- ZAR benefits at expense of RUB and TRY

- Falling USD boosts support for emerging markets

- CNH strength also aids ZAR

Image © Adobe Images

- GBP/ZAR spot rate at publication: 20.40

- Bank transfer rates (indicative guide): 19.68-19.80

- Transfer specialist rates (indicative): 19.60-20.00

- Get a specialist rate quote, here

- Set up an exchange rate alert, here

The South African Rand remains the hands down outperformer of the week and is likely on course for further gains over and above its recent 16-month highs over the coming periods, according to some traders and analysts.

South Africa’s Rand was lower against its nine largest developed as well as emerging world counterparts on Friday but in spite of this was still carrying healthy gains over all for the week following an uptick in demand that has dragged USD/ZAR beneath a layer of important technical support levels.

Rand bulls chased USD/ZAR all the way to 14.13 and its highest since January 2020 this last week before the still buoyant currency began to consolidate those gains on Friday, although another attempt at setting a further new high could now be just a matter of time, according to a trader at Credit Suisse.

“The Rand continues to post gains, benefiting from outflows from RUB and TRY. We have seen selling of TRY/ZAR after the CBRT. Our franchise flows were initially selling USD/ZAR following the break of 14.40 support (we saw decent volumes going through), however, they turned two-way close to the 14.20 level as some investors booked profits,” says Yuliya Kryzhanovska, a trader at Credit Suisse. “Expect the Rand to continue to post gains following the technical break of 14.40 support. Inflows into SAGBs are likely to support this momentum.”

Above: USD/ZAR falling below 200-week moving-average and major Fibonacci retracement level.

The Rand had been struggling with the above levels throughout April before a proverbial dam burst on Thursday.

South Africa’s Rand has pushed USD/ZAR below support, which denoted resistance for the Rand, just as the U.S. Dollar’s January 2021 ‘dead cat bounce’ looks to unravel concurrent with the recuperation of the Euro-Dollar rate, which accounts for 57% of the ICE Dollar Index.

“In the first two weeks of April, the USD Index lost half the gains it had achieved in the first quarter of this year. From a technical perspective, the 50-day moving average for the DXY or EURUSD has not crossed the 200-day moving average. This suggests that the general trend for a weaker USD has not been fundamentally challenged,” says Thomas Flury and Wayne Gorden, both strategists at UBS. “The consolidation in the first quarter opens the way to further USD weakness.”

The U.S. Dollar was easily the worst performing major currency of the week by Friday and is, according to strategists in the chief investment office at UBS Global Wealth Management, on course for even further declines over the coming months.

They’re watching the Euro, among other things, for cues on the Dollar’s next likely moves.

A declining U.S. Dollar is supportive of emerging market currencies and even more so when accompanied by things like the nascent but possibly only temporary decline in U.S. bond yields.

Above: U.S. Dollar Index testing 50-day moving average (black) after falling below 200-day average.

“The USD continued to dribble lower, as long-term US yields backed off again (BBDXY -0.15%, UST 10Y yield at 1.56%),” says Stephen Gallo, European head of FX strategy at BMO Capital Markets.

“Precious metals prices are starting to regain some of their footing, given the subdued tone in US longer-term yields, which naturally has implications for real rates. Spot gold has rallied 1.8% this week alongside an 8.8bps drop in the US 10-year Treasury yield. Platinum has lagged (+0.0%), but palladium and silver have climbed 4.1% and 3.4% respectively," he adds.

Dollar and yield declines are doubly supportive of emerging market currencies that also happen to underwrite commodity exporting currencies, like the Rand, while strong Chinese economic data like that released overnight is increasingly also supportive of the outlook for the global economy.

China, also South Africa’s largest trade partner and the source of its profitable trade surplus, saw GDP rise by an annualised 18.3% in the first quarter with economic activity in the period having turned out far ahead of that seen in the opening months of 2020 when the country was in the midst of its own first wave of coronavirus infections.

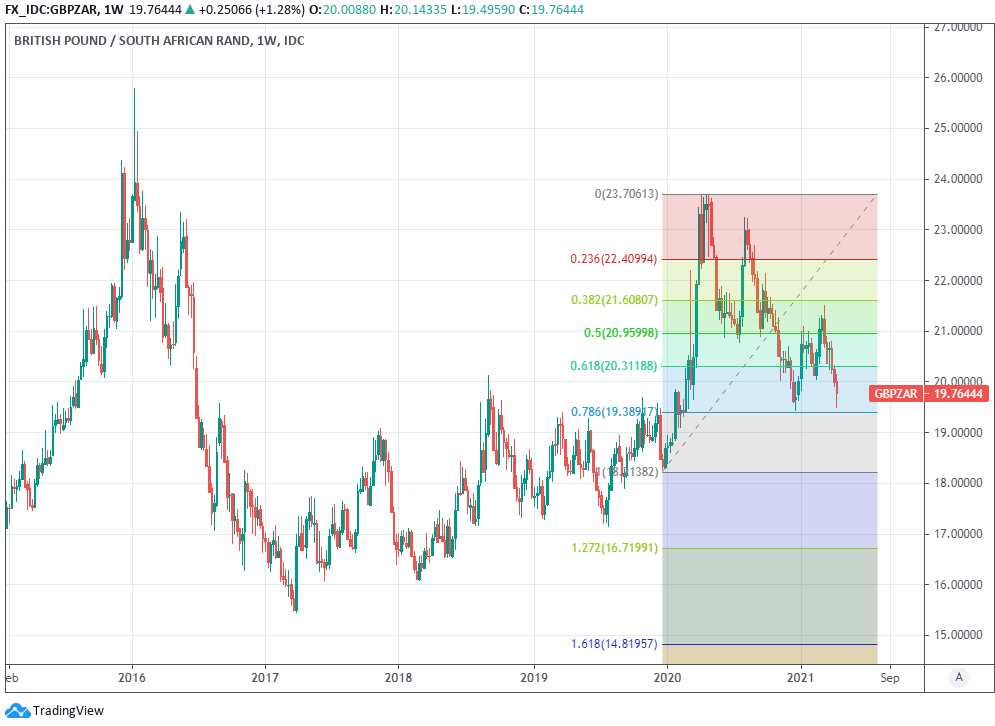

Above: GBP/ZAR at weekly intervals, testing major Fibonacci retracement level.

The Renminbi-Dollar rate was a fraction stronger while the trade-weighted Renminbi was a touch lower on Friday after a lengthy six-month period spent testing or otherwise setting new multi-year highs.

The Rand often benefits from strength in the Renminbi.

“Current rand trading falls squarely into the risk-on scenario posed by our FX analyst. A modicum of the brightness in the rand market extended to the rates space yesterday as SAGB bond yields closed tighter, reflecting a solid trading session with limited follow-through demand after the market repriced lower,” says Nema Ramhelawan-Bhana, head of research at Rand Merchant Bank.

“In crafting a narrative that includes SA, we cannot overlook the obvious health and socio-political occurrences. Our local media provides much of the detail,” she adds.

Rand strength may be positive for the South African Reserve Bank (SARB), which is to some extent banking on an appreciation of the domestic currency in order to keep upside risks to its inflation target in check.

The SARB assumed in its latest policy decision that the trade-weighted Rand would strengthen somewhat this year.

This would in the process cheapen the cost of imports into South Africa while potentially weighing on the consumer price index in what would be an economically supportive turn of events.

Governor Lesetja Kganyago also spoke following a SARB event on Wednesday of a need to keep inflation expectations contained.

This was possibly a tacit hint that it might not take much to get the bank thinking about raising interest rates while "foreign investors are well-rewarded” already.

The SARB’s quarterly projection model brought forward the timing of recommended interest rate rises in November and in March it continued to advocate a 25 basis point rise in each of the second and third quarters.