- ZAR closes in on chart support after USD’s advance

- Outlook hinged on Fed stance, market’s USD appetite

- But SARB’s inflation focus, rate pledge underpins ZAR

Image © Adobe Images

- GBP/ZAR reference rates at publication:

- Spot: 19.89

- Bank transfer rates (indicative guide): 19.20-19.34

- Transfer specialist rates (indicative): 19.71-19.75

- Get a specialist rate quote, here

- Set up an exchange rate alert, here

The Rand saw widespread losses on Tuesday which lifted USD/ZAR close to nearby resistance levels on the charts and left the outlook for the South African currency hinged on whether a supportive South African Reserve Bank (SARB) monetary policy stance can keep a resurgent Dollar at bay.

South Africa’s Rand has ceded further ground to all major developed and emerging market counterparts early in the new week and was building on losses Tuesday as the Dollar strengthened ahead of an appearance by Federal Reserve (Fed) Chairman Jerome Powell before Congress in Washington, where he’ll be questioned about the bank’s policy response to the coronavirus crisis.

This was despite another acceleration in the SARB composite business cycle indicator, which rose by 3.7% for the month of April after having increased by 2.3% in March.

“The largest contributors to the increase in the composite leading business cycle indicator in April 2021 were an acceleration in the 12-month rate of increase in the composite leading business cycle indicator for South Africa’s major trading-partner countries and an improvement in the RMB/BER Business Confidence Index,” the SARB’s announcement reads.

Tuesday’s 19:00 appearance by Powell could be an important determinant of appetite for the Dollar through the rest of the week at least as it’s the first scheduled opportunity the Fed Chair will have to remark upon the market response to last Wednesday’s monetary policy announcement, or to otherwise comment on the market’s apparent perception of its implications for the U.S. interest rate outlook.

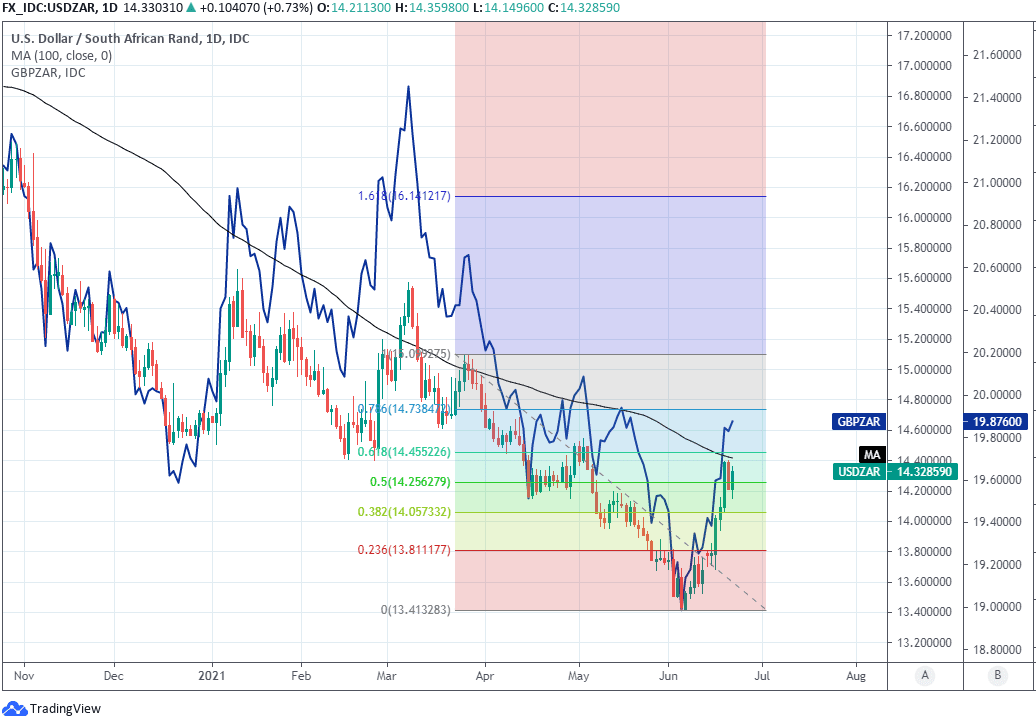

Above: USD/ZAR shown at daily intervals with Fibonacci retracements of second quarter decline, 100-day moving-average and GBP/ZAR.

“Offshore has been selling so consistently over the last two days we remain a touch cautious and investors are urged to bid accordingly,” says Deon Kohlmeyer, a trader at Rand Merchant Bank, referring to South African government bonds.

Last week’s update saw a majority of the Fed’s rate setters indicate they now individually expect to vote to lift U.S. rates before the end of 2023, with a substantial minority on the Federal Open Market Committee even seeing a potential case for a move as soon as next year, which appeared to send investors scrambling to exit earlier wagers against the greenback and culminated in steep gains last week for all U.S. exchange rates.

“USD/ZAR’s descent has taken it to the current June low at 13.4066 while medium-term from where it has swiftly reversed higher to the 2020-2021 downtrend line at 14.3668,” says Axel Rudolph, a senior technical analyst at Commerzbank.

“Together with the December-to-February lows and May high at 14.3952/5437 it offers strong resistance,” Rudolph adds.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

Much about the immediate outlook depends on if on Tuesday Fed Chairman Powell in any way vindicates the market for having apparently read last Wednesday’s update as meaning that upside risks to the Fed’s 2% average inflation target are becoming sufficient enough to mean the market was right to already be bringing forward the timing of the first likely interest rate rise it anticipates for the years ahead.

That could provide the Dollar with firmer ground on which to trade at least over the short-term and could mean in turn make it tougher for the Rand to extend its period of outperformance, which saw the South African currency rise against all major developed and emerging market rivals throughout the second quarter, effectively enabling it to erase much if-not all of the large losses wracked up against many during the crisis period last year.

A more sustained U.S. Dollar bounceback would be a headwind that could prevent the Rand from making further gains over at least the short-term, while South Africa’s third wave of coronavirus infections could become a domestic headwind if it leads to renewed closures of the economy.

“Those emerging market currencies that were seeing increased demand particularly in forward markets as a result of the higher rate of interest they offered are now offering a weaker reward when compared with the market’s expectations for the US Dollar,” says Charles Porter, CEO at SGM-FX Private.

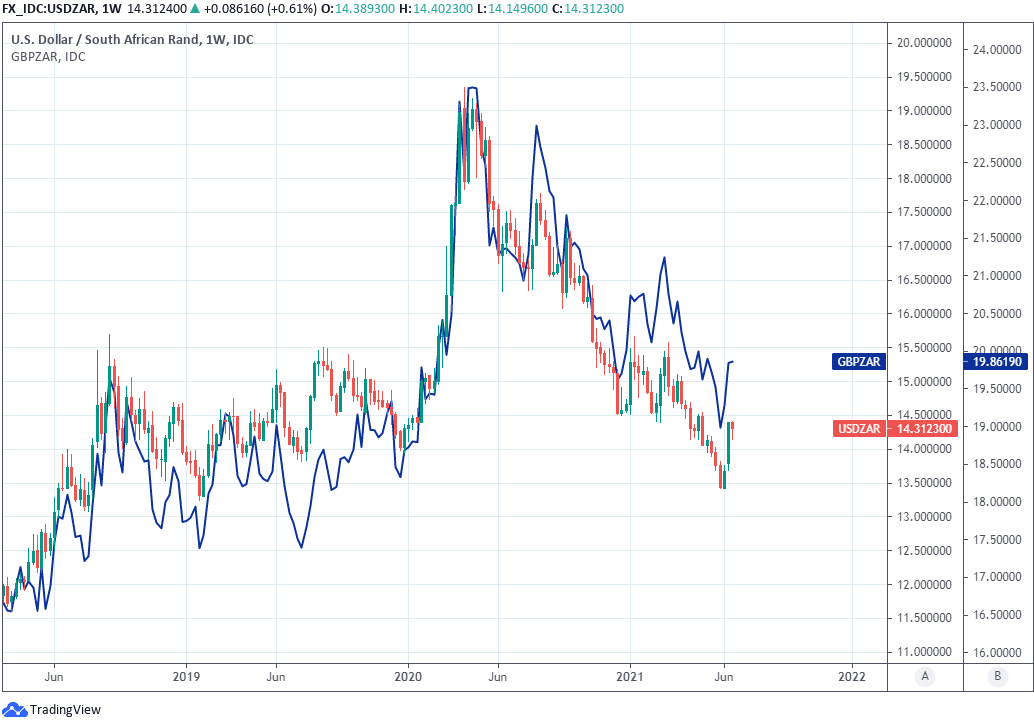

Above: USD/ZAR shown at weekly intervals with Pound-to-Rand rate.

However, there’s reasons for why South African exchange rates could still remain relatively well supported even if the Dollar recovers further elsewhere, and not least among them is the ever nimble monetary policy stance of theSARB.

“While we currently don’t expect any interest rate hikes in South Africa this year, 2022 could well see the SARB begin hiking, given its past hawkish bent, even before the US does, which is currently seen likely to be only in 2023,” says Annabel Bishop, chief economist at Investec.

“While the SARB is sounding a less dovish tone, and this is likely to help the rand retain some support, SA’s Reserve Bank is also likely to not hesitate to hike interest rates as global monetary policy becomes less accommodative, and rate hikes increase in other EMs,” Bishop adds.

SARB Governor Lesetja Kganyago was reported to have told a conference last week that weakness in South African exchange rates could lead the bank to begin giving serious consideration to an interest rate rise over the coming months, especially if that weakness leads inflation to threaten the upper 6% boundary of the bank’s inflation target, which is a prospect that could potentially ward off further weakness in the Rand.

South Africa’s cash rate was left unchanged at 3.5% last month following a unanimous decision by the monetary policy committee although the prospect of inflation rising further above the 4% midpoint of the SARB’s 3%-to-6% target this year or next was enough to keep the bank’s model advocating interest rate rises.

The SARB did acknowledge at the time however, that the Rand’s steamrolling 2021 rally has been helping to reign in those upside inflation risks in recent months by reducing the cost of imported goods.