- ZAR reverses earlier losses on Mboweni's budget surprise.

- VAT hike avoided, easing concerns over Gov hit to growth.

- Tax reliefs provided through above-inflation bracket shifts.

- Spending cuts coming as public sector wage bill faces axe.

- But budget deficit, gross debt projections deteriorate again.

- Not clear if SA can still retain top rating for long after March.

Image © Government of South Africa. reproduced under CC licensing

- GBP/ZAR Spot Rate: 19.57, down -0.99% today

- Indicative bank rates for transfers: 18.89-19.03

- Indicative broker rates for transfers: 19.28-19.40 >> find out more about this rate.

South Africa's Rand swept higher on Wednesday after reversing earlier losses in response to Finance Minister Tito Mboweni's eagerly-awaited budget, which appears to have been warmly received investors who'd been hoping to see a spending plan that might avert a Moody's credit rating downgrade.

The Pound-to-Rand rate was down 0.99% following Finance Minister Mboweni's budget address to parliament, although some of that loss reflects weakness in Sterling, while the USD/ZAR rate slipped -0.49% making it one of only three Dollar exchange rates to decline during the Wednesday session.

Investors bid the Rand higher and sold government bonds which are the safe-haven 'risk-free' asset for investors in the domestic market even after Mboweni confirmed the unsustainable debt trajectory the was outlined in October's medium-term debt budget plan.

"The rand wasn’t the only financial instrument to show a source of strength, as South African banking stocks rose and yields on the benchmark 2026 bond fell to a five-year low," says Simon Harvey, an analyst at Monex Europe. "The mere acceptance by the Treasury that austerity wasn’t the way out of the negative debt trajectory was enough for markets to cheer along a rally."

Above: Pound-to-Rand rate shown at hourly intervals alongside USD/ZAR rate (red line).

South Africa's government announced 'net non-interest spending reductions of R156.1 bn for the next three years which includes "large reductions" to the public sector wage bill, in addition to above inflation increases to tax brackets. The latter are a relief to some investors given the government was expected to use below-inflation increases in tax brackets to protect tax revenues while there had also been expectations for another increase in the VAT tax rate again.

VAT hikes have been tried before and only served to damage the economy rather than return the public finances to a more sustainable trajectory. And given South Africa's economy is suspected of having slipped into a "three quarter recession" this year, large tax increases might only have exacerbated existing economic problems. Monex's Harvey says the budget is a step in the right direction but that if it doesn't bare fruit the markets will likely run out of patience.

"The 2020 Budget finally delivered the actual cuts to its expenditure projections (R156bn) that have long been deemed necessary, although the downwards adjustments are not as large as are needed, given also the downward revisions to revenue projections in earlier years, which helps debt projections remain unchanged at above 71% of GDP in 2022/23," says Annabel Bishop, chief economist at Investec.

Despite the market's favourable reaction to the budget South Africa remains on a spending and debt trajectory that has already been flagged as a major issue by Moody's, the last remaining agency to still rate the country an 'investment grade' borrower and the only thing standing between the country and a 'junk' credit rating. Moody's is set to announce its latest rating decision on March 27 and only time will tell whether it will move ahead with an immediate downgrade.

Above: Pound-to-Rand rate shown at hourly intervals alongside USD/ZAR rate (red line).

"South Africa’s fiscal situation remains dire, however, as the deficit widens to its highest level in 18 years," says Bianca Botes, a treasury partner at Peregrine Treasury Solutions. "While government is planning to slash the wage bill by R156bn over next three years, which will go a long way to ensure fiscal sustainability, the actual ability to effect this remains to be seen."

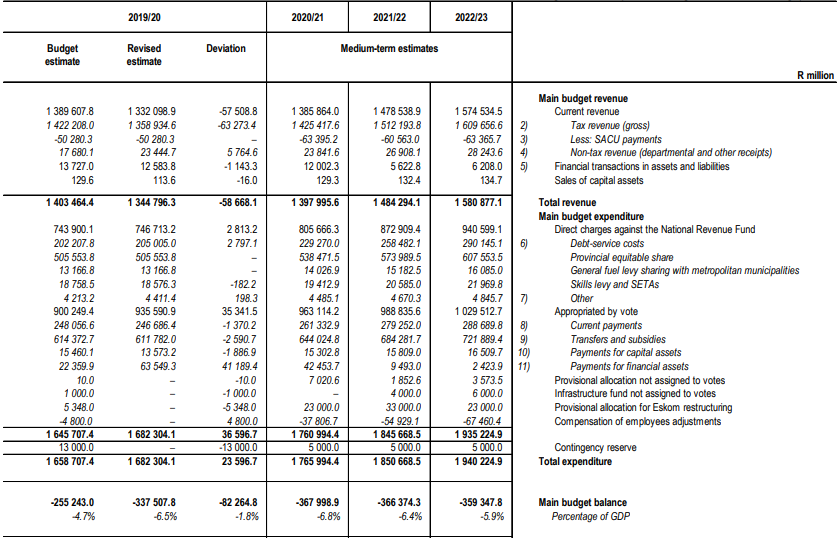

Some of the headline numbers referred to in parliament by Mboweni are different to those contained in the statistical annexe at the back of the budget document - due to "claissfication, definition and rounding" - and it's the latter that rating agencies will use to make their decisions. Those latter numbers show the budget deficit for 2019 coming in at -6.5% of GDP, which is even worse than the -6.2% number that horrified markets back in October, before topping out this year at the same -6.8% flagged in October.

However, the deficit projected for 2022/23 was 5.9% on Wednesday, which is an improvement on the -6.2% tipped back in October. But the government's debt trajectory has deteriorated in tandem with the improvement in the deficit, with 2019 gross debt now seen at 61.6% of GDP when it was expected to come in at 60.8% while the years out until the end of 2023 are all also subject to the deteriorated projections except for the final year.

The prospect of a downgrade to 'junk' has weighed on the Rand for years, keeping it close to record lows against the Dollar, and it could weigh further if it looks at any point as if Moody's will go ahead with one. It already downgraded the outlook on the rating from stable to negative in November, an indication that it could now make the call to downgrade at any subsequent decision.

Above: South African Treasury deficit trends and forecasts. Source: Budget 2020 statistical annexe.

"This last statement is likely to be highly problematic for government, and on its own will be enough to leave SA on a negative outlook from Moody’s. While Moody’s could downgrade SA on the strength of this Budget alone, it has recently said it is not in a rush to do so, and could well wait until November for a final rating decision, if not in 2021," Investec's Bishop says.

Moody’s matters to the Rand because a downgrade to junk would force the sale of government bonds by fund managers who are only able to hold 'investment grade' debt, leading to potentially large capital outflows. Managers of passive funds that mimic pre-determined benchmarks like the Citi World Government Bond Index, now called the FTSE World Government Bond Index, will have to sell their bonds if SA is excluded from those benchmarks by a downgrade.

Lucie Villa, the agency’s vice president and lead sovereign analyst, was reported to have told attendees that the once 'stable' outlook on the rating meant there was only a very low probability of a downgrade happening imminently. Villa said Moody's prefers to the downgrade countries' outlooks to negative before actually cutting the rating, and told eENCA South Africa is "likely" to keep the rating in 2019. However, that doesn't preclude a March 2020 downgrade or a cut to the rating thereafter.

"SA will likely remain on a negative outlook at Moody’s country review on 27th March. While there are some concerns SA will receive a credit watch, we believe this is very unlikely. A credit watch is used when a credit situation is very fluid and so changing, and the outcome is very uncertain, and SA is seeing slow change in the right direction," Bishop adds.

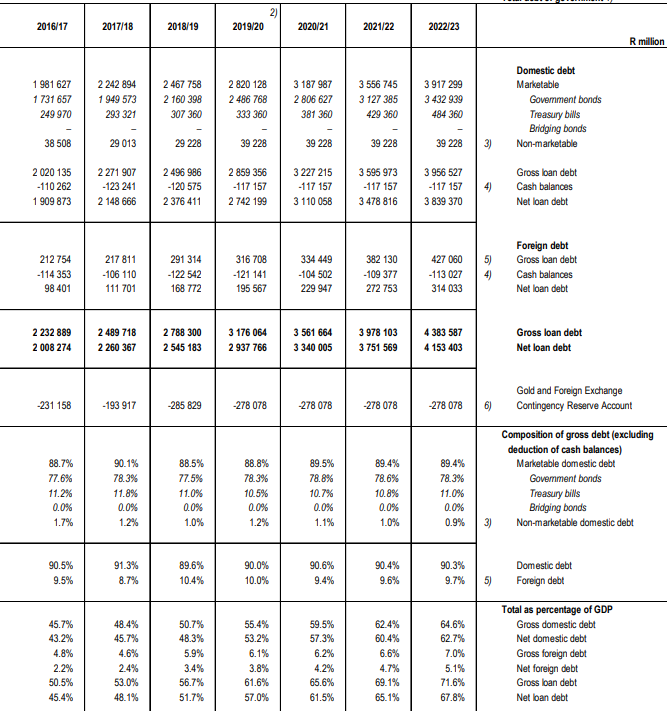

Above: South African Treasury balance sheet trends and forecasts. Source: Budget 2020 statistical annexe.