© Lefteris Papaulakis, Adobe Images

- GBP/ZAR finds support at beginning of new week.

- Market rested on major trendline near multi-year lows.

- GBP eyes Wesminster as ZAR looks for Eskom bailout.

The Pound-to-Rand rate was trading around 17.28 Tuesday following six weeks of losses, although studies of the charts suggest the pair has now found support and could be due a period of sideways consolidation over the coming days.

The 4-hour chart, which we use to determine the short-term outlook including the next 5 days, shows the market now trading just above a major trendline that is likely to provide support around the 17.15-to-17.20 level. This is a level the market has typically been repelled from.

In addition, the relative-strength-index (RSI) momentum indicator has been converging bullishly with price for the last week and taken together with the above, suggests at least a pause in the exchange rate's losses and probably a period of sideways consolidation.

Convergence occurs when the exchange rate makes a new low but the RSI does not follow. It is usually indicative of weakening downside momentum. However, there is also a risk the exchange rate could break below the support and continue falling, opening the door to a move below 17.10 and potentially as far down as 16.75.

Above: Pound-to-Rand rate shown at 4-hour intervals.

The daily chart, which we use to give us an indication of the outlook over the medium-term including the next month ahead, shows the main chart levels more clearly. Assuming a continuation of the still-intact downtrend and a break below 17.10, the pair will probably eventually continue down to a target at 16.50.

Alternatively, a rebound higher and break above the 17.65 level would confirm a continuation up to 18.10, which coincides with the 200 and 50-day moving averages (MA).

There is also a chance however, that the pair could simply move sideways over the longer-term given the oversold RSI, which is just exiting the oversold territory. This is a signal to buy. Such a sideways range would probably have a top at the 17.50 level and a bottom at the trendline around 17.20-30.

Above: Pound-to-Rand rate shown at daily intervals.

The weekly chart, which we use to give us an idea of the longer-term outlook including the next few months ahead, shows a rising trend channel in all its glory. The trendline is actually the lower borderline of this ascending channel.

A breakout of the channel and below the trendline would be a very bearish sign, likely indicating a decline to 15.30. The RSI momentum indicator in the lower pane is also relatively low, which is also bearish.

In addition, there's a possibility that the hard floor of support currently underpinning the pair holds. Such a thing could eventually give way to a rebound higher, enabling a rise all the way up to around 18.30 which is also the level of the 50 and 200-week moving-averages.

AA

AA

Above: Pound-to-Rand rate shown at weekly intervals.

AA

The South African (SA) Rand: What to Watch

The main event for the Rand this week is the announcement of the details of a strategic plan to provide long-term financial support for Eskom, the troubled electricity provider.

The financial needs of Eskom are considerable and have surpassed the provisions laid out in the budget so more help is required. This will be made clear when the Eskom Special Appropriations Bill is tabled in Parliament on Tuesday, July 23. Markets will be keen to see what the government’s longer-term strategic plan is since Eskom remains a major risk to the public purse and nation's top credit rating.

“We conservatively estimated that Eskom needs an additional ZAR28bn, on top of the ZAR23bn per year already provided for in the 2019 Budget," says Peter Worthington, an economist at ABSA Bank.

The other main event for the currency is be inflation data for the month of June, which is forecast to show a 0.3% rise on a monthly basis for both the headline and core consumer price indices when the figures are released at 09:00 London time on Wednesday. Headline and core CPI are seen at an annualised 4.4% and 4.1% respectively..

This is important for the Rand is because inflation dictates South African Reserve Bank (SARB) interest rate policy which has a direct influence over capital flows. When inflation falls below its target level central banks tend to cut interest rates, which makes the country less attractive to foreign investors as a place to park capital. This causes inflows to fall and weakens demand for the currency. The opposite is true when inflation rises.

“CPI inflation for June likely moderated to 4.4% y/y, from 4.5% y/y in May. The forecast risk here is exceptionally high though due to food inflation and, more importantly, the weighty quarterly rental inflation survey,” says Thanda Sithole, an economist at Standard Bank. “The South African Reserve Bank’s forecast of the output gap has widened, even after taking into consideration last week’s 25 bps cut, implying that domestic demand and thus demand-inflationary pressures are even more muted now. And, whatever the positive impact of this recent cut on growth will likely be negligible due to persistently depressed business and consumer confidence.”

The fluctuating Dollar is another driver of the Rand, which is negatively correlated to the U.S. currency, which means when the Dollar falls the Rand tends to rise and vice-versa. The main release for the Dollar this week is GDP data, which is forecast to have risen by an annualised 1.8% in the second quarter after a 3.1% increase previously.

The result is likely to influence the Federal Reserve (Fed) as they deliberate over whether the economy needs an ‘insurance’ interest rate cut to help support growth or not. A lower-than-expected result would ring alarm bells for the economy and confirm a Fed cut at one of the up-and-coming meetings.

Global risk trends can also often impact the Rand and on that note the main themes are the ongoing U.S.-China Trade talks and geopolitical tensions in the Gulf. On the U.S.-China trade deal, the situation seems to be improving after President Trump tweeted that Treasury Secretary Mnuchin had a “very good call” with his Chinese counterpart and the Global Times appearing to back this up saying that face-to-face talks are not far off.

Remarks on trade talks should be taken with a healthy dose of scepticism though because they seem to change with the wind and only last week Trump was saying ‘we are a long way from a deal’ and that Chinese links to Google needed to be investigated.

Meanwhile, Mnuchin was saying the opposite - that everything was fine and a deal is around the corner. It may sound cynical but it could be Trump’s positive tweet Monday was aimed at showing solidarity to his Treasury Secretary after contradicting him so starkly last week.

The other key driver of global risk trends to which the Rand is sensitive is the flare-up in the Gulf between Iran and the UK, which has the potential to escalate. In the most recent turn of events, a UK tanker was seized by Iranian revolutionary guard as it passed through the Strait of Hormuz.

The UK condemned the capture and a British frigate H.M.S Montrose approached and warned the Iranians to back-off, but it was too far away to intervene. Oil will probably be the asset most affected should tensions escalate.

If the oil price continues to rise it could spark concerns about rising fuel costs weighing on businesses and consumers, which might reduce growth and hurt the Rand.

AA

The Pound: What to Watch

The major driver of the Pound this week is likely to be the announcement of the winner of the Conservative Party leadership election on July 22, but with little difference remaining between the two candidates' stated Brexit policies, the result may not cause as much volatility as previously expected.

Jeremy Hunt is seen as more ‘moderate’ and less likely to take the UK out of the EU without a deal, so his election might provide some relief for Sterling. The opposite is true of Boris Johnson, who is the bookmakers' favourite to win, although such an outcome is likely in the price of the Pound by now.

According to betting website oddschecker, Johnson's chances of winning have increased to 97.08%. On the data front the major release is the CBI Industrial Trends survey, which on Tuesday and a speech from Bank of England’s (BOE) chief economist Andy Haldane on the same day.

Andy Haldane is set to make a speech at 13.15 on Tuesday. The market will be keen to hear his views on the economy after recent mixed data. Previously the BOE had been one of the few major central banks not expected to cut interest rates, and was actually talking about raising them. Much depends on Brexit of course. Will Haldane continue to endorse a marginally hawkish stance, or is he going to turn more neutral? On Tuesday we shall see. If he changes his tune it could weigh on Sterling.

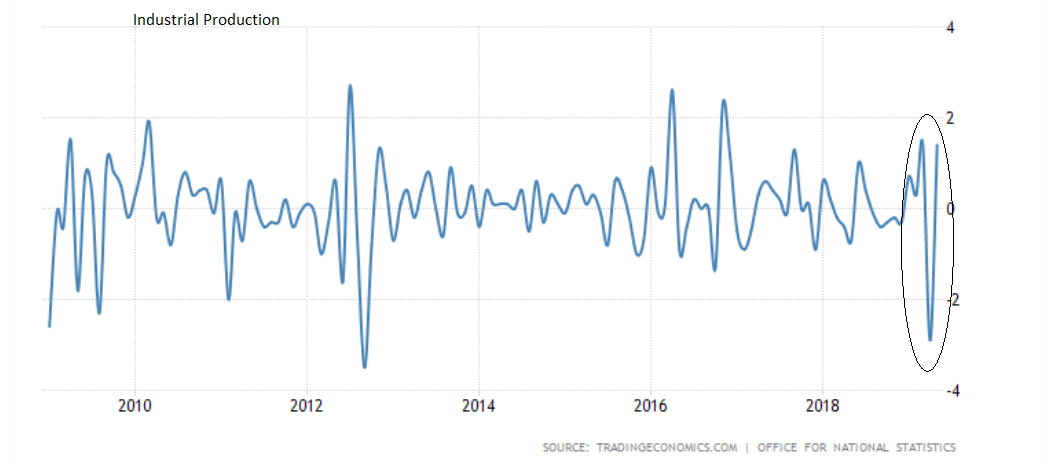

The CBI survey is usually closely followed because it provides timely insight into changing industrial trends. Industrial production unexpectedly plunged -2.7% in June and although it rebounded 1.4% in July it was a worrying result, and the worst since 2013. Investors will therefore be keen to see what the CBI data reveals when it is released on Tuesday at 11.00 BST and whether the sector is likely to see more declines in the future or not.

Above: Changes in UK industrial production. Source: Tradingeconomics.com.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement