Image © Pavel Ignatov, Adobe Stock.

- GBP/NZD probably in a new short-term uptrend

- Break above the 50-day MA for confirmation

- Main release for Sterling PMI data; for NZD Chinese manufacturing

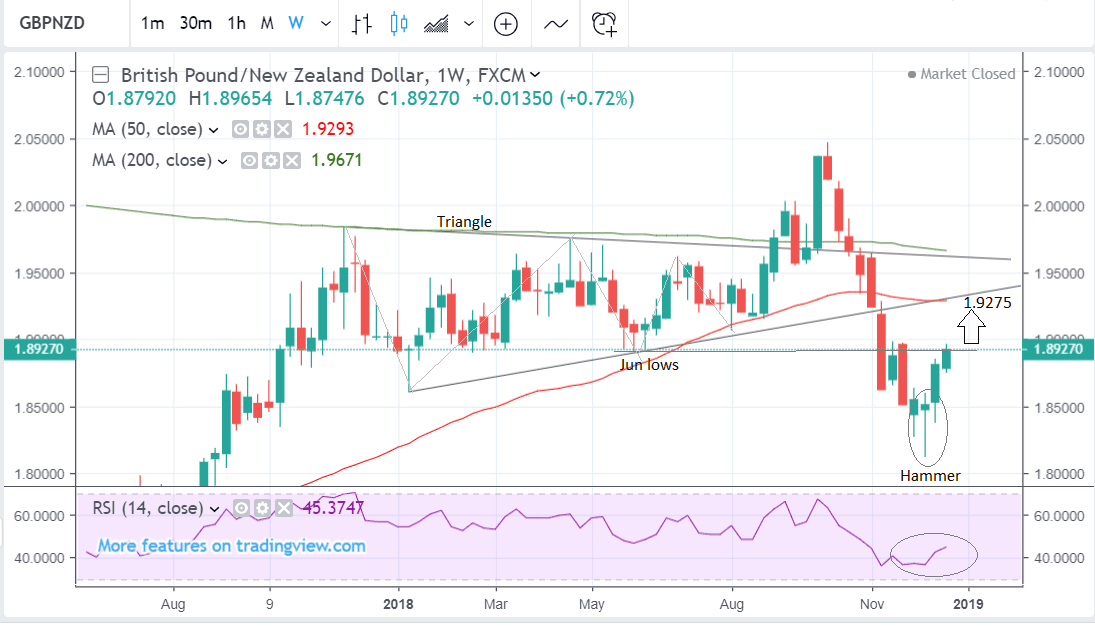

The Pound to-New Zealand Dollar rate starts the new week at 1.8927 having risen over 0.7% in the previous week.

After relentlessly falling since the early October highs, the GBP/NZD stopped and reversed at the 1.81 lows three weeks ago, after forming a 'hammer' pattern and rising strongly in the subsequent week.

Despite the strong bounce, it is unclear to read from the weekly chart whether the pair has reversed trend or not over a longer-term horizon and the downtrend from the 2.04 highs still looks quite intact.

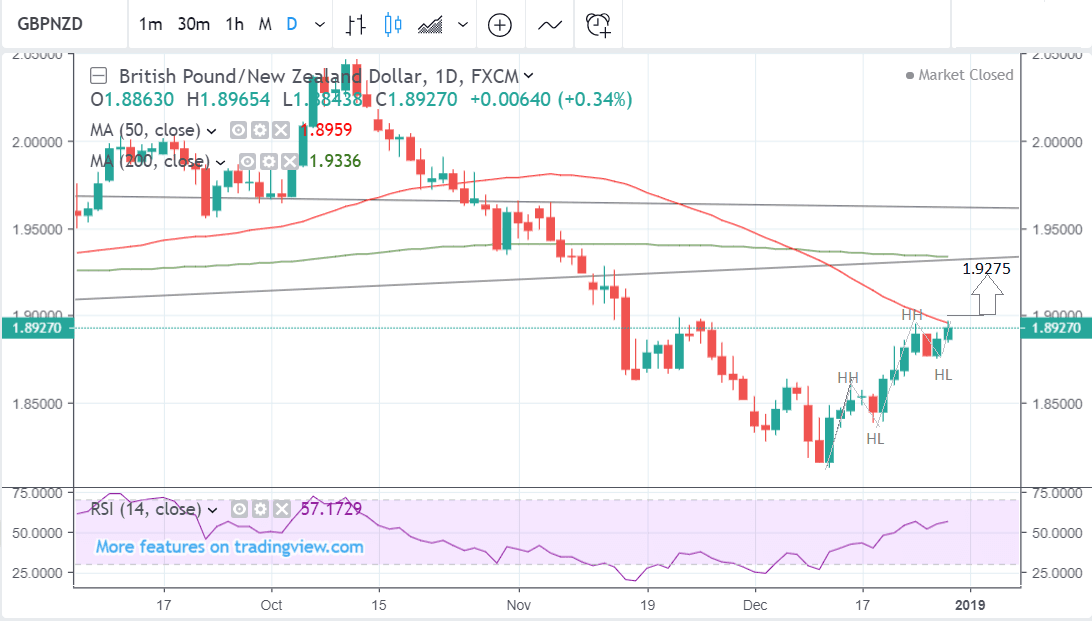

The daily chart, which gives shorter-term clues, is however less ambiguous. The recovery from the early December lows now looks to have evolved a new sequence of peaks and troughs higher. The establishment of two higher highs (HH) and higher lows (HL) is the first strong sign the exchange rate is changing trend.

The 50-day moving average (MA) at 1.8979 is an impediment to progress higher as large MA’s often present dynamic levels of resistance to the dominant trend, but it will probably be superseded.

Still, GBP/NZD would have to break clearly above the MA to increase expectation of an extension of the bounce. This would require a break above 1.9075 for confirmation, but assuming that would probably see a move up to a target at 1.9275.

Momentum is exceptionally bullish, further supporting the upside bias. On the daily chart it is currently at levels where it was when the exchange rate traded at its 2.04 highs in October.

Those watching Sterling and the New Zealand Dollar with the intention of making a payment in the future should note that while the interbank exchange rate is at 1.8927 the rate offered by high-street banks lies between 1.8260 and 1.8396, however independent providers are seen offering rate closer to the market between 1.8755 and 1.8830.

The New Zealand Dollar: What to Watch this Week

The main economic release for NZD in the week ahead is the Global Dairy Trade Index (GDT) out on Tuesday at 14.30 GMT. The GDT provides details of price changes seen at the fortnightly global dairy auction.

Dairy products are New Zealand's key export so a rise in prices tends to be supportive of the Kiwi currency. This is especially true for whole milk powder.

Milk prices have fallen steadily this year but at the auction two weeks ago they rose 1.7%. Kiwi farmers and the economy have been hurt by lower prices, and if the data out on Tuesday confirms further price weakness it could impact negatively on the Kiwi.

Also important for the New Zealand Dollar is Chinese data given the Kiwi’s sensitivity to the economic health of its largest trading neighbour.

China NBS manufacturing and non-manufacturing PMI is out at 1.00 GMT on Monday, December 31. The former is forecast to show a fall of a basis point to 49.9 from 50.0 in December. A move below the key 50 threshold would be a sign of contraction rather than expansion and would be negative for NZD.

Another gauge of Chinese manufacturing, the Caixin PMI, is out on Wednesday at 1.45 and is forecast to show a fall to 50.1 in December, from 50.2 in the previous month.

The Pound What to Watch this Week

The main release for Sterling in the week ahead is probably key sector PMI data for December.

The first sector data scheduled for release is Manufacturing PMI out at 9.30 GMT, on Wednesday, January 2. This is forecast to show a slowdown in manufacturing activity to 52.5 from 53.1. A greater-than-expected slowdown would be bad for the Pound.

Next comes Construction PMI on Thursday at the same time. This is forecast to show a slight fall to 52.9 from 53.4 in December.

Finally, Services PMI is out on Friday at 9.30 and is forecast to show a rise to 50.7 from 50.4. Services is the largest sector in the UK and, thus, is probably the most important of the three. Just like in the case of Manufacturing, a greater-than-expected slowdown would be detrimental for the Pound.

The rest of the data from the UK is unlikely to move the Pound much. Nationwide house prices are out at 7.00 on Friday when they are expected to show a 0.1% rise in December from the previous month.

Consumer credit and mortgage lending data is also out on Friday at 9.30. Consumer Credit is expected to show a rise to £0.95bn in November from £0.9bn in October. Mortgage lending is forecast to fall from £4.1bn to £4.0bn, month-on-month in November.

Brexit headlines are also likely to drive Sterling in the week ahead, although given Parliament is in recess their importance may be more circumstantial than key.

Those looking to lock in a good GBP/NZD exchange rate ahead of a potentially volatile month and year should do so over coming days as we expect volatility to be relatively low ahead of the key Brexit vote mid-month. If you lock in an exchange rate for a major international payment you can set aside any concerns on what this volatility might deliver, find out more here.

Marshall Gittler, a market veteran and currently strategist with ACLS Global says January tends to be the most volatile time of the year in the FX market.

"That’s probably because investors who’ve wound down their activity ahead of the year-end book closing rush in to take new positions. Many hedge funds traders for example basically step back from the markets in early December so as not to jeopardize their bonuses for the year. Then in January they start up with a vengance, taking positions that they hope will net them profits over the year," says Gittler.