- GBP/NZD supported near 1.94 & sharp rally possible

- Scope to advance above 1.96 & could approach 2.00

- If RBNZ rate decision or forecasts disappoint market

- Decision, forecasts could quibble with market pricing

Above: RBNZ Governor Adrian Orr. File Image © Pound Sterling, RBNZ

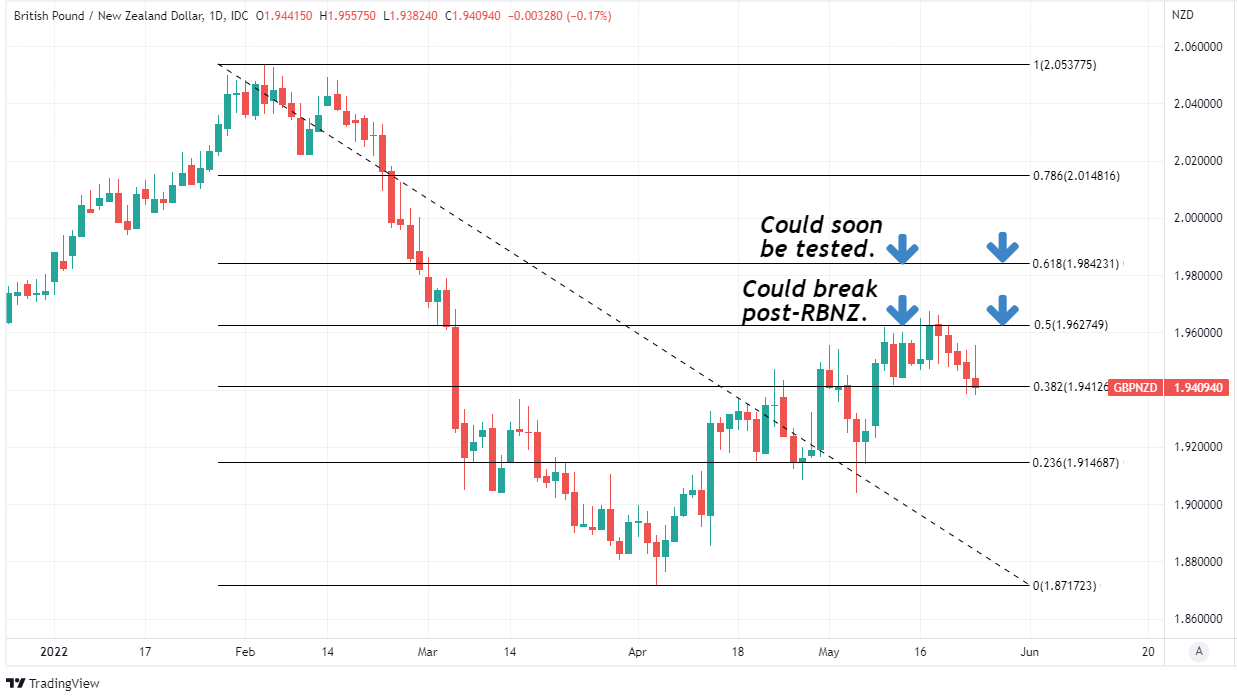

The Pound to New Zealand Dollar rate has been volatile from the outset this week but could rally above 1.96, or even approach the two-for-one level if Wednesday’s Reserve Bank of New Zealand (RBNZ) interest rate decision or forecasts disappoint lofty financial market expectations.

Sterling slumped broadly on Tuesday in price action that pulled GBP/NZD back down to the round number of 1.94, entirely reversing Monday’s sharp rally after the May series of IHS Markit PMI surveys hinted of a darkening outlook for the UK economy in the months ahead.

But it could reverse these losses and potentially even trade up to levels not seen since before Russia’s late February invasion of Ukraine if the RBNZ quibbles with financial market expectations for its cash rate this Wednesday.

“It’s not going to be the 50bp hike that’ll get attention (it’s universally expected), but rather the tone and forward guidance. If the RBNZ can allay fears of a hard landing and preserve optionality in 2022 H2, that’d probably be pretty well received in FX markets,” says David Croy, a strategist at ANZ.

The RBNZ is widely expected to lift its cash rate from 1.5% to 2% on Wednesday when it announces May’s monetary policy decision and publishes its latest forecasts for the New Zealand economy and related variables.

Above: Pound to New Zealand Dollar rate shown at daily intervals with Fibonacci retracements of February decline indicating various areas of technical resistance to any further recovery by Sterling. Click image for more detailed inspection.

The potential rub for the Kiwi is that another large 0.5% increase in the cash rate cannot be taken for granted and neither can an endorsement of the market’s expectations for borrowing costs in the months and quarters ahead.

The RBNZ lifted its cash rate by 0.50% for the first time in more than two decades in April but most pertinently for this Wednesday’s decision, it also indicated strongly that further steps of that magnitude are far from assured.

“The Committee remained comfortable with the outlook for the OCR as outlined in their February Monetary Policy Statement. They agreed that moving the OCR to a more neutral stance [estimated to be around 2%] sooner will reduce the risks of rising inflation expectations. A larger move now also provides more policy flexibility ahead in light of the highly uncertain global economic environment,” the RBNZ said prominently in April’s statement.

This language is notable for various reasons but not least because the RBNZ said in February that it estimated a “more neutral” level of the cash rate to be only around 2% while its projections implied that its cash rate would be unlikely to rise beyond the 2.25% level this year.

That potentially primes leaves the New Zealand Dollar at risk of an upset this Wednesday and one that could push the main Kiwi exchange rate NZD/USD back to its recent low around 0.6231, which would be a favourable outcome for the closely-linked but often inversely correlated GBP/NZD.

Above: NZD/USD at weekly intervals with Fibonacci retracements of 2020 recovery indicating possible medium-term areas of support for the Kiwi and shown along with GBP/USD. Click image for more detailed inspection.

Above: NZD/USD at weekly intervals with Fibonacci retracements of 2020 recovery indicating possible medium-term areas of support for the Kiwi and shown along with GBP/USD. Click image for more detailed inspection.

This is in part because the financial market implied path for the cash rate suggests that it will rise to 2% on Wednesday and to 2.5% in July, with further increases then seen taking it to 3.25% or more before year-end.

“While the OCR has been increased in recent quarters, it remains below the Reserve Bank’s estimate of a nominal neutral interest rate of about 2 percent,” the RBNZ had said in its February Monetary Policy Statement.

The risk is that the elevated level of inflation in New Zealand and resilience of the domestic economy lead the RBNZ to conclude this week that the cash rate has to rise further than was previously envisaged in order to bring price pressures under control in the years ahead.

GDP growth and inflation were modestly above RBNZ forecasts in the fourth quarter 2021 and first quarter 2022 respectively but it remains to be seen whether they were strong enough to prompt the RBNZ to remain on the interest rate path currently priced into financial markets.

“The majority of members from the NZIER shadow board reportedly opted for a 50bp May OCR hike, consistent with the market consensus (including ourselves),” says Mark Smith, an Auckland based economist at ASB Bank.

“The focus will be how far beyond circa 2% neutral levels the RBNZ would be prepared to push the OCR, and for how long,” Smith said on Tuesday.