- GBP/USD towards bottom of 2021 range

- Commerzbank sees support likely holding

- But warns of "BIG" breakdown point

Image © Adobe Images

- GBP/USD reference rates at publication:

- Spot: 1.3683

- Bank transfers (indicative guide): 1.3304-1.3400

- Money transfer specialist rates (indicative): 1.3560-1.3615

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

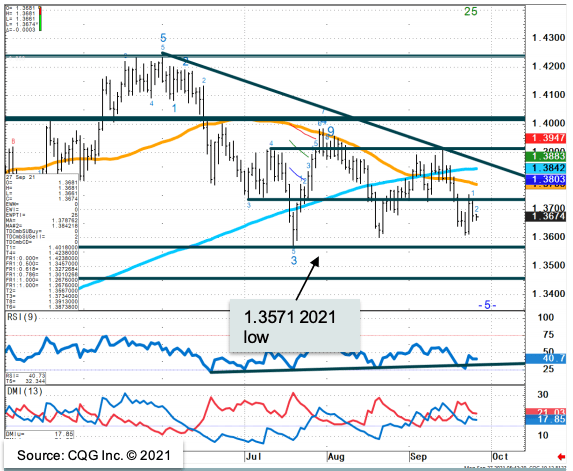

The Pound-to-Dollar exchange rate starts the new week at 1.3670 which places it towards the bottom of a range that has held since February, but one technical analyst says notable support located nearby will remain hard to crack.

Analysis from Commerzbank shows 1.3557/78 to be a near-term line in the sand for the Pound-Dollar exchange rate, confirmed by a bounce from this region towards the end of the previous week.

"GBP/USD recovered last week from the 1.3557/78 July low, February low and long term Fibo, which suggests a reluctance to break down at this stage," says Karen Jones, Head of FX and FI Technical Research at Commerzbank.

Image courtesy of Commerzbank.

Jones says any rallies by Pound-Dollar will find initial resistance at 1.3726/34 which is the September 08 low.

"Stronger resistance is found at one month highs at 1.3893/1.3914. We have no strong bias," says Jones.

But beware, although coming days might not offer up significant moves in Pound-Dollar, Jones warns the 1.3571/57 low is key, "and a break below here would represent a BIG break down point".

Failure of this level would potentially see a fall to the 1.3504 January 2009 low and introduce scope to the 200-week moving average at 1.3161 she says.

The British Pound picked up some buying interest at the aforementioned 1.3557/78 low last week thanks to the Bank of England which effectively endorsed market expectations for an interest rate rise to take place in the early part of 2022.

Market expectations have built during the course of recent months that rising UK inflation levels and a stronger-than-expected labour market would induce the Bank of England into a rate rise in 2022.

But market expectations have firmed further for an early 2022 hike after the Bank said last Thursday that "some modest tightening of monetary policy over the forecast period was likely to be necessary to be consistent with meeting the inflation target sustainably in the medium term."

"Some developments during the intervening period appear to have strengthened that case," the Bank said in a Statement.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

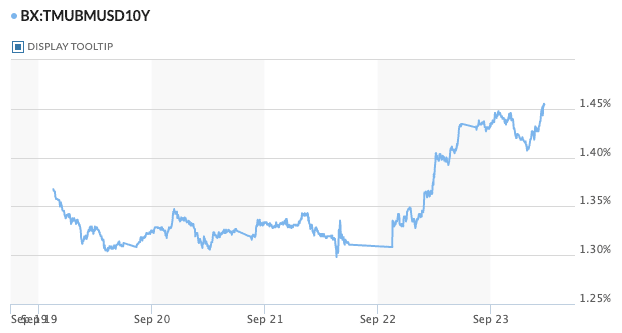

The Pound rose on the day as UK bond yields rose to reflect expectations for interest rate rises, but the rub for Pound Sterling bulls is that yields also rose in Germany and the U.S. at the end of the previous week as investors saw higher central bank interest rates elsewhere too.

The Federal Reserve said on Wednesday it would conduct a relatively sharp tapering of its own quantitative easing programme, hoping to be done by mid-2022.

The prospect of an interest rate rise in 2022 is still relatively low but certainly by 2023 the market is expecting up to three rate rises.

"The September FOMC meeting was hawkish. We expected a November taper start but the mid-’22 completion suggests a faster purchase reduction (vs our prior base case of September taper end). This clears the runway for hikes as early as 2H ’22," says Mark Cabana, an analyst with Bank of America.

This relatively hawkish takeaway from the Fed inevitably diminished any boost to UK yields and Pound exchange rates offered up by the Bank of England.

"We recently revised up our Sterling forecasts after our economists brought forward their projection for rate hikes following firmer inflation prints and strong labor demand, as well as some more hawkish BoE rhetoric about how to respond to those economic developments," says Michael Cahill, an analyst with Goldman Sachs.

The Bank of England went so far as to say that raising interest rates in 2021 was still not out of the question as they felt ending quantitative easing was not a requisite before interest rates can start.

The quantitative easing programme is expected to end in December.

"The BoE meeting ... confirmed that change in outlook, and if anything the risks to the first hike now appear to be skewed even earlier, with the MPC explicitly 'ruling in' rate hikes this year, even if that seems fairly unlikely," says Cahill.

"Sterling should perform well against this backdrop," he adds.

Cahill does caution on expecting significant upside, however, citing "reasons to limit the enthusiasm on the currency’s upside."

"The BoE’s plan to more actively use its balance sheet in the normalization process will likely weaken the link between the policy outlook and currency performance somewhat," he says.

The balance sheet utilisation referred to above is the plan set out by the Bank of England in August to actively reduce the stock of bonds it has brought up during its quantitative easing era once the economy had recovered.

This limits the need to raise interest rates, thereby denting some support the Pound might have expected from this avenue.

The broader market backdrop will also matter for the Pound.

"Sterling remains a fairly cyclical currency, so we would be cautious on fresh long positioning while China worries are driving risk sentiment," says Cahill.

The Pound tends to underperform when global stock markets are struggling, as was the case last Friday when a sell-off in global stock markets linked to a surge in global financing conditions was seen to be dictating currency moves.

Most major indices were in the red and 'risk off' or 'safe haven' currencies were benefiting as a result.

As mentioned earlier in this piece, UK, US and German yields all rose as markets priced in higher central bank interest rates in coming months.

Above: The yield on US ten year sovereign bonds. Image: MarketWatch.

This raises the cost of financing, with investors anticipating it to act as a headwind to growth and stocks suffered accordingly.

For foreign exchange markets currencies such as the Yen, Dollar, Franc and to a lesser extent the Euro, would tend to benefit against the Pound.

"We still favour USD strength in the months to come," says Kristoffer Kjær Lomholt, Chief Analyst at Danske Bank.

Danske Bank say not only has the Federal Reserve turned more 'hawkish' - thereby supporting the Dollar - but the global market backdrop is not as constructive as it once was.

This view therefore gives opportunity for 'safe haven' currencies such as the Dollar to perform well over coming weeks.

"We expect further move towards a tightening of global liquidity conditions, lower PMIs, peak inflation concerns and a further recovery in US jobs," says Lomholt.