Image © Adobe Stock

- GBP/NZD to resume downtrend

- Recent gains a temporary pull-back

- Pound to be impacted by 'no deal' Brexit developments, PMIs and BOE meeting

- New Zealand Dollar to be driven by Chinese data and FOMC

The Pound-to-New Zealand Dollar rate is trading at around 1.8654 at the start of the new week, 0.91% higher than the previous week.

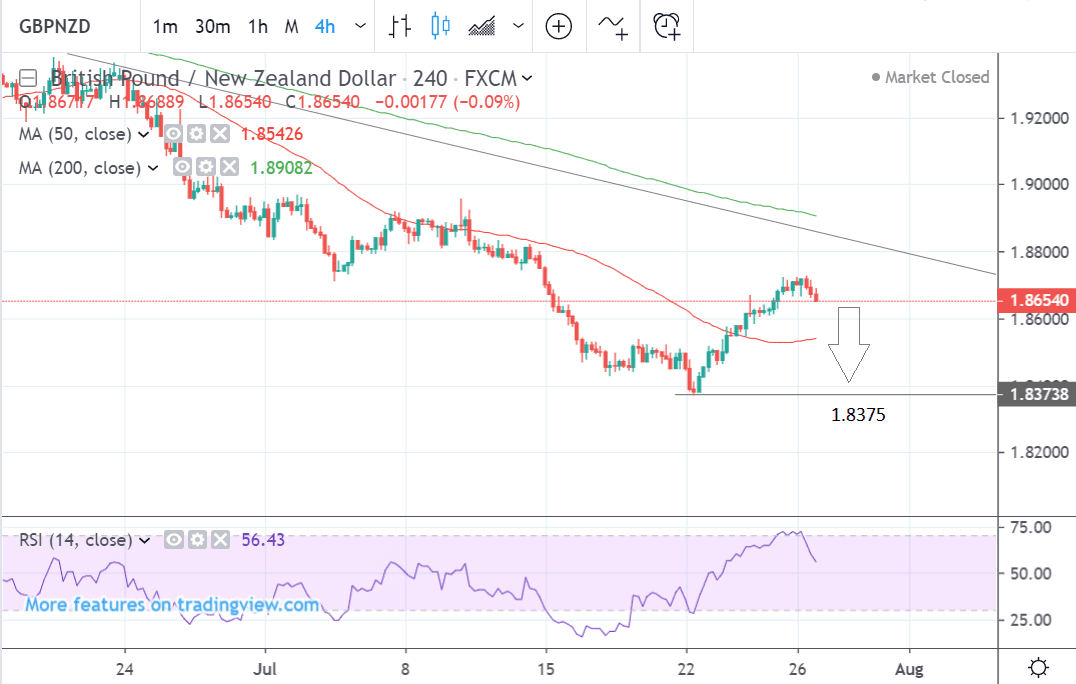

Despite the recent gains, the pair remains within the confines of a broader downtrend and this is expected to extend over the next five days.

The 4-hour chart - used to determine the short-term outlook, which includes the coming week or next 5 days - shows the pair recovering after bottoming at the July 22 lows. Nevertheless, despite the recovery, the downtrend remains intact and we expect it to continue lower in accordance with the old adage that ‘the trend is your friend’.

The RSI momentum indicator has just exited the oversold zone above 70 which is a sign to sell, and this supports our bearish forecast.

Overall, we expect the pair to work its way down to 1.8375 lows over the short-term as the dominant downtrend resumes.

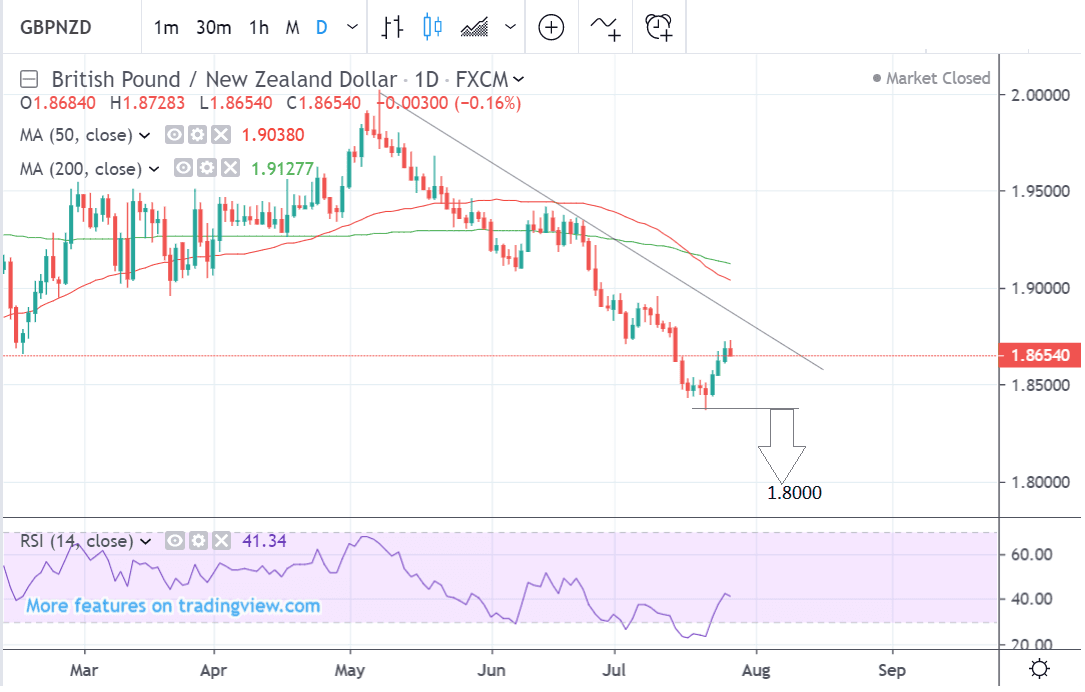

The daily chart - used to give us an indication of the outlook for the medium-term, defined as the next week to a month ahead - shows the pair is in steep decline since the beginning of May and although there has been a recovery since the July 22 lows it is not expected to endure.

A break below the 1.8375 lows would confirm a continuation down to a target at 1.8000 in the medium-term.

The weekly chart - used to give us an idea of the longer-term outlook, which includes the next few months - shows pair forming a bearish measured move pattern, which is incomplete and suggests an extension of the downtrend down to a target based on the proportions of the pattern.

The length of the final c-d leg can usually be forecast using the length of a-b, and in this case it suggests an end target of around 1.7600.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

The New Zealand Dollar: Chinese Data to Dominate

The main driver of the New Zealand Dollar in the week ahead is likely to be Chinese data where investors will be looking for signs of a pick-up in activity.

China is the largest destination for New Zealand exports and is therefore the prime source of foreign exchange earnings: the health of the Chinese economy is therefore an important factor for the NZD.

Chinese Manufacturing and Non-Manufacturing PMI data are out on Wednesday and these will provide an insight into how the Chinese economy is bearing up under current trade tensions.

Chinese PMI data provides a gauge of activity levels in different economic sectors. It is based on survey responses from purchasing managers in the companies within the sector under observation. Recently Manufacturing PMI has been poor - not just in China but most of the world - and analysts will be keen to see if the trend extends into July when data is released on Wednesday.

Chinese Manufacturing PMI is forecast to rise to 49.6 from 49.4 previously when released at 2.00 BST early on Wednesday morning.

Non-manufacturing PMI is expected to fall slightly to 54.0 from 54.2 over the same period.

"Sentiment among manufacturers likely improved. We expect the PMIs to edge higher as the impact of the US-China trade truce filters through. Also despite a weak Q2

GDP outcome, activity indicators picked up momentum in June, which likely carried through into July amid ongoing easy liquidity and phased cuts in the RRR for small and medium sized companies," says a note to clients from TD Securities.

A surprise drop in the figures would weigh on the outlook for trade, the global economy, and the Kiwi; conversely a surprise rebound would support the New Zealand Dollar.

The FOMC meeting in the U.S. may also have global implications when it is held on Wednesday at 19.00. The Federal Reserve will provide an analysis of the global economy in their statement and this could impact on the Kiwi, if it varies from market expectations, which are currently rather pessimistic. This is reflected in that fact that market-based gauges expect the Fed to make one if not two 0.25% interest rate cuts on Wednesday.

On the domestic data front, the main releases are building consents in June out at 23.45 on Monday and ANZ business confidence on Wednesday at 2.00.

The Pound: Brexit Headlines, Bank of England

Brexit sentiment is easily the most important driver of the Pound at present, and weekend headlines are unsupportive of the currency we belief.

Media reports suggest Prime Minister Boris Johnson has fully committed to a 'no deal' Brexit "by any means necessary".

The Sunday Times reports Johnson has set up a “war cabinet” to deliver Brexit “by any means necessary” by October 31 as a senior cabinet minister warned that there was “now a very real prospect” of no deal.

While markets have ramped up expectations for a 'no deal' Brexit since May, it is likely that there is further 'no deal' risk sentiment to be absorbed and therefore Sterling has the propensity to move lower and trigger fresh multi-month lows.

"Though we still see the risk of a no-deal Brexit at a fairly moderate 20%, we are bearish on Sterling over the short-term amid the expectation that Mr Johnson’s rhetoric towards the EU will remain belligerent and perhaps harden further still in the run-up to 31 October," says George Brown, an analyst at Investec.

On the calendar, the main event for the Pound next week is the Bank of England (BOE) rate meeting, since the BOE sets interest rates which are tier 1 driver of the Pound, however, in reality this may not be the case. Brexit uncertainty has paralysed the BOE and until it is resolved they are highly unlikely to take any action and all their guidance will be conditional on ‘a smooth Brexit’.

"Another possible trigger for sterling could be next Thursday’s Bank of England MPC decision, which is set to be accompanied by the quarterly Inflation Report. Our expectation is that the committee will vote to maintain the Bank rate at 0.75% unanimously (9-0) for the eighth meeting in succession," says Brown.

The current stance is still marginally hawkish due to upbeat wage growth and this sets the BOE apart from most of its G10 peers, with the exception of the bank of Canada. This should translate into pent up upside potential for the Pound should the UK achieve a managed Brexit.

However, as anyone who has been following developments in the new Boris Johnson administration this is far from certain. Johnson has gathered what looks increasingly like a ‘war cabinet’ of Brexiteer ministers who might be prepared to take the UK out of the EU with a 'no deal' Brexit on October 31.

“The Bank of England (BOE) continued to show a bias towards eventual tightening at its June meeting. This tightening is contingent on an eventual smooth exit from the European Union, however, an effort that has at times looked increasingly like a quixotic journey,” says Wells Fargo in a preview note on the meeting. “Inflation data have been stronger in the U.K. than in Europe, and according to the last statement “growth in unit wage costs has remained at target consistent levels.” “The U.K. economy has looked a bit more wobbly of late, particularly the manufacturing sector, which may be increasingly feeling the pressure from the factory sector struggles in continental Europe.”

The U.S. bank goes on to suggest ‘peer group pressure’ from other central banks turning increasingly dovish could be a further incentive for the BOE to turn dovish itself.

They forecast an eventual BOE rate hike not coming until 2020.

Given Manufacturing could be the weak link in the economy, the spot-light may be more closely trained on UK Manufacturing PMI data for July out on Thursday morning at 9.30 BST which is expected to show a decline to 47.7 from 48.0 previously.

A deeper-than-expected lapse as seen in European figures last week could spark weakness in the Pound, as it could be seen as the crack which could open up a wider slowdown.

* Advertisement