Image © Leonid Andronov, Adobe Stock

- GBP/JPY spot rate at time of writing: 139.55

- Bank transfer rate (indicative guide): 134.66-135.64

- FX specialist providers (indicative guide): 137.45-138.57

- More information on FX specialist rates here

The Japanese Yen advanced against most major currencies on Friday as the Dollar rose amid faltering investor risk appetite, and after the Bank of Japan (BoJ) was sighted assembling a rifle and possibly preparing to enter into a currency war in which warning shots have effectively already been fired.

Japan's Yen was bought widely alongside fellow safe-haven currencies like the Swiss Franc and U.S. Dollar ahead of the weekend, although was lower relative to the greenback and its European counterpart.

Price action came as faltering investor risk appetite was reflected in falling stock markets and sovereign bond yields, with analysts citing and newswires reporting an array of prospective drivers behind the turn in exchange rates.

"USD/JPY punished the break sellers for the umpteenth time. We're more inclined to sell if the bounce extends close to 104.00 but it's not the easiest pair to monetize," says Jonathan Pierce, a trader at Credit Suisse.

Above: USD/JPY rate ahown at daily intervals alongside U.S. Dollar Index (black line, left axis).

It's in the markets of 2020 where, with investors intoxicated by simplistic risk-on-risk-off narrative - or merely stupified by an ongoing documentary of Washington's failure to agree even a greatly reduced and woefully inadequate 'stimulus package' - that financial vampires and werewolves may soon move out of the exchange rate shadows and into the light of day in order to do battle with each other in a war that would inevitably become unavoidably apparent.

Unfortunately, there's no easy on the eye, leather-clad men or women, ladies or gentlemen in this movie - just the sexless suits of the central bankers instead.

"The bank decision came after CPI for November showed at a weaker than expected -0.9% y/y. USD/JPY is firmer on-the-day, a combination of USD consolidation elsewhere and the BoJ commitment," says Patrick Bennett, a strategist at CIBC Capital Markets.

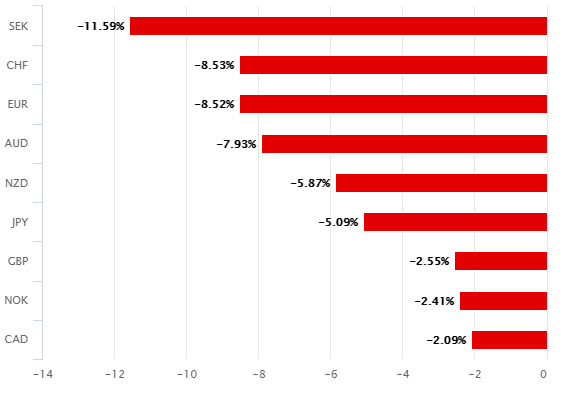

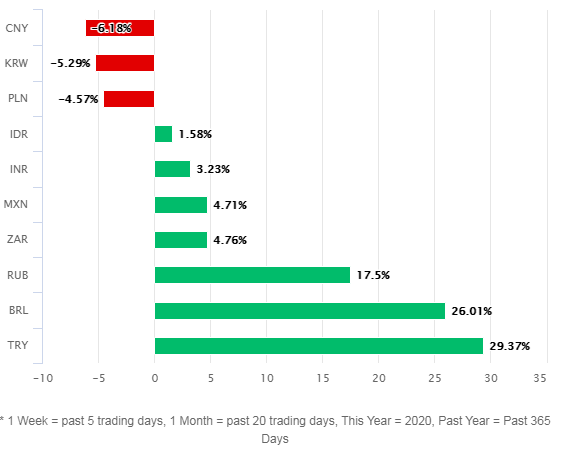

While not necessarily related, Friday's price action followed hard on the heels of the December monetary policy decision from the BoJ, and comes at the tail end of year in which the great, almighty and one true Dollar has fallen from grace with investors like an angel from heaven, having capitulated in earnest against all major currencies. America truly did come first in this year's currency market.

Above: U.S. Dollar's 2020 performance against G10 (left) and major emerging market currencies (right).

Dollar declines have been meaningful enough for it to have ceded ground to even a Pound Sterling that could now be just weeks away from a 'no deal' Brexit cliffedge, and are approaching the stage where they become problematic for a host of developed world central banks including the BoJ, Swiss National Bank, Bank of Canada and European Central Bank, Bank of England and Sveriges Riksbank to name just a few.

Ultimately and for mechanical reasons that often go underappreciated but which are partly explained in section B of the answer to question nine, it's possible if-not likely this conflict will leave no exchange rate or country untouched - irrespective of whether all of the respective central bank actively participate.

"In this situation, financing, mainly of firms, is likely to remain under stress for the time being," says the Bank of Japan in its December policy decision released on Friday. "Given that economic activity and prices are projected to remain under downward pressure for a prolonged period due to the impact of COVID-19, the Bank will conduct an assessment for further effective and sustainable monetary easing, with a view to supporting the economy and thereby achieving the price stability target of 2 percent."

The BoJ cited a coronavirus that was resurgent in both Japan as well as the wider world on Friday for its decision to begin preparing a new monetary policy tool, one which it pointedly stated will be entirely separate and distinct from the "QQE with Yield Curve Control" operation it has relied on to date. The bank judges the latter "has been working well to date," and so "there is no need to change it." Instead, the BoJ "will assess various measures conducted under this framework and make public its findings."

"We see this in part as a reflection of possibly building risks of JPY appreciation through the 100-level – something we now expect next year," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG, Japan's pre-eminent lender and the world's fifth largest bank.

The BoJ's review is tantamount to the assembly of a new rifle that it intends to use in a bid to ward off the deflationary pressures which again loom over Japan's economy. Much like elsewhere in the world, disinflation and the spectre of deflation have long kept the BoJ awake at night, although this plight of the world's policymakers has been exacerbated in 2020 by the U.S. Dollar decline that many analysts expect will continue through 2021.

Source: MUFG.

Japan's decision could be indicative of concerns about currency strength, which have already been voiced by the Bank of Canada most recently and the ECB before then, having turned into tensions among a normally close knit, cooperative and collegiate international community.

"Reports in the Nikkei daily [suggest] that PM Suga told the Finance Ministry in November not to allow USD/JPY to drop below 100.00," says Jane Foley, a senior FX strategits at Rabobank.

Inevitably, if ever used the BoJ's new rifle would first be pointed in the direction of the Fed, and this time there's no telling how the U.S. lender of last resort and shepherd of price stability will respond. Likewise with all of the others.

"The BoJ is set to try and counter this disinflationary FX move. The announcements this week certainly reinforce the prospects of loose monetary conditions and favourable risk asset performance, which led by the Fed will keep the US dollar on a weakening path," says MUFG's Halpenny.

Stronger currencies mean cheaper imports, weaker inflation and impaired competitiveness that threatens the growth outlook for export or trade oriented economies. This, in a market where developed economies and the largest banks on the bloc have wallowed for decades in falling rates of inflation and GDP growth, is hardly going to be welcomed by anybody.

One problem is that the further down this year's great, big Dollar decline takes the U.S. currency, the greater the risk becomes of other central banks or authorities entering the fray alongside the BoJ and possibly the Federal Reserve. Already, and this week alone, the U.S. Treasury Department designated Switzerland as a 'currency manipulator' for reasons that relate to all of the above while the Bank of Canada warned of risks to its inflation target as well as exporters and economy - which rise as the U.S. Dollar falls.

"For the first time in a decade the National Bank of Poland intervened to prevent the zloty from appreciating against the euro on Friday. On numerous previous occasions the MPC has indicated its preference for a weaker zloty to support recovery from a recession caused by the coronavirus pandemic. In our view this was a proper warning shot that the NBP is ready to act and intervene directly if the zloty appreciates too fast," Rabobank's Foley says.

Above: USD/JPY rate ahown at monthly intervals alongside U.S. Dollar Index (black line, left axis).