© Naru Edom, Adobe Stock

- NZD seen limping through 2019 by Morgan Stanley, J.P. Morgan.

- NZD/USD to languish at multi-year lows, as GBP/NZD rises by 8%.

- As RBNZ cuts interest rates again and markets eye further moves.

The New Zealand Dollar will underperform all its G10 rivals other than the U.S. Dollar in 2019, according to forecasts from Morgan Stanley and J.P. Morgan, as domestic and international pressures conspire against the Kiwi unit.

The Antipodean currency is expected to suffer broadly over the coming months, enabling the Pound-to-Kiwi rate to rise by more than 8%, after the Reserve Bank of New Zealand (RBNZ) cut its interest rate last week in a move that many saw as marking the beginning of an 'easing cycle'.

New Zealand's main interest rate now sits at a new record low of 1.5%. That's in line with Australia's rate and still joint-second highest in the G10 universe, but markets are betting heavily that another rate cut could come before year-end.

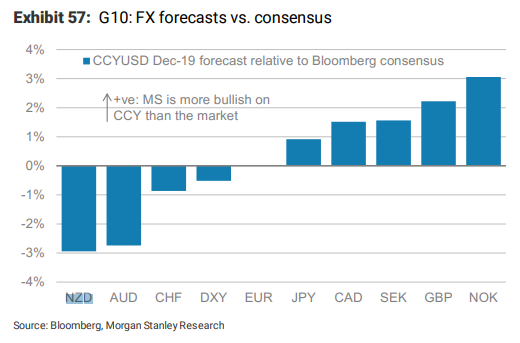

"The RBNZ has shifted to a proactive easing stance and is arguably the most dovish central bank in G10, which suggests increased sensitivity of NZD to weak domestic and foreign data given the low bar to future rate cuts, making it difficult for NZD to rally," writes Hans Redeker, Morgan's head of FX strategy.

May's rate cut came after a multi-year period in which Kiwi inflation has undershot the midpoint of the RBNZ's 1%-to-3% target. Conventional economic thinking states that higher inflation requires faster economic growth, which means lower borrowing costs might be necessary.

Interest rate decisions influence international capital flows, which tend to move in the direction of the most advantageous or improving relative-returns, and are a lure for short-term speculators.

Another interest rate cut from the RBNZ would further reduce Kiwi bond yields, which represent the return earned by investors in New Zealand government debt, and at a time when yields on some other countries bonds are expected to eventually move higher.

"The RBNZ's expected decision on raising banks' capital buffers in 3Q19 may also cause concerns about growth and fuel expectations of rate cuts, pushing yield differentials against NZD," Redeker adds, in Morgan's mid-year outlook.

Above: Total expected 2019 return for New Zealand Dollar ad G10 rivals. Source: Morgan Stanley.

Redeker is concerned about the RBNZ's looming decision over whether to radically increase the amount of money that domestic banks must keep in reserve for dark days, which is expected before the end of September.

The RBNZ plans to almost double the amount of equity capital that lenders need to hold. It's own estimates show that such a move could wipe out around 70% of the affected banks' profits over the course of a five-year period.

Analysts including Redeker have flagged that such a policy could lead to a reduction in bank lending and slower growth for the economy, which would further undermine already-weak Kiwi inflation pressures and potentially demand further reductions to the cash rate.

"Given the weak USD environment expected in 2H19NZDUSD is likely to trade sideways this year in the 0.65-0.66 range. Against all other G10 currencies including AUD, though, NZD should underperform," Redeker says.

Redeker forecasts the NZD/USD rate will end the year at 0.66 and the Pound-to-New-Zealand-Dollar rate will rise by more than 8% to 2.12 the curtain closes on 2019. He's not alone in looking for a dire performance from the Kiwi either.

Above: Pound-to-New-Zealand-Dollar rate shown at daily intervals.

"While both NZD/USD and local rates were conflicted on the message regarding path from here, we remain confident that further easing is likely. Both the staff forecasts and the Governor’s guidance include an easing bias, one that is as firm as could be expected in the absence of a commitment to cut again at the very next meeting. We expect another cut to come in November," says Sally Auld, chief economist for Australia and New Zealand at J.P. Morgan.

Financial markets briefly convinced themselves last week that another rate cut might not emerge from the RBNZ for quite some time, given what was seen as a mixed message in the bank's policy statement.

However, with the RBNZ bank capital decision looming and President Donald Trump on the trade warpath with China again, the market's optimism about the rate outlook didn't last for long.

Pricing in the overnight-index-swap market implied on Wednesday, an RBNZ cash rate of 1.31% for November 13, which is almost an entire -25 basis point rate cut below the current cash rate.

"While the RBNZ may be in for a brief pause, the months ahead still will provide plenty of oxygen for those arguing the neutral rate is falling. The consultation period for the RBNZ’s Bank Capital Review has ended, and the final decision will be announced in 3Q," Auld says.

Above: NZD/USD rate shown at daily intervals.

Auld cites other estimates that suggest Kiwi commercial banks will need to lift variable mortgage rates by as much as 0.5% in order to ensure that shareholders' profits are not wiped out by the regulation changes.

However, that would amount to a de facto RBNZ rate hike for many Kiwi households and could necessitate a response from the bank.

It's not yet clear whether the second rate cut that markets are betting on represents investors' expectation of that response, or if they'll bet on an even steeper cut once the decision is known.

Auld says this RBNZ policy outlook should ensure the NZD/USD rate declines to 0.65 before year-end and the Pound-to-New-Zealand-Dollar rate rises to 2.09, both of which are just beneath Morgan Stanley's forecasts.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement