Image © Adobe Stock

- GBP/NZD seen rising as trend continues

- Break above highs required for confirmation

- Politics to drive Sterling; for the Kiwi China data

The Pound-to-New Zealand Dollar rate is to start the new week from 1.8870, only marginally lower than the previous week's open, after the New Zealand Dollar recovered following a sudden devaluation during last week's flash crash, caused by fears about a slowdown in China.

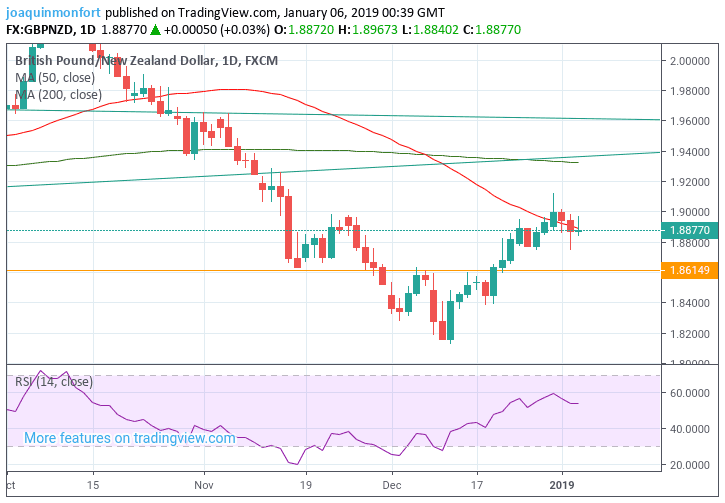

GBP/NZD is nevertheless in a short-term uptrend which started at the early December lows and this is expected to continue in the week ahead. Although the pair pulled back after touching the 50-day moving average (MA) situated at the 1.8890 level, the short-term uptrend remains intact and therefore biased to extend.

A break above the 1.9120 December 31 highs would provide confirmation of a continuation up to the next upside target at circa 1.9290 and the level of the 50-week moving average (MA).

The RSI momentum indicator in the lower pane is relatively high and suggestive of 'pent-up’ upside potential. It is at the same level it was at when the exchange rate was above 2.04 back in October.

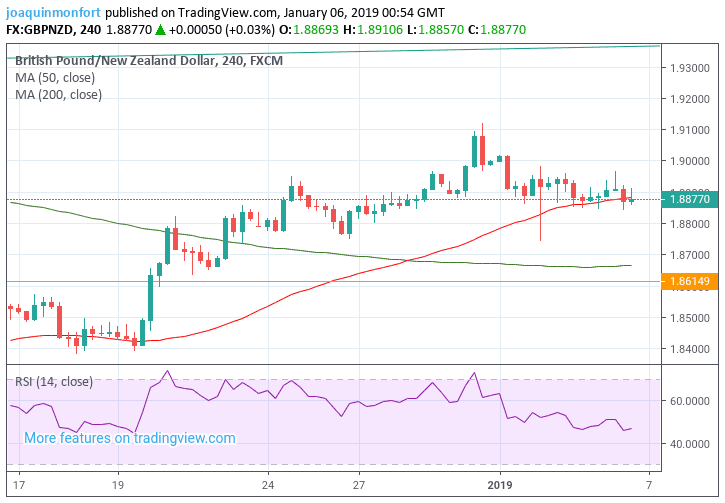

The four-hour chart shows a pullback from the end of year highs in more detail. It is looking quite bullish after forming a hammer candlestick on January 2. This rather long hammer indicates more probable upside on the horizon eventually once the pair starts rising and adds further evidence to support our bullish stance.

Advertisement

Bank-beating exchange rates. Get up to 3-5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The New Zealand Dollar: What to Watch this Week

With no major data releases coming out of New Zealand, the next most important class of data for the New Zealand Dollar is Chinese data, since China is the country's largest trading neighbour.

Chinese inflation data out on Thursday, may impact on the currency. It is expected to fall in December as the economy cools. A greater-than-expected decline, however, would be extremely detrimental to the New Zealand currency.

“China's producer price index (PPI) is expected to have moderated further in December to an annual rate of 1.6% highlighting further the weakening factory demand for raw materials,” says Raffi Boyadjian, an analyst at broker XM.com.

If he is right, a negative result could add further headwinds to the Kiwi, which exports considerable volumes of dairy products for China's growing affluent middle class. Another major export are soft commodities like wood.

A fall in demand would hit the Kiwi as China has to pay for these NZ imports using New Zealand Dollars thus slacker demand would lead to a fall in demand for the currency as well, resulting in a devaluation of the Kiwi.

The Pound: What to Watch

The UK enters a critical three week period as parliamentarians return to Westminster to debate the merits of the Government's withdrawal deal with the EU. A vote is due in the week commencing January 14.

At present, the deal is expected to be voted down by legislators amidst a lack of fresh concessions from the EU. The government is expected to bring the deal back before parliament for a second vote in the event of the first vote failing.

However, any second vote must contain some material changes, so we expect the EU to offer something in the near future as they will know only too well that the deal they worked on over the past 2 years will not pass in its current form.

Sterling will likely trade relatively subdued, range-bound levels until the point it becomes clear that either 1) May's deal will pass or 2) a No Deal Brexit is going to happen in March 2019. We will be watching the newswires for any indications that a decisive shift in either direction has occurred.

The Pound's rise on Friday was in part driven by the release of better-than-expected services sector data, but in the week ahead the focus will be more on the heavier parts of the economy with industrial and manufacturing production data for November scheduled for release, as well as, of course, GDP.

Industrial production is forecast to end a 3- month losing streak in November, when it is released at 10.30 GMT, on Friday, and forecast to show a 0.2% rise. Manufacturing is forecast to show a 0.4% gain when it is released at the same time: these would contrast with -0.6% and -0.9% respectively in October.

Monthly GDP data for November is also out at the same time on Friday and is expected to show a 0.1% rise month-on-month, the same as it did in October, and a 1.3% rise year-on-year.

Despite growth in the UK being weak, it remains about the same as in the Eurozone.

“Despite the Brexit gloom and gridlock in Parliament over the withdrawal deal, the UK economy does not seem to have slowed down anymore than its European counterparts and probably managed growth of 0.1% in November, estimates are anticipated to show.” Says Rafi Boyadjian, an analyst at broker XM.com.

The other key economic release for the Pound is trade balance data, also out on Friday.

Advertisement

Bank-beating exchange rates. Get up to 3-5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here