© Natanael Ginting, Adobe Stock

- INR wobbles as row between government and central bank escalates.

- Clean-up of bad loans, borrowing costs and lending at centre of dispute.

- Government interference risks a Turkish Lira-style crisis for the Rupee.

The Reserve Bank of India's (RBI) independence is under threat from government intervention in the affairs of the bank and so too is the Rupee, because political meddling in the machinations of India's monetary policy machine could risk creating a Turkish Lira-style crisis.

Indian press has been awash with headlines about an ongoing row between the Reserve Bank's board and its political masters in New Delhi.

The fracas started Friday when deputy governor Viral Acharya gave a speech at the A. D. Shroff Memorial Trust in which he evoked imagery of repeated financial crises in Argentina during an open lecture to the government on the apparent perils of actions that compromise the independence of central banks.

"Governments that do not respect central bank independence will sooner or later incur the wrath of financial markets, ignite economic fire, and come to rue the day they undermined an important regulatory institution; their wiser counterparts who invest in central bank independence will enjoy lower costs of borrowing, the love of international investors, and longer life spans," Acharya said.

It transpires the Indian government has in fact shown signs it is contemplating a direct intervention in the bank's affairs over some of its recent policy decisions. It is reported to have written several letters seeking consultation with the bank's governor over its "Prompt Corrective Action (PCA) framework" for cleaning up bad loans in the financial sector.

Financial markets, particularly bond and currency markets, have a severe aversion to political meddling in the affairs of central banks given the risk that politically-motivated decisions can pose to creditors of sovereign governments.

Governments can easily be tempted to pressure central banks into keeping interest rates low for electoral reasons, but this kind of decision almost always gives rise to market fears over the inflation outlook.

After all, benchmark interest rates are the primary tool for managing inflation in the modern economy. When rates are kept too low for too long, inflation rises and eats into the returns of money lenders. This leads creditors to demand even higher rates than they otherwise would have when lending to governments.

Not only does that make some government functions and public services more costly to run, it can also dent the economy if a funding squeeze leads projects to be abandoned, and if any spillover into commercial interest rates leads private companies to do the same.

Above: U.S. Dollar and Turkish Lira exchange rate at height of Turkish crisis.

The 2018 crisis in Turkey, which saw the Lira depreciate by as much as 60% at one point, demonstrates just how bad things can get for a country when government officials come through the back door to appoint themselves as de facto heads of a central bank.

"Rumours are now circulating that Governor Urjit Patel is considering resigning in protest," says Shilan Shah, an economist at Capital Economics. "We can’t claim to have any special insight about whether Governor Patel will call it quits. But what is clear is that the government’s comments and actions risk eroding the independence of the RBI which, over recent years, has been one of India’s more credible institutions."

Finance Minister Arun Jaitley criticised the RBI on Tuesday for failing to prevent a build-up of bad loans in the Indian banking sector, saying it looked the other way as firms chased growth by lending without sufficient regard to borrowers' ability to repay. Some of those defaulted loans sit on the balance sheets of state-owned banks.

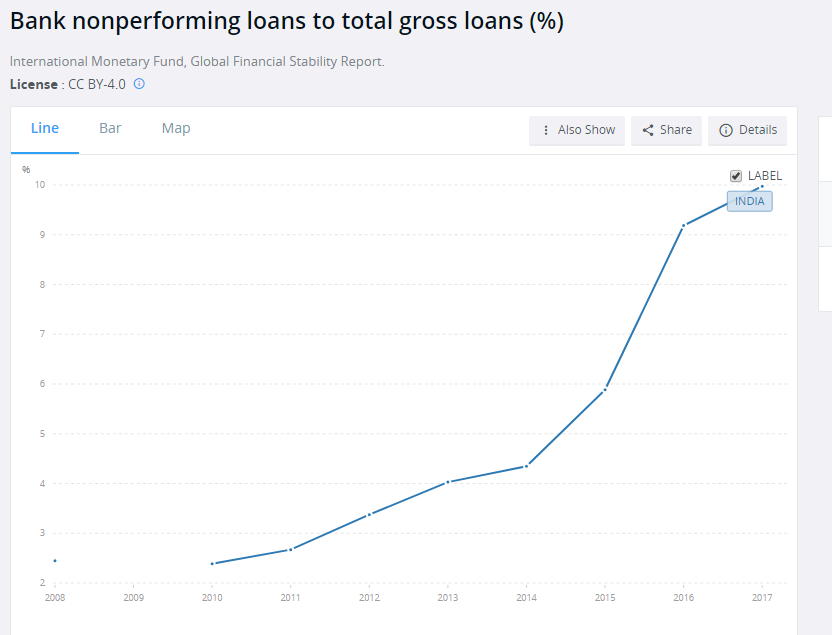

World Bank data shows Indian non-performing loans more than tripled to 10% of all banking system assets between 2009 and 2017. This compares poorly against a world average of 3.74% and an Organization for Economic Cooperation and Development (OECD) average of 2.66%.

Above: World Bank graph showing Indian non-performing loan ratio.

India's Infrastructure Leasing & Financing Services (IL&FS) Group, a large provider of non-bank finance to companies, defaulted on some its debts in September. This has seen market borrowing costs for many non-bank finance providers rise in recent weeks, crimping companies' ability to raise capital and risking economic growth ahead of an election year.

However, and in a sign of the RBI's current predicament, the finance ministry is also criticising the RBI for being what they suggest is too heavy-handed with it efforts to fix the loan problem, through its PCA framework. This restricts the financing and commercial activities of troubled banks, in the name of financial stability.

Presumably, those government ministers fear that a clampdown on "shadow bank" lending will slow economic growth going into 2019, and elections are due to be held there before May, which will place the government's stewardship of the economy and financial system under a spotlight.

These are two contradictory criticisms that are being levelled at the bank, likely motivated by political concerns ahead of elections due to be held in 2019. The RBI has already hiked interest rates twice in 2018, raising borrowing costs for all.

"The stakes are high. After all, inflation expectations have dropped to single digits for a sustained period for the first time since 2009," says Capital Economics' Shah. "Any erosion of independence could permanently reverse this long-term drop in inflation expectations, affecting spending and saving decisions and wage negotiations and ultimately pushing up actual inflation."

For its part, the Indian government said Wednesday that the autonomy of the central bank is "an essential and accepted governance requirement", but then doubled down on its recent foray into the machinations of bank policy, according to The Economic Times.

The USD/INR rate was quoted 0.40% higher at 73.94 Wednesday, denoting a stronger Dollar and weaker Rupee, and has now risen by 15.8% in 2018.

The Pound-to-Rupee rate was 0.84% higher at 94.37 and has gained 9.5% this year.

Advertisement

Bank-beating exchange rates! Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here