RBC Capital see the NZ Dollar remaining supported owing to continued currency inflows from foreign investors seeking higher interest on their investments.

- Pound to New Zealand Dollar exchange rate (14/9/16): 1.8135, see live rate here

- Euro to New Zealand Dollar exchange rate (14/9/16): 1.5422, see live rate here

- Australian to New Zealand Dollar exchange rate (14/9/16): 1.0271, see live rate here

- New Zealand to US Dollar exchange rate (14/9/16): 0.7282, see live rate here

NZD has shown a rare vulnerability to the EUR, USD and even GBP of late as Asian and commodity-linked currencies fall out of fashion.

The declines in this broad complex of currencies is linked to growing expectations for interest rates to rise in the United States.

When US rates rise, global growth tends to slow as the cost of borrowing money in an USD-denomintated world rises.

This therefore has implications for commodity prices and for a commodity exporting nation like New Zealand currency inflows may take a knock.

That said, it remains hard to bet against the NZD and eyes will return to domestic issues on Thursday the 15th September when the release of the latest set of GDP data will remind us that the economy remains in rude health.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3528▲ 0%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2728 - 2.2822 |

**Independent Specialist | 2.3199 - 2.3293 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

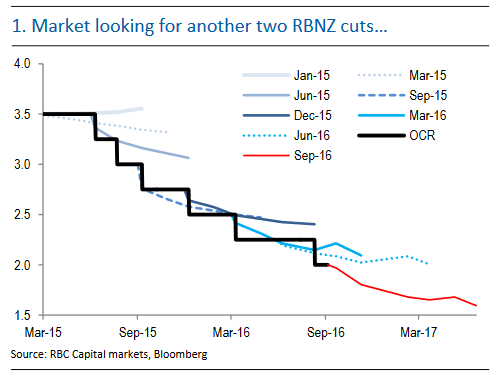

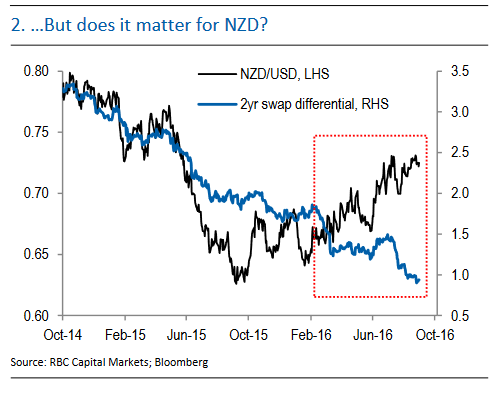

The NZD continues to strengthen even in the teeth of interest rate cuts by the Reserve Bank of New Zealand (RBNZ), which reduced rates from 2.25% to 2.00% in August.

Lower interest rates in the current climate would be expected to lead to a fall in the host currency as they attract less inflows of foreign capital seeking higher returns.

The kiwi has studiously ignored falling interest rates and continued strengthening. What could explain this apparent contradiction?

The answer appears to be that New Zealand rates, though they have fallen, are still much higher than most other G10 countries.

The UK now has a 0.25% base lending rate, the Eurozone 0.0%, Japan a negative -0.1%, the US 0.5%, Canada 0.5%, Australia 1.5% and so on.

In comparison to these New Zealand’s high 2.0% rate is actually several multiples higher.

In addition, the country (unlike the UK and US) has retained its AAA credit rating, making it a sure as well as a lucrative bet.

The reason the kiwi is so strong is via a form of investment called the ‘carry trade’ which seeks to profit from interest rate differentials.

The carry trade operates by investors borrowing money in a low interest rate currency like the yen or the euro and putting that money into New Zealand, either as an investment in bonds or simply in a bank account.

The money is then earning about 2.0% interest in New Zealand at a cost of only 0.0% in the Eurozone for example.

The investor pockets the difference – or 2.0% in this case.

This sort of trading has become more aggressive in the new zero-interest rate world of global financial markets since investors have access to money for next to nothing.

“We have revised our NZD forecasts substantially higher this month. We underestimated the importance of carry as a driver in G10. It has been an important source of support for AUD and NZD and it could run further from here," says Elsa Lignos of RBC Capital.

RBC believe that while the RBNZ is likely to cut again NZD will still remain the highest yielder in G10.

“With that in mind we have revised up our end - 2016 forecast to 0.78," says Lignos.

Further supporting the outlook for a stronger NZD is an improving balance of trade, due to rising dairy prices and rising exports of new horticultural exports such as kiwifruit, wine, apples and seafood.

“In real terms, NZ’s trade balance is showing some improvement driven by services. But exports of non-commodity goods continue to decline. NZD is well above its long-term average real effective exchange rate,” says Lignos.

In the long-term RBC forecast the pair to weaken as the difference between rising US interest rates and falling - or stagnating New Zealand interest rates – reduces the kiwi’s advantage and results in more flows going to the US and the kiwi losing its primary crutch.

But, Lloyds Commercial Banking See NZD/USD Falling

In contrast to RBC Capital's forecast of a rise to 0.78 by the end of 2016, Lloyds Commercial Banking’s Jeavon Lolay sees the pair falling to 0.69 by the end of the year, as US rates rise and New Zealand interest rates fall.

“At its August policy meeting, the RBNZ cut interest rates from 2.25% to 2.00%. Despite the upbeat domestic outlook, it is likely to exercise caution from a policy perspective as inflation expectations remain anchored near all-time lows and the currency displays persistent strength,” said Lloyds’s Lolay, adding:

“Given the scope for policy divergence through to the end of the year, we anticipate NZD/USD declining towards 0.69 by end-2016.”

It seems the difference in the two analyses lies in the speed with which the two rates converge, but given recent poor ISM data for August and commentary on Monday the 12th from Fed’s Lael Brainard, who urged “prudence”, the Fed still lacks the consensus necessary to push through another rate hike in 2016.

Likewise the strong domestic economy and continued hot housing market in New Zealand corners the Reserve Bank of New Zealand to some extend making it difficult for it to manoeuvre or ease policy, especially not rapidly enough to impact the exchange rate.

As Lignos says in her report on the currency, governor Wheeler himself has suggested aggressive rate cutting is not on the radar.

Accordingly, it is hard to argue rate dynamics can drive NZD lower when

(1) they clearly haven’t mattered so far and,

(2) the RBNZ would need to deliver more than two cuts to ‘surprise’ the market.

“Comments from Wheeler seem to rule that out , we do not believe that the outlook of balance of risks = warrants a position of no policy change, nor a position of rapid easings,” she notes.

And Lignos quotes the sort of deep Swedish-style cuts required to really bring the kiwi down to fair value, would, according to Wheeler, “overheat the economy”.