Image © Adobe Stock

- Exporter should consider lightening up hedging ratios as interest rate differentials invert

- More favourable conditions for importers to hedge

- Long-term NZD/USD short positions favoured due to carry advantage

New Zealand exporters should consider 'dropping the hedge' on NZD/USD exposure now interest rates are no longer in their favour and the 'free lunch' premium they used to enjoy on forward rates has inverted say BNZ Bank.

The New Zealand Dollar has weakened amidst diverging interest rate expectations with US rates now higher than New Zealand (2.0% vs 1.75%), this makes it more beneficial for traders to hold long-USD/short-NZD positions as they stand to gain a carry profit of 0.25% simply for being in the trade.

This has significant implications for the various actors in the NZD/USD FX market, including currency speculators, exporters, importers and fundmanagers, according to a recent research report by BNZ bank.

Previously NZ exporters used to have more incentives to hedge their 'repatriations' back into Kiwi's.

Not only was there a greater risk they could lose money from exchanging back into a stronger Kiwi but if they hedged using a forward contract they could lock in a forward rate at a premium because interest rates in new Zealand were the highest in the G10.

Effectively this meant they were compensated in a better forward rate, providing them, with a 'free lunch'.

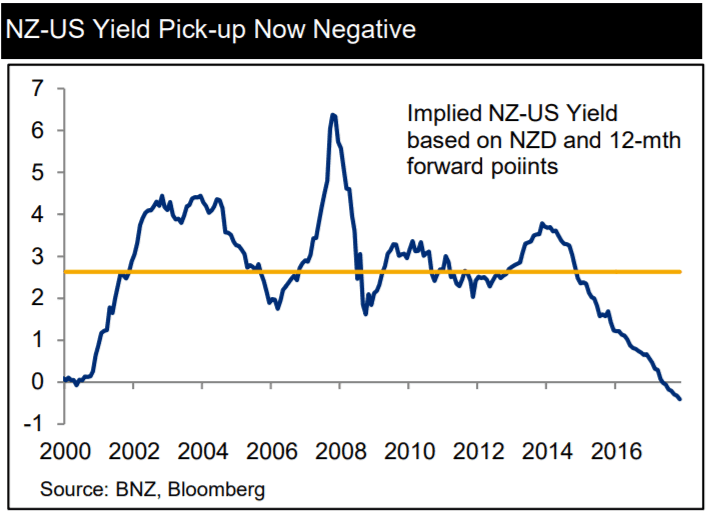

Now, however, the opposite is true. Due to US interest rates surpassing NZ rates, FX forward rates are discounted instead, as shown in the chart below, which measures the basis points an NZD/USD 12-month forward contract is discounted due to interest rate differentials.

In addition, the Kiwi is more likely to weaken (to their benefit) due to lower relative interest rates so a hedge is less necessary.

Expectations for further NZD weakness come as the currency continues to struggle and nurses a 7.5% loss against the US Dollar in 2018 as well as a loss of 3.60% against the Pound and a 4.0% loss against the Euro.

In anticipation of further losses New Zealand exporters should consider hedging less, advises Jason Wong, chief FX researcher at BNZ.

"Strategically we see some merit in exporters and local fund managers targeting a lower than usual hedging ratio over the next few years. The flip-side is that importers should see more benefit in hedging foreign exchange," says Wong.

It is now more advantageous for importers to consider hedging against Kiwi weakness as they stand to enjoy the premium on forward rates, and because of the risk a weaker Kiwi could leave them short when it comes to settling up.

"We see some merit in importers in targeting higher hedge ratios than they have typically maintained, with the added benefit of reduced costs," says Wong.

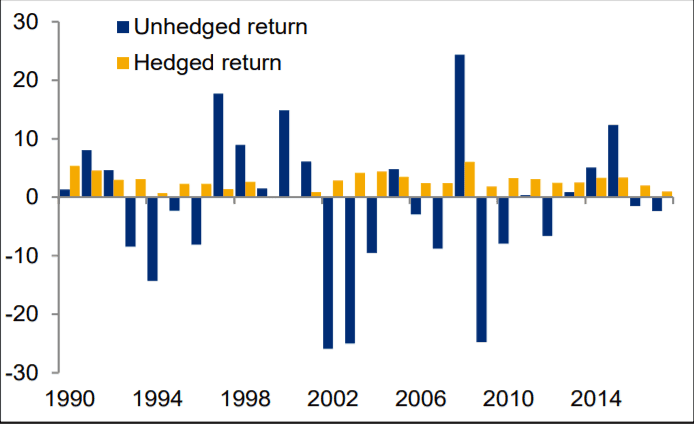

Whilst historically it is more sensible to hedge than not (see chart below) Wong thinks there may be some merit in exporters reducing hedging ratios anyway.

The diverging outlook for interest rates in the US and NZ will lead to increase hedging costs and probably a weaker Kiwi, which makes it even less worthwhile bothering with a hedge.

"Given our outlook that NZ interest rates remain steady against a backdrop of higher US rates, some exporters and local investors might be tempted to keep hedging ratios lower than usual. In that interest rate environment, it is difficult to see the NZD “taking off” and strongly appreciating. Thus, we see some merit in exporters and local fund managers strategically targeting a lower than usual hedging ratio," says Wong.

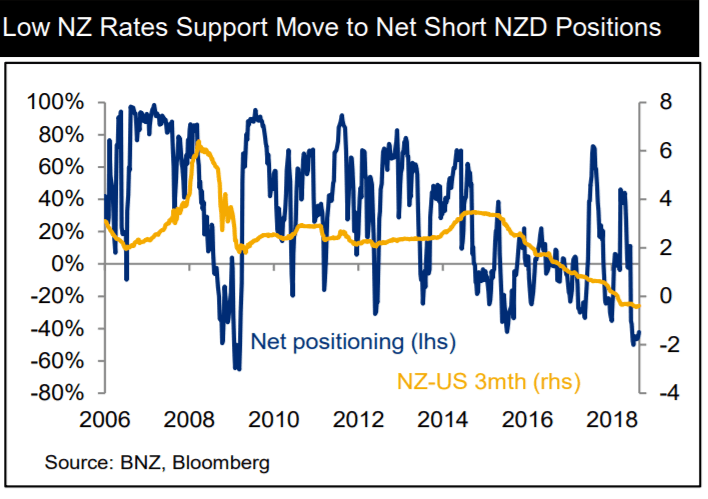

The inversion of the rate differential on NZD/USD now also means that speculators are more likely to hold long-term short positions rather than long-term long positions since they only gain on the positive carry from the former.

"Historically, NZ has enjoyed higher rates relative to the US and this has encouraged the “hot money” to be long NZD and pick up the yield carry. Over recent years, the lower NZD-US rate differential has seen an increasing move towards short NZD positioning," says Wong.

This has implications for the interpretation of positioning data. Normally when positioning reaches a short extremes it is taken as a contrarian indicator that a 'short squeeze' may happen and the underlying assets will start to rise, however, given there is now a carry advantage in holding short NZD long-term the bullish implications are less pronounced.

Where positioning data is useful is when analysing long positions, which when they reach an extreme are likely to be a more reliable indicator of a top forming in the underlying asset.

"Whereas previously we would have suggested that the current level of short positioning might threaten a short squeeze and therefore a contrarian view might be appropriate, short NZD positioning in the current environment could well be sustained for an extended period," says Wong. "Unlike the current status quo, this positioning indicator is likely to be a much better contrarian signal when net positioning is long NZD than short."

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here