An A-list appointment to head the RBNZ, higher public spending and rising inflation may not be enough to make up for a fading carry trade and continued political risk next year.

New Zealand’s Dollar could weaken further in the months ahead because times are a changin and, with a static Kiwi cash rate, rising interest rates in the rest of the world are set to diminish the relative attractiveness of the currency in 2018.

The currency has already lost ground through 2017 due to fears over the impact NZ politics will have on the economy and inflows of foreign capital, while analyst assessments for 2018 remain mixed.

My Turkish friend used to say: "Money makes money," by which he meant the more money that you have, the easier it is to make even more of it.

Nowhere is this truer than in the world of high-finance where capital provides an elite group of financiers with the means to take advantage of opportunities not available to mere mortals.

The 'carry trade' is one of the tools in their kit - a method by which international investors can take advantage of differences in global interest rates to make money.

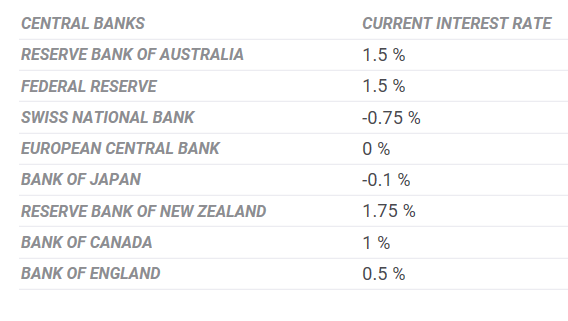

Carry trading involves borrowing in a currency where interest rates are exceptionally low, such as in the Eurozone, and placing that money in a jurisdiction where interest rates are relatively high, such as New Zealand.

Cash rates are at 0% in Europe while, in NZ, they are currently at 1.75%. This means traders can borrow in Europe for nothing, or close to nothing, and invest in New Zealand where they receive a minimum of 1.75% per year in interest.

This is the “carry trade” and, with foreign currency risk aside, it’s like shooting ducks in a barrel. Could there be an easier way of making money?

In reality, it isn’t that simple. Movements in exchange rates can wipe out profits easily if traders pick the wrong currency to buy with their cheap money or if trades aren’t timed properly.

If EUR/NZD rose by 1.75% in a year (it is up 11.75%) then the extra interest income alone would not be enough to compensate investors. But traders can also make money from movements in bond prices and will take foreign exchange into account when making their bets.

This is the context in which currency strategists have been analysing “high yielding” commodity currencies such as the Aussie, Kiwi and Canadian Dollar, all of which have enjoyed higher interest rates compared to the rest of the G10 world ever since the financial crisis.

With interest rates now rising elsewhere in the world, times are a changin for these currencies, as the “carry interest” that has propped them up in recent years is set to fall.

This means demand for New Zealand Dollars, from carry traders, is set to diminish and strategists say this could mean a further weakening of Kiwi Dollar in the next six months.

"In a synchronised global tightening cycle, a latent RBA and RBNZ policy response would reduce the 'high-yielding' attractiveness of the AUD and NZD," says Viraj Patel, an FX strategist at ING Bank.

The Reserve Bank of Australia (RBA) and the Reserve Bank of New Zealand, who set the base interest rates for both countries, have found their hands tied when it comes to raising interest rates during recent years.

"Dollar Bloc central banks will be at the dovish end of the spectrum in 2018 and this will see the theme of depleting carry advantage continue," Patel adds.

Above: Table showing G10 country interest rates.

Although both economies have notable strengths - the Australian labour market and recent NZ business confidence - this is not translating into higher inflation and it is only in response to higher inflation that central banks will raise interest rates.

And even if growth and inflation start to pick up next year, as is expected, there are other factors that are expected to keep interest rates low.

First, what central bankers call 'financial stability risks' may prove a headwind. Highly indebted households may not be able to cope with higher interest rates after years of low-to-no pay growth.

Levels of private debt are exceptionally high in both countries, partly as a result of the housing booms, and prices of everyday goods have risen faster than wages during recent years.

This is a powerful disincentive for the central bank to raise interest rates as higher rates might have negative knock-on effects for the economy, since consumers will be less able to spend if they have more money going out to service debts.

Politics are Still a Threat

Recent weeks saw the New Zealand Dollar earn some respite from its 2017 sell off but the new Labour-led coalition government’s politics will remain a threat to the currency during the coming months.

The main fears surrounded the new government have been centred on policies that are seen hindering foreign investment in the short term and weighing on economic growth in the longer term.

New restrictions on foreign purchases of residential property and farmland are seen as discouraging for investors.

A looming shake-up of the RBNZ, with the introduction of a committee to make decisions and a mandate to target full employment, has led to fears over central bank independence and the Kiwi interest rate outlook.

The recent appointment of a new governor of the RBNZ has helped to offset some of the concerns around the central bank reform and Kiwi interest rate policy.

“He currently runs the New Zealand government’s sovereign wealth fund, which has returned 16.2 percent per annum over the last five years," says Boris Schlossberg, a managing director at BK Asset Management.

Adrian Orr, who heads the NZ sovereign wealth fund and is seen as a highly competent appointment, will takeover at the top of the bank in 2018. He has a track record in central banking after having served as a deputy governor there earlier in his career.

"Investors were reassured that he will keep monetary policy on an even path, restraining the worst impulses of a stimulatory fiscal policy," says Kathy Lien, also a managing director of foreign exchange strategy at BK Asset Management.

But Orr’s appointment alone will not be enough to safeguard the New Zealand Dollar from further losses, as the fallout from the government’s maiden budget highlights.

Prime Minister Jacinda Ardern’s maiden budget, last week, announced a large increase in public spending, which are normally stimulatory for economies and positive for currencies.

Markets shrugged off the fiscal stimulus and sent the New Zealand Dollar lower on the day after critics took issue with overly “optimistic” growth and borrowing forecasts.

"While the policy uncertainty of a Labour-NZ First coalition has seen NZD sell-off in recent months, we do expect the currency to stabilise as the dust settles on the new government," says ING's Patel.

Patel actually forecasts upside risks for the New Zealand Dollar over the longer term due to the potential for the RBNZ to move off the sidelines and possibly raise interest rates in the second quarter of 2018. This would lead to a potential 5.0% rise in the NZD/USD pair.

"It’s all about timing the turning point and we're eyeing up a positive re-rating in 2Q18 that sees NZD/USD up +5.0%," says Patel.

However, not all share this positivity, with J.PMorgan analyst Paul Meggyesi saying the RBNZ is an "unlikely candidate to signal tighter policy."

Stricter immigration controls will lead to lower growth, among other things, and prevent the RBNZ from raising rates in the new year says, according to a recent note from the strategist. Meggyesi says the RBNZ will remain po-faced despite rising inflation over the coming years.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.