- GBP/NZD forecast to remain well supported

- NZ Dollar at risk of coronavirus flare-up

- Undervalued Pound to help support GBP/NZD says ANZ

Image © Pavel Ignatov, Adobe Stock

- Spot GBP/NZD rate: 2.0258, +0.08%

- Bank transfer rates (indicative): 1.9550-1.9692

- Money transfer specialist rates (indicative): 1.99-2.00 >> Find out more.

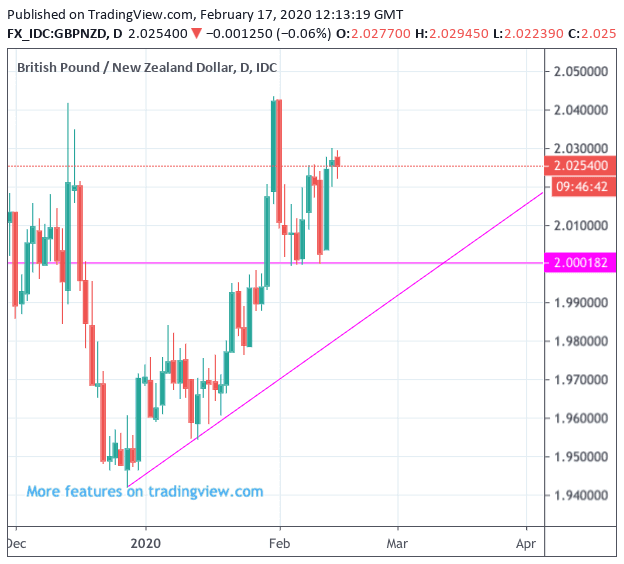

The British Pound's 2020 rally against the New Zealand Dollar is intact and the reliable bids that have been triggered by any bouts of Sterling weakness leave a number of analysts confident that further gains in the GBP/NZD exchange rate are possible.

Indeed, the setup in the charts and the broader fundamental backdrop suggests a fresh assault on the January highs at 2.04 is possible in the near-term.

The GBP/NZD exchange rate hit a high at 2.0433 at the end of January amidst some solid month-end buying interest in Sterling, however the spike higher was ultimately swiftly reversed amidst a bout of anxiety over the flavour of looming UK-EU trade negotiations and the rapid repricing in coronavirus fears in the global investor community.

Ultimately however the Pound-to-New Zealand Dollar exchange rate's sell-off failed to extend below the floor at 2.00 which confirms to us that this psychologically significant level remains the bottom of the short-term range and will likely to offer a floor to any bouts of weakness.

Buying interest has shown to increase in the 2.00 vicinity and we are therefore confident that the level will provide a spring board to any recoveries.

At present we are watching for the exchange rate to push higher and test the 2020 highs at 2.0433 once more.

Domestic Events in New Zealand this Week (Courtesy of ANZ Research)

- ANZ Monthly Inflation Gauge – January (Monday 17 February, 1:00pm).

- REINZ housing market data – January (Tuesday 18 February, 9:00am). The market has tightened, and that is expected to translate to into lifting house price inflation in the short term, though credit headwinds appear to be forming.

- GlobalDairyTrade auction (Wednesday 19 February, early am). The GDT Price Index is expected to decline by approximately 2.5% as the market deals with the uncertainties associated with COVID-19.

- Retail Trade Survey – Q4 (Monday 24 February, 10:45am). Retail sales volumes posted a strong 1.6% q/q rise in Q3. A technical retracement wouldn’t surprise.

The New Zealand Dollar's week ahead will likely largely rest on developments in China with regards to the coronavirus outbreak. China is New Zealand's largest export market and therefore a significant source of support for New Zealand Dollar demand; any slowdown in China owing to the coronavirus would therefore have a direct impact on New Zealand's economic health.

The market's assessment is that the outbreak is largely contained and that while there will be a hit to global growth in the near-term, the longer-term effects will be minimal.

The market's assessment that the outbreak is likely to be contained explains the New Zealand Dollar's relative resilience in February, and is one reason why the Reserve Bank of New Zealand (RBNZ) last week opted to keep interest rates unchanged last week while also signalling the outlook for the economy remains relatively robust.

The RBNZ also said that it was too soon to judge the effects of the coronavirus and that they were happy to adopt a wait-and-see approach to the outbreak.

While the RBNZ provided some temporary support for the NZ Dollar, we note that the currency appears to have run out of upside traction on the now established market view that the coronavirus is unlikely to be a short-term blip for the global economy. Therefore it stands that the downside risks to the currency of any flare-up in coronavirus fears could be relatively significant.

"Our initial thinking is that the impact will be a little larger and extend into Q2, with quarterly growth 0.5% pts lower than otherwise over the first half of 2020. But with COVID-19 implications still highly uncertain it’s fair to say that the RBNZ’s latest forecasts (and ours) are at risk of looking out of date pretty quickly," says Sharon Zollner, Chief Economist at ANZ Bank.

ANZ expects near-term downside risks associated with virus-related disruptions to continue to dominate market sentiment.

"The RBNZ’s sanguine assessment matched the RBA and the Fed’s tone, and while that needs to be acknowledged, market interest rates and the NZD are the natural shock absorbers and we will reprice as fresh news comes to hand. Rates will struggle to rise in this environment, and similarly, the Kiwi will be capped," says David Croy, a Strategist at ANZ.

With regards to the GBP/NZD exchange rate outlook in particular, ANZ say they expect the New Zealand Dollar to remain under pressure against Sterling, particularly in the face of market expectations for a more expansionary UK fiscal policy, "especially with the Kiwi under pressure and GBP structurally cheap".

The British Pound advanced on its global peers last week following a notable shakeup to the UK's finance ministry that could influence the scale of the country's looming fiscal expansion.

Chancellor of the Exchequer Sajid Javid resigned and was replaced by rising star Rishi Sunak. While Sunak surely is a competent replacement he is still a relative newcomer to the Cabinet, suggesting the Prime Minister will have a more malleable Chancellor when it comes to enacting his vision on spending and taxation.

Markets are sniffing a larger-than-expected boost to spending as a result of the moves.

"The fiscal floodgates are about to open – whatever brake the Treasury might have had on Number 10 has been cut entirely with this move," says Neil Wilson, Chief Market Analyst for Markets.com. "Sterling dipped initially as chancellor Sajid Javid resigned, after he refused to fire all his special advisers. The move knocked GBP/USD lower but cable ripped higher as Rishi Sunak, the chief secretary to the Treasury, was appointed in his place."

We have been reporting that increased government spending could prove to be a major source of support for Sterling in the first half of 2020 as it could provide a base for the economy heading into EU-UK trade negotiations.