The British pound remains supported against the NZ dollar after the Reserve Bank of New Zealand (RBNZ) shifted into 'easing' gear at their January 28 meeting.

The Reserve Bank of New Zealand’s January rate meeting saw no changes to policy announced - as expected by markets. However, the message we take away is NZD-negative as the prospect of a rate cut in coming months has grown.

At the last meeting they made a 0.25% cut to 2.5%, and the Bank said they would be reviewing the flow of economic data before deciding to make another cut.

The message from the January meeting is that, “some further policy easing may be required”.

"We got a clearer easing bias in the RBNZ statement, but not an explicit signal that the RBNZ will necessarily cut the OCR as soon as March. Global risks, rather than a sea change in the inflation outlook, seemed more influential in shifting the RBNZ’s stance," say A.S.B in a client note in the wake of the release of the RBNZ's statement.

A.S.B say they continue to expect the RBNZ to cut the OCR 50bp in 2016, starting from June.

The risks to that forecast remain for a slightly earlier start.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3513▲ + 0.12%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2713 - 2.2808 |

**Independent Specialist | 2.3184 - 2.3278 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Fitch Undermine the Kiwi Dollar

The kiwi, meanwhile, is currently languishing after Fitch Ratings down-graded the outlook for the country to 'stable' from 'positive'.

Fitch downgraded the outlook partly on a predicted deterioration in agricultural exports.

It revised down its assessment of New Zealand's near-term growth prospects as a result and it also cited uncertainty over migration rates and the El Nino weather pattern.

Fitch expected New Zealand's gross domestic product to pick up in the next two years but at a slower pace than previously forecast.

With weaker growth prospects came slower-than-expected debt reduction.

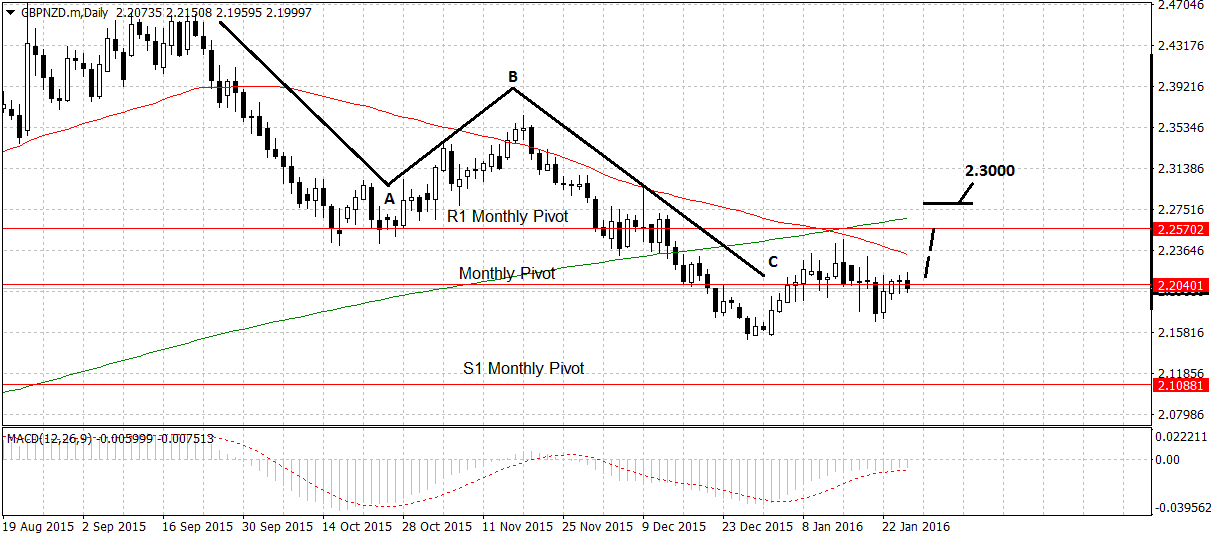

GBP to NZD Forecast: Base Building

A technical analysis, meanwhile, shows a possible foundation building on pound-to-kiwi, with the potential for a new rally higher (sterling positive; kiwi negative), however the new rally has not been confirmed and much resistance lies above.

This includes the monthly pivot at around the current trading level, at 2.2040, the 50-day MA just above at 2.2335, the R1 Monthly Pivot at 2.2570, and then the 200-day MA at 2.2669.

Whilst there are compelling signs the exchange rate may be about to move higher in a third wave up, which could eventually reach the R1 Monthly Pivot at 2.2570, these strata of resistance present a risk the up-move could fail, therefore, ideally I’d want to see aclearance right above the 200-day MA, completely ‘out of the woods’ before confirming a move higher to 2.3000.

Fitch Cites Increasing Indebtedness

Fitch’s downgrade of the outlook for New Zealand from “Positive” to “Stable” on the 26th may not have been factored in by the economists in the Bloomberg survey cited by Juckes, and raises the possibility that this new information may have increased the chances of a surprise RBNZ cut.

Fitch’s main reasons for the down-grade was a rise the New Zealand’s government’s own projections of the country’s indebtedness, from 23.8% of GDP in 2014 to 28.3% in its most recent projections.

The debt agency, however, also warned of the risk of a ‘negative shock’: “such as a steep rise in external borrowing costs, prolonged weakness in the dairy sector, or sharp reversal in house prices.”

Under the Hoof

Finally, a prolonged period of low dairy prices were also a factor influencing Fitch’s decision:

“a potential deterioration in asset quality caused by the softening economic environment, particularly in the dairy sector. A second season of low dairy prices has affected the debt-servicing ability of farmers, with around half of the dairy sector estimated to be facing negative cash flow during the 2014-15 season.”

Overall the New Zealand dollar has been under pressure in the later part of January, as a result of the negative inflation data and further weakness in dairy prices prompted by the fears surrounding a hard-landing in China.

At the last Global Dairy Auction on Monday 19th , dairy prices declining by 1.4%, to an average price of $2,405, from the previous week’s $2,458.

According to Farmers’ Weekly, recent research has shown that world milk output is running well above recent averages and is expected to rise a further 1.0% in 2016, indicating the possibility of further downwards pressure on dairy prices in the future.