The Pound to New Zealand Dollar exchange rate is broadly moving sideways with a slight upside bias, it is expected to extend higher in the week ahead – or at the very least continue sideways, we see the least likely outcome as further weakness.

Our analysis is based on a signal on the monthly chart which impacts on the daily chart and will probably influence the outlook for the coming week.

The monthly chart is showing that the past two months were red down months which occurred within the early stages of an uptrend.

According to research, when this happens the following month has a higher than 50% probability of being an up-month, in fact on EUR/USD research has shown a 66% probability that it will be green.

July is already green and there is therefore a higher than 50% probability it will remain green, which is a bullish indicator for the rest of the month’s activity.

Indeed, looking at the daily chart, this is not hard to believe, given the bullish look and feel of the chart which suggests - to my eye at least - a propensity for a move higher rather than a move lower.

The MACD momentum indicator in the lower panel is also rising and converging bullishly with price action which remains broadly sideways and chaotic.

This suggests ‘pent-up’ buying potential which should eventually express itself in a continuation higher.

A break above the range highs at 1.7910 would probably confirm such an extension up to a target at an old resistance line at 1.7990.

Get up to 5% more foreign exchange by using a specialist provider. Get closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here

Data for the New Zealand Dollar

The main release for the New Zealand Dollar (Kiwi) in the week ahead is Q2 inflation data out at 23.45 on Monday, July 17.

Inflation has been rising quite strongly in New Zealand and it is expected to continue, albeit at a slightly more modest rate.

The consensus amongst analysts is currently for a slow down to 1.9% year-on-year rise (ie compared to Q2 last year).

This would be lower than the 2.2% registered in Q1.

Canadian investment bank TD Securities are more sceptical, expecting it slow even more to 1.7%, as fuel deflation erodes.

The RBNZ have forecast 2.1% result and if it matches or exceeds that – which is very well might – then the Reserve Bank of New Zealand may become more hawkish, which would lead to a rise in the Kiwi.

Yet given the above technicals and ‘seasonality’ such a push higher in prices would be surprising.

“As the RBNZ expected 2.1%/yr in the May monetary policy statement (MPS), a softer outcome justifies Wheeler remaining neutral at the 10 August MPS and into his late Sept retirement.

“Fuel –3.0%/qtr implies private transport -2.1%/qtr and negative tradable inflation (f/c -0.8%/qtr). Housing construction (+1%/qtr) so domestic inflation pencilled in at +0.7%/qtr. However, domestic seasonality suggests lower domestic inflation,” said TD.

Data for the Pound

The standout release for Sterling in the week ahead is June Inflation data which is out at 9.30 BST on Tuesday July 18.

The release is important because it impacts on the decision making of the Bank of England (BOE), which in turn is a major driver of the Pound.

Inflation has risen steeply after the Pound weakened following the referendum, which had the consequence of pushing up the prices of imports.

Inflation in May stood at 2.9% year-on-year (yoy: ie compared to May 2016), and 0.3% month-on-month (mom).

The consensus amongst analysts is that it will remain at 2.9% in June yoy but rise at a lesser 0.2% mom.

However, Canadian Investment Bank TD Securities think the market is being too dovish and forecast a higher 3.0% rise in inflation.

TD expect Core inflation to come out at 2.6% which is the same as the market.

A rise in the cost of utilities is likely to be the driving force behind higher broad inflation and stable core.

“Inflation is likely to have continued its march upward in June, in part due to utility price increases. Core inflation, meanwhile, is likely to have remained stable.”

Nor do TD see this as the “peak for inflation” as core could rise 1 or 2 basis points and headline could rise to the “min-3% range”, which would, “head up the debate about a (single) rate hike later this year.

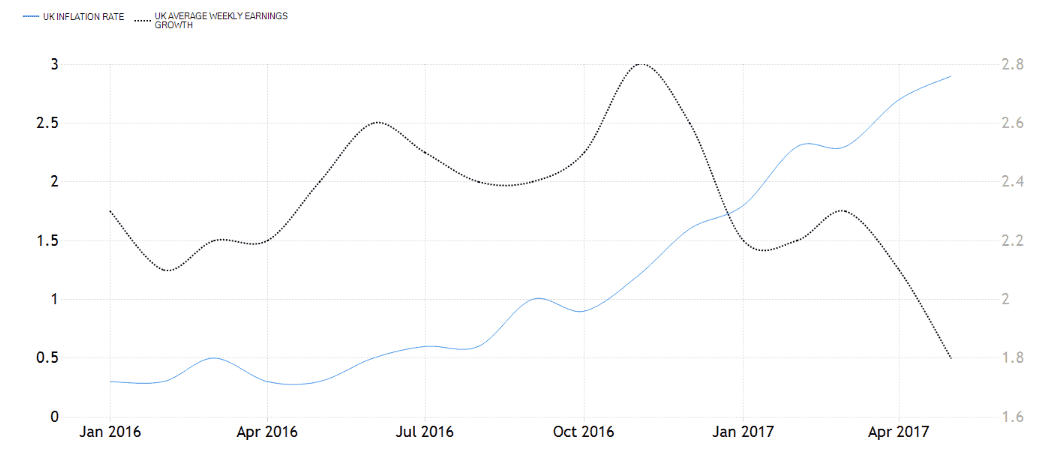

Incidentally the divergence between slowing average earnings in the UK and rising inflation is probably the root cause of the slowdown in the high street or “consumption” as economists like to call it.

The drag on growth from people spending less money is likely to keep the hawks at the BOE in check and limit any possibility of a rate hike.

We know Carney for one won’t change his view until the “trade-off” facing the MPC “continues to lessen” by which he means the trade-off between slowing growth and rising inflation.

Which brings us on to the other major release of the week for Sterling – Retail Sales on Thursday, July 20 at 9.30.

The market is currently being very optimistic about the gains expected in June.

They see headline Sales rising 2.6% yoy – which is a big jump from the previous 0.9% print; and Core increasing 2.4% from May’s very much lower 0.6% rise.

The market also expects a monthly rise of 0.4% for headline and 0.5% for core from -1.2% and -1.6% respectively in May.

This turnaround appears hugely optimistic from both our and TD Securities perspective, and seems to have little logic backing it up.

TD are of the opinion that Sales will not rise by anything (0.0%) mom in June rather than the 0.4% suggested by the market – we agree.

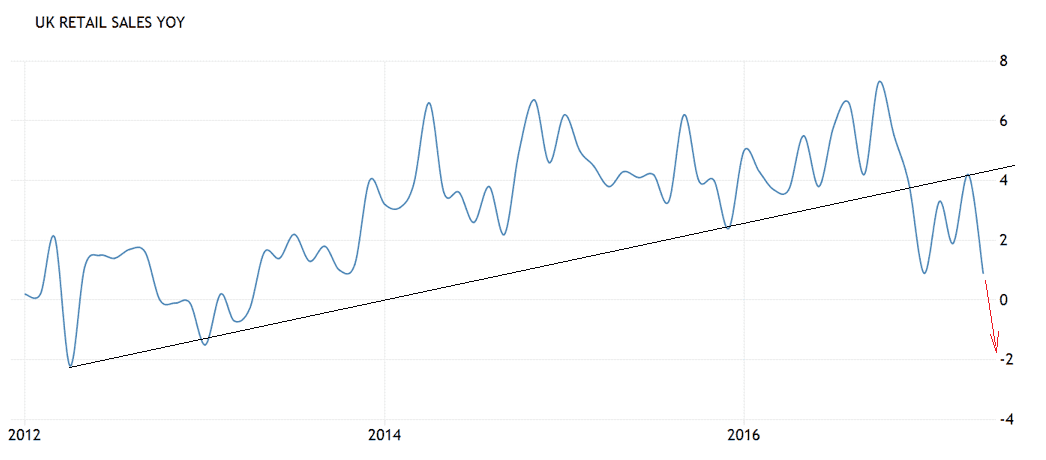

The picture below showing historical Retail Sales data shows a breakdown in the prior up-trend which gives the outlook a definite bearish hue.

The look and feel of the chart betokens a more negative print next Thursday than a more positive, which would also make more sense given the fall in real earnings.

BK Asset Management’s Kathy Lien, however, thinks there is a chance of a better-than-expected print:

“The smaller decline in shop pricesand the uptick in BRC retail sales monitor points to stronger numbers that should help rather than hurt the GBP/USD rally,”

Whilst this fits with the bullish technical outlook we, nevertheless, retain a negative bias.