- GBP/USD steadies after being hit by coronavirus concerns.

- But GBP remains in a month-long technical consolidation.

- Chart continuation pattern implies break to upside pending.

- But BofA Global Research says GBP unfit for another rally.

- GBP is no longer undervalued in the way markets perceive.

- And faces only a steady grind higher Vs a weakening USD.

Image © Emil Sykko, Flickr. Reproduced under CC licensing.

- GBP/USD Spot rate: 1.3126, up 0.06% today

- Indicative bank rates for transfers: 1.2767-1.2858

- Transfer specialist indicative rates: 1.2929-1.3008 >> Get your quote now

Pound Sterling continued a technical consolidation against the Dollar Friday, from which it could eventually break either to the up or downside although whatever happens, some say it lacks the horsepower for another big rally.

Sterling was quoted lower against the Dollar Friday after being buffeted by fresh concerns about the spread of China's new coronavirus, which lifted safe-haven currencies while weighing on their riskier counterparts, although the Pound has remained within its narrowing consolidatory range against the greenback.

The Pound has carved out a 'symmetrical triangle continuation pattern' since mid-December, which is now clearly visible on the 4-hour and daily charts.

Above: Pound-Dollar rate carves out symmetric triangle after topping out at 1.35 in December.

"Continuation patterns usually indicate that consolidative price activity will resolve in the same direction as the trend that was in effect before the pattern formed," says George Davis CMT, chief technical analyst at RBC Capital Markets and two-time winner of Technical Analyst of the Year. "The symmetrical triangle is a continuation pattern that is formed by an ascending lower trendline and a descending upper trendline that converge."

Sterling's symmetric triangle began to form just weeks after it appeared to have converted a long-established downtrend into a new uptrend, which should mean the eventual breakout from the consolidatory range will be to upside.

The British currency had spent the period between April 2018 and October 2019 mired in a downtrend but overcame a key downward sloping trendline in mid-October when Prime Minister Boris Johnson declared victory in his attempt to renegotiate aspects of Theresa May's EU withdrawal agreement.

Overcoming the downtrend led Sterling straight into an earlier symmetric triangle continuation pattern that resolved to the upside when it emerged Boris Johnson was on course for a landslide election win back in December.

Above: Sterling overcomes April-2018 downtrend in October 2019, leading to triangular consolidation through November.

"While this pattern can be bullish in an uptrend or bearish in a downtrend, a price breakout must occur before the three-quarter point of the triangle apex in order for this pattern to remain valid," Davis says in an explainer to RBC clients.

Established theory on technical analysis dictates that this latest pattern in the Pound-to-Dollar rate should also resolve to the upside, which is a view that's been somewhat seconded by technical analysis from BofA Global Research.

"Another close below 1.30-1.2961 confirms a technical top and signals a decline to 1.2685. Otherwise spot is attempting to form a bigger picture double bottom. The 4Q19 rally looks like a successful repeat of the April-Sept 2017 rally, so far, with more to achieve," says Paul Ciana CMT, chief technical analyst at BofA.

The 1.30-1.2961 level flagged by Ciana as a trigger for more downside coincides closely with the bottom of the Pound-to-Dollar rate's symmetric triangle, although Ciana favours a resolution to the upside for Sterling.

Above: Pound-to-Dollar rate shown at weekly intervals.

The prospect of further upside is seconded by BofA Global Research fundamental analysts, who're more concerned with estimates of 'intrinsic value' than they are studies of trends and momentum on charts. But they also say Sterling lacks the horsepower for another big rally because it's no longer as undervalued as many think and will be weighed down in the months ahead by a slowing economy and interest rate cuts from the Bank of England (BoE).

"The narrative has been that the removal of Brexit risk will allow GBP to gravitate back towards some notion of fair value and therefore significant appreciation. We challenge this view," says Kamal Sharma, a fundamentals oriented strategist at BofA Global Research. "Whilst we concede that there is scope for a GBP recovery on our base case scenario we find it hard to make the case for a sustained break above $1.40 in the coming years."

Sterling was hurt badly by the vote for Brexit in June 2016 and since then some commentators have suggested that if future relationship negotiations are able to negate the worst of the risks around an EU exit - the threat of a return to tariffs - the Pound should reverse its post-referendum decline and then some. That implies substantial upside for an exchange rate that routinely traded above 1.50 before the referendum but was quoted at only 1.31 Friday.

One city firm is still forecasting a Pound-Dollar rate of 1.50 by year-end based on the expectation of a smooth Brexit and it's not the first to have done so, but the mechanical parts that drive perceptions of exchange rate value have moved meaningfully since the referendum. In other words, the rest of the world has moved on since the Brexit vote and crucially, some important central banks.

Above: BofA Global Research graph highlights symmetric triangle and overcoming of post-April 2018 trend.

"Whilst the pricing out of political risk premium has provided the initial catalyst for GBP/USD to recover from the low $1.20's, we believe that sustained sterling appreciation will need more than just a squeeze in speculative positioning. To us, the easy gains in GBP have been made," says BofA's Sharma. "We think at least in the near-term that the UK macro/rates outlook will increasingly come to dominate GBP price action."

Pound Sterling enjoyed parity between the BoE's Bank Rate and the Fed Funds rate of the Federal Reserve (Fed) at the time of the referendum, which matters when it comes to the outputs of financial models that attempt to estimate things like 'fair value'. And the two economies enjoyed broadly similar rates of economic growth, which is also important for model outputs.

However, all of that has since changed and the Pound is now disadvantaged by an interest rate differential that leans 100 basis points, or 1%, in favour of the Dollar. It's also being hampered by an economic growth rate of just 0.6% for the 12 months to the end of November, which is far below the BoE's estimate of the economy's inflation-producing rate of expansion, not to mention an actual 1.3% inflation rate that's a long way off the 2% target of the BoE.

The UK economy is deteriorating at the same time as the U.S. economy demonstrates its resilience in the face of a global downturn, with the annual rate of U.S. GDP growth still in excess of 2% at the last count. That matters when it comes to fair value for the Pound-Dollar rate and so too does the fact that investors have this month gone 'all-in' with wagers the BoE will cut Bank Rate from 0.75% to 0.50% on January 30. The Fed Funds rate remains at 1.75%.

Above: Logarithmic scaled price chart depicting Pound-to-Dollar rate at monthly intervals.

Sterling was frequently described as 'overvalued' when it traded between 1.50 and 1.70 in the post-crisis, but pre-referendum years. And that was a period when it had either an interest rate differential in its favour (25 basis points) or when it benefited from parity between central bank rates.

But if expectations crystallize into a rate cut reality at month-end then the UK-U.S. rate differential will move to 125 basis points in favour of the Dollar. And that might mean it's only a matter of time before investors begin to reconsider the question of an appropriate long-term fair value for the exchange rate.

"We are sympathetic to the views of the IMF in its 2018 Article IV Consultations that GBP could be anywhere from 0%-15% overvalued," Sharma says. "We have previously argued that GBP was undervalued versus some of its key macro anchors such as growth and the housing market following the EU Referendum. The same cannot be said now which is why we leverage our higher GBP call on the ability of the UK/EU to either strike a deal this year, or more likely agree on a transition extension."

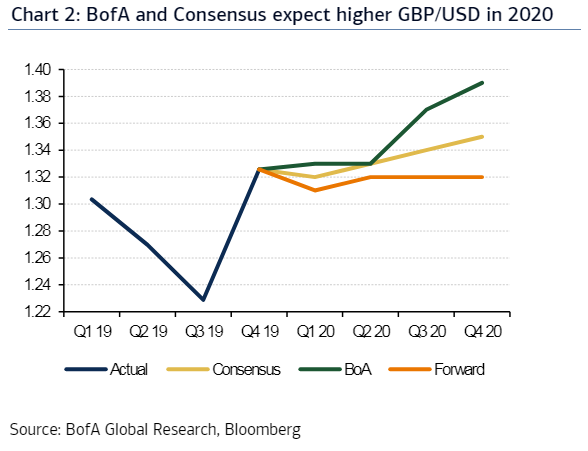

Sharma and the BofA team forecast a higher Pound-Dollar rate at year-end although they envisage more of a slow grind to the upside than a big rally.

Above: BofA Global Research forecast path relative to market expectations.

BofA's forecast is determined partly by an expectation of a turn lower in the Dollar, and the remainder the assumption the UK and EU will either amicably agree a future relationship or settle for extending the transition period that's currently expected to run between January 31 and beginning of 2021.

The bank forecasts the Pound will rise to 1.33 by the end of March and remain close to that level until the end of June, when it's expected to begin climbing toward 1.37 before eventually seeing out the year at 1.39.

Much of Sterling's movement is anticipated in the second half of 2020 because the UK has until July to decide if it wants to request an extension of the transition period. Boris Johnson currently says that won't happen although he also said the October 31 Article 50 deadline wouldn't be extended.

"A long term technical view of a developing double bottom points as high as 1.60. Price action still has a lot to do to prove this, however the structure exits. In 2020 conviction in a bottom pattern increases above 1.35 and decreases below 1.25. A decline through the trailing lows circa 1.20 reminds us of an old risk, a full downside target of 1.08," adds chief technical strategist Paul Ciana.

Above: BofA Global Research technical analysis of long-term Pound-Dollar trend. Depicts possible double bottom pattern.