- NZD outperforms on house price growth, china sentiment.

- CoreLogic data shows double-digit price surge continuing.

- Lifting NZD as risk appetite steadies, Chinese stocks rise.

© Adobe Stock

- GBP/NZD spot rate at time of publication: 1.8820

- Bank transfer rate (indicative guide): 1.8160-1.8292

- FX specialist providers (indicative guide): 1.8537-1.8687

- More information on FX specialist rates here

The New Zealand Dollar rose broadly on Tuesday as the antipodean country's latest house price figures were seen posing as a further deterant to additional Reserve Bank of New Zealand (RBNZ) interest rate cuts and as investors chased assets that offer exposure to China.

New Zealand's Dollar was higher against all major rivals except its Australian counterpart as market risk appetite appeared to stabilise and investors showed a preference for assets that offer a proxy exposure to China's economy and financial markets.

This is after Chinese stocks outperformed global counterparts in the overnight session following a New York Stock Exchange decision not to move ahead with an earlier announced plan to push three Chinese telecoms firms off of the exchange.

The decision was seen as positive for U.S.-Chinese relations as well as the global economic outlook so offered a tailwind to commodity currencies like the Kiwi and Australian Dollars, although the New Zealand Dollar was also supported by domestic house price data.

"NZD/USD recovered above 0.7200. New Zealand house prices increased at an annual pace of 11.1% in December 2020, the most since May 2017. The red‑hot housing market reduces expectations for additional RBNZ policy rate cuts and is NZD supportive," says Elias Haddad, a senior FX strategist at Commonwealth Bank of Australia.

Above: NZD/USD shown at weekly intervals.

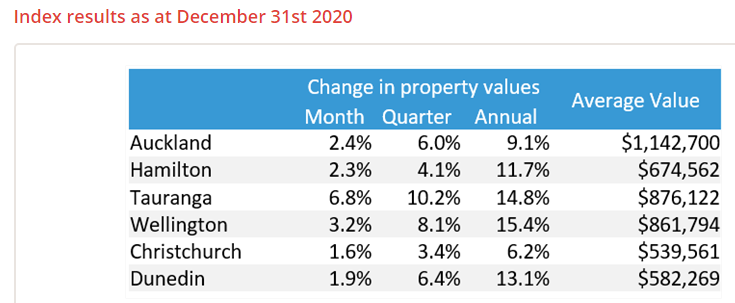

CoreLogic NZ data revealed overnight that New Zealand's house prices continued to rise steeply into year-end amid rising investment demand and limited supply, taking annual price growth comfortably into the double-digits for 2020 in some parts of the country.

Rising house prices and government concerns about affordability for first time buyers have led to tension between the RBNZ and Treasury in recent months, with one side effect being that investors now see political objections making a shift to negative interest rates in New Zealand less likely for the year ahead. As a result investors have gone from betting in October that New Zealand's cash rate would be cut far below zero this year, to wagering that it remains unchanged at 0.25% over the coming years.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

"It is clear that New Zealanders are looking towards property as a safe investment and the most attractive asset for wealth accumulation," Core Logic says. "Without any major policy change regarding property in the works, the long term affordability of the property market is reliant on significantly increasing supply, which is a slow moving factor. So for now, all indications are that the fervent growth in property values will continue throughout the summer at least."

Investment demand and limited supply have been key factors lifting the Kiwi housing market, although so too has a robust domestic economy that has been spared from the same extent of disruption at the hands of the coronavirus that has been seen elsewhere and most recently in Europe, where major economies are again in 'lockdown'.

Source: CoreLogic NZ.

Superior containment of the coronavirus has led restrictions on activity to be eased in a sustained way in New Zealand, enabling the economy to begin clawing back lost output while lessening the need for additional support from the RBNZ, which began to back away in November from the verge of implementing a negative interest rate policy.

"The NZD should benefit from a friendlier global trade environment in 2021. As such, the NZD/USD appreciation is catching up with local commodity prices, and the gap will be bridged should the exchange rate reach the region of 75 cents," says Kit Juckes, chief FX strategist at Societe Generale.

The RBNZ's tempering of its guidance on the interest rate outlook has lifted the Kiwi sharply in recent months, although it's appetite for the U.S. Dollar that's likely to have the greatest influence on the trajectory of the New Zealand Dollar into the mid-week session.

The U.S. Dollar's performance is in turn hinged substantially on the outcome of a runoff election in the state of Georgia Tuesday where control over Congress will be decided through votes for two Senate seats. If Democratic Party candidates are able to flip the seats then it'll likely mean more debt-funded financial support can be provided to the economy over the coming months without necessarily requiring a prolonged period of horsetrading in Congress first, which is generally seen as a risk to the U.S. Dollar.

"Success for the democrats in the Senate votes today in Georgia will therefore determine the scope of Biden’s presidency. This result will identify whether he is able to enact those policies that we might expect him to pursue given more free will and scope, many of which are thought to be USD-negative," says Charles Porter, an analyst at SGM FX.

Above: Pound-to-New Zealand Dollar rate shown at daily intervals.

NZD/USD was near three-year highs above 0.72 again on Tuesday while GBP/NZD was -0.41% lower at 1.8827 and on route back toward its mid-December lows near 1.85 after the UK was placed back into 'lockdown' overnight in response to the new, more infectious strain of coronavirus. Coronavirus developments have ensured that Sterling got little respite after UK and EU leaders agreed terms of the future relationship last month.

"Following a pick-up in cases in late December, covid-19 trends (and associated restrictions) are once again weighing on markets. The UK is currently faring the worst – cases in England and Ireland are rising at a very rapid rate," says Imogen Bachra, a European rates strategist at Natwest Markets. "Most other Western European countries look to be past the peak of the second wave, but there are clear concerns about (a) the new, more-transmissible, virus strain and (b) a pick-up in cases following the festive period."

Speculation ahead of what is now the UK's third national shutdown ensured global markets got off to a shaky start during the first trading session of 2021 on Monday as investors weighed the disruption that it might yet cause in other countries and economies. The shutdown is expected to weigh heavily on the UK's services-dominated economy in the first quarter, following a year in which many economists expect GDP to have contracted by more than -10%.

"The double dip recession will increase pressure on the BoE to deliver further monetary easing as soon as at their next policy meeting in February. We expect speculation to build over the likelihood of the BoE introducing negative rates given the options for delivering more stimulus are becoming more limited. The developments should weigh on the pound and dampen further upside following the last minute Brexit deal," says Lee Hardman, a currency analyst at MUFG.