARB’s interest rate forecasts from its quarterly projection model change frequently, and the SARB also ignores the projections depending on the conditions in the economy,” says Annabel Bishop, chief economist at Investec.

“The economy is unlikely to be particularly robust over 2022 or 2023, and such a 2.25% hike in the repo rate is currently unlikely. The SARB forecasts weak economic growth of 2.3% y/y in 2022 and 2.4% y/y in 2023. For 2021 it forecasts 4.2% y/y, although this is at risk,” Bishop adds.

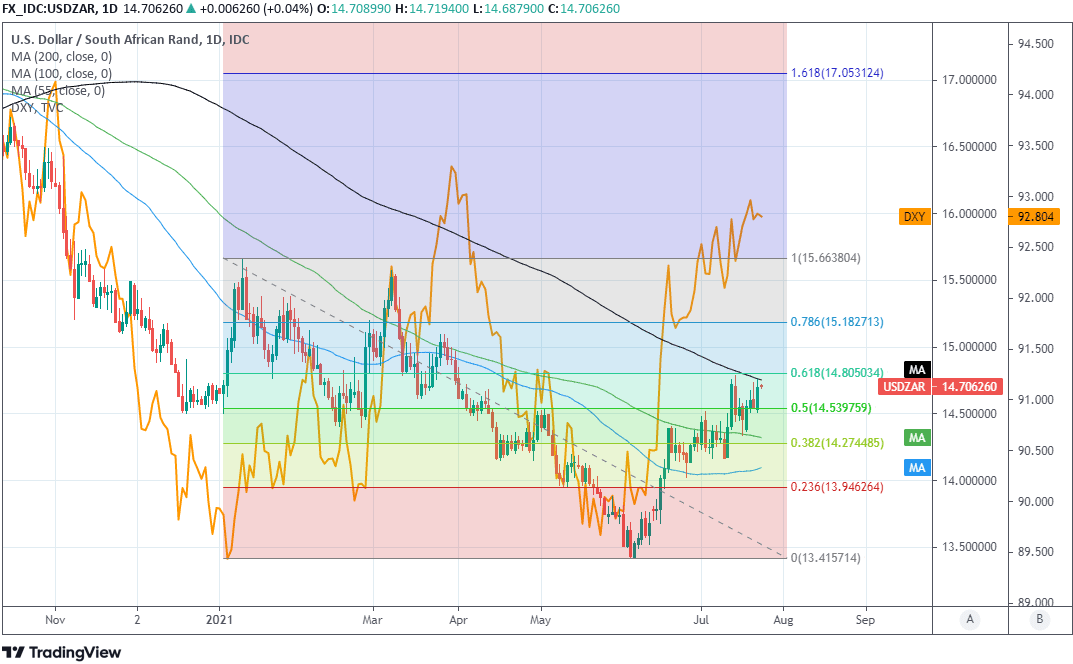

Above: USD/ZAR with Fibonacci retracements of 2021 fall, selected moving-averages (200:black) and U.S. Dollar Index (yellow).

The SARB also said its model is further advocating a 25 basis point increase in the cash rate for each of the eight quarters from January 2021, which would take its benchmark for borrowing costs back to 6% by the end of 2023.

But Investec’s Bishop and others are sceptical that such rate rises will be seen nearly as soon, however, given this month's tweaks to the SARB's forecasts for South African GDP growth and inflation.

“The forecast revisions were more dovish than we had anticipated. This – along with our more benign outlook for medium-term inflation than the SARB and consensus – supports our expectation that the SARB will refrain from tightening policy for the foreseeable future,” says Andrew Mattheny, a CEEMEA economist at Goldman Sachs.

The reserve bank noted that first-quarter GDP growth of 4.6% annualised had been “much stronger” than anticipated in its May policy decision, much of which was attributed to gains in commodity prices, but the bank still left its 2021 forecast unchanged at 4.2% as well as those for 2022 and 2023.

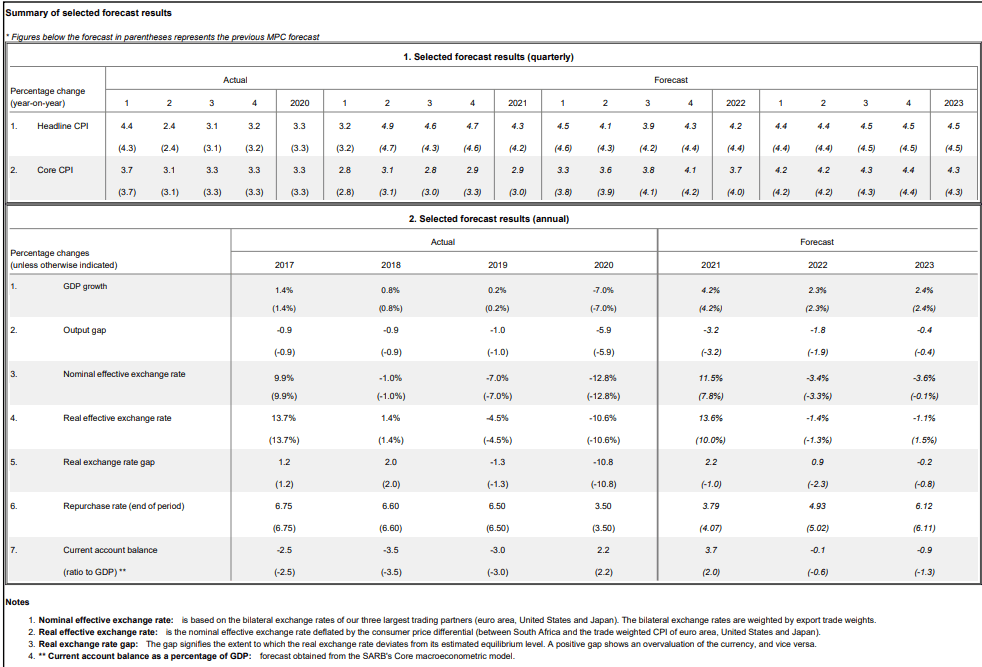

Above: July’s Monetary Policy Committee forecasts. Source: SARB.

Rising commodity prices have lifted and sustained national income at an elevated level in recent months but last week’s civil unrest and resulting damage to property and disruption of services was cited as having eliminated much of the benefit gained from the first quarter surprise.

“Given that the upside surprise to Q1 GDP implied on our estimates a mechanical upward revision to the full-year growth rate by around 0.5pp (all else equal), we take this to suggest that the SARB sees a growth impact of the recent unrest of around this magnitude,” says Goldman Sachs’ Mattheny.

The Rand softened against many currencies following the SARB’s decision, although the USD/ZAR exchange rate remained contained beneath the 14.70 area that has recently acted as resistance for the Dollar.

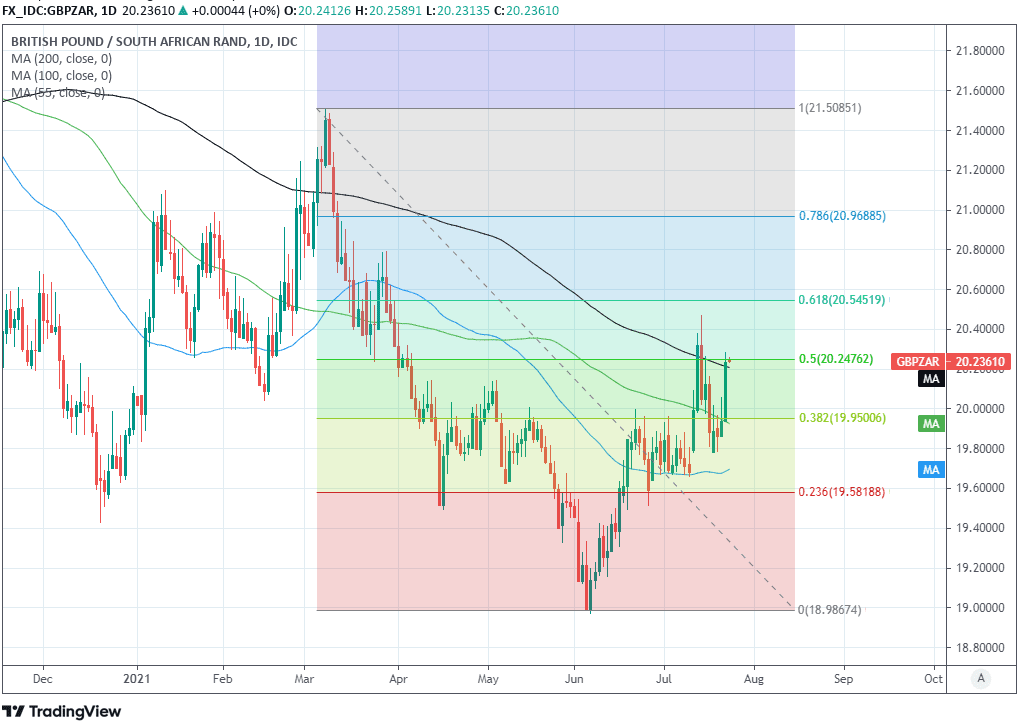

The Pound-to-Rand exchange rate rose above its 200-day moving-average at 20.20 meanwhile, where it remained early in the final session of the week.

The SARB cited new coronavirus variants and ongoing restrictions on activity in major economies as headwinds to the economy’s recovery, although what may have mattered as much for the Rand as the delay to its initial rate hike was the tame inflation outlook implied by the SABR's new forecasts, which were lowered almost across the board.

Above: Pound-to-Rand rate shown at daily intervals with Fibonacci retracements of 2021 fall, selected moving-averages (200:black).

“While economic activity strengthens over the forecast period, the current exchange rate level and modest growth in unit labour costs contain the expected rise in core inflation,” the SARB says in its statement.

The bank’s projection for the main inflation rate was revised a tad higher from 4.2% to 3.3% though next year’s forecast was cut while the outlook for the important core inflation rate - which overlooks the impact of changes in volatile energy prices - was downgraded for 2021 as well as 2022 and is not expected to return to the 4.5% midpoint of the SARB’s 3%-to-6% target band before late 2023.

This is potentially a big part of why the market appeared to lose enthusiasm for the Rand after the SARB’s decision because it’s inflation the bank is seeking to manage with its interest rate policy, and the tame outlook for price pressures creates scope for further delay and an even later lift-off for the cash rate than the SARB’s model advocated this month.

“The domestic inflation outlook is well anchored around the midpoint of the target, i.e. 4.50%, due to weak domestic demand, containment of unit labour costs, negative growth in private credit extension, a resilient rand, and expectations of a bumper maize harvest later this year,” says Kim Silberman, a bond and currency analyst at Rand Merchant Bank, who tips USD/ZAR to trade between 13.4 and 15.00 into the second half of 2021.

“We expect the SARB to begin hiking rates in mid-2022, in contrast to the FRA market which is pricing in a far more aggressive rate hiking cycle,” Silberman adds.