Data on trade positioning from major financial institutions reveals sentiment towards the British Pound continues to improve which in turns suggests the potential for further gains over coming weeks and months.

How the global foreign exchange rate markets are positioned on a currency is typically indicative of which way it is likely to move: when traders are overall 'long' on a currency it suggests they believe it will rise.

When they are 'short' they believe it will fall. It will come as no surprise to readers that since the Brexit referendum of June 2016 sentiment towards Sterling has fallen in the 'short' category.

This sentiment has corresponded with double-digit declines in the value of Sterling which saw the Pound-to-Dollar exchange rate fall into the 1.20's region and the Pound-to-Euro exchange rate fall into the 1.08's.

However, data on trader sentiment now appears to be turning in such a way that would suggest a recent recover in Sterling could be building a head of steam.

Traders Might be Favouring Sterling Again

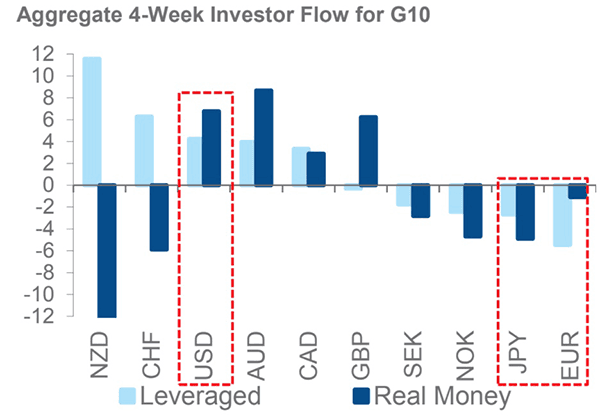

Analysts at global investment banking giant Morgan Stanley say their in-house models show GBP positioning increased to long in the final weeks of December.

"There was broad-based GBP buying across all investors captured in our positioning tracker. GBP was one of the only two currencies bought by non-commercial IMM accounts in the three weeks to December 26," says Strategist Gek Teng Khoo at Morgan Stanley in London.

Khoo say this trend was led by asset managers buying to become mostly 'long' on the British Pound for the first time since June 2016, while leveraged funds were small sellers.

"GBP was also the only currency bought by Japanese retail accounts in the last three weeks of December, and the only currency where sentiment is bullish. Global macro funds were also GBP buyers. While bullish sentiment has not reached extreme levels yet, long positioning could be a risk if sentiment turns around," says Khoo.

The data is revealed by Morgan Stanley's FX Position Tracker which monitors sentiment amongst traders in the global currency trading community.

![]()

It combines a host of available data points on sentiment amongst traders in the global currency sphere; including the IMM Commitment of Traders Report, the Toshin, TFX and internal measures of ETF flows and internal sentiment monitors.

Meanwhile, a report from Citi - the world's largest dealer of foreign exchange - echoes the findings of Morgan Stanley.

Citi report "the strongest hedge fund flow in the final week of 2017 was NZD, GBP and JPY buying and AUD and USD selling, in a reversal of previous weeks."

Above (C) Citi

Currency traders might not necessarily be turning positive on Sterling however.

As noted by analyst Viraj Patel with ING, we could be witnessing a situation whereby traders are merely exiting negative 'short' bets against Sterling; such a move would logically shift the market's stance into a more friendly one for the currency.

"While speculative investors have turned net long in recent months, this adjustment in positioning has been mainly driven by GBP shorts bailing – which suggests to us that the attractiveness of selling GBP has been fading given the absence of any factor that could seriously delay Brexit talks and push the U.K. closer towards the March 2019 cliff-edge," says Patel in a note dated January 3.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Strategists Position for Gains in the Pound

Evidence of a more constructive stance on Sterling in global currency markets gels with the views of a number of strategists we follow who have told clients to prepare for Sterling gains in 2018.

The Pound is still expected to be a politically-inspired currency over coming months - in keeping with trends in place since the June 2016 E.U. membership referendum - but the outlook is deemed to be brighter.

Analysts at Danske Bank have recommended clients buy the Pound against the Euro, saying "the Brexit issue is set to remain the main driver for GBP in 2018 and while uncertainty and fundamentals justify an undervalued GBP for now, we see prospects of a recovery in 2018 as clarification on Brexit increases."

Progress made by the E.U. and U.K. on the so-called 'divorce terms' of Brexit means negotiations in 2018 will firstly focus on the shape of a transitional that will cover the period between the exit date and the final Brexit state.

Sterling has in the past shown it likes talk of a transitional state that reflects the current status quo; and should this be confirmed in the opening months of 2018 the Pound could well go higher.

"This should eventually bring investors back to GBP assets due to attractive valuations," say Danske Bank in their note to clients. "What matters for GBP is the future E.U. - U.K. relationship and, not least, reassurance that it can avoid a ‘cliff-edge Brexit’, where there is no deal and no plan when the current 2Y negotiation window ends and the UK formally leaves the EU."

Meanwhile, ING's Patel says he believes Sterling is likely to rise against both the Dollar and Euro in the first quarter of 2018 as politics surrounding Brexit negotiations become less threatening.

Indeed, Patel reckons the U.K. and E.U. should agree a Brexit transitional deal within the first half of 2018.

"We prefer to focus on potential catalysts for a positive reassessment of the UK economic cycle and a hawkish re-pricing of BoE policy expectations. We cite 2 non-mutually exclusive factors – an agreed Brexit transition deal by 1Q18 and positive surprises in UK economic data," says Patel.

ING's conviction call is for GBP/USD to rally up to 1.40 on this story, with EUR/GBP moving to 0.85-0.86.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Sterling Supported by Better-than-Forecast Services Sector Data

Pound Sterling was seen trading at near-unchanged levels in the wake of the release of Services PMI data from IHS Markit and the CIPS.

Accounting for in excess of 80% of U.K. economic activity, the release tends to impact direction in Sterling whenever it surprises against analyst expectations.

The problem for those hoping for volatility is that the data came in more-or-less in line with economist expectations - analysts were forecasting a reading of 54.1 for the month of December, a tick up on November's 53.8.

The confirmed reading was for 54.2, which confirms the sector continues to grow at a decent enough clip. However, for a currency trader the beat was not enough to justify a fresh bid on Sterling.

At the time of writing the Pound-to-Euro exchange rate is quoted at 1.1239 and the Pound-to-Dollar exchange rate at 1.3524 - both key rates are well within recent ranges.

Nevertheless, the strong reading of 54.2 confirms the U.K. economy enters the new year with decent impetus and this should underpin the Pound longer-term which reinforces those forecasts that see Sterling appreciating in the year ahead.

“The services sector experienced mixed fortunes in December, as business activity expanded at an accelerated pace but the flow of incoming new work was the slowest since August 2016," says Duncan Brock, Director of Customer Relationships at the Chartered Institute of Procurement & Supply.

Elsewhere, the Bank of England’s money and credit figures for November revealed that the number of mortgages approved for house purchase rose from 64,887 in October to 65,139, above the consensus expectation for a further fall, which had seemed likely following the decline revealed in the UK Finance measure which covers the main high-street banks, released on 27th December.

At the same time, consumer credit continued to expand at a fairly strong £1.4bn on the month.

"All in all, then, the latest data suggests that the economy maintained a decent amount of momentum in Q4, which we expect to be built upon in 2018. Indeed, our forecast is for GDP growth of 2% or so, compared to the consensus forecast of a slowdown to 1.4%," says Paul Hollingsworth, UK Economist with Capital Economics.

At the time of writing, the Pound-to-Euro exchange rate is at 1.1239 EUR while the Pound-to-Dollar exchange rate is at 1.3530.

Euro Eyes Inflation Data Ahead of the Weekend

For the single currency, all eyes will be on the release of inflation data at 10:00 GMT.

Friday, January 5 should prove to be an interesting one on global currency markets owing to the amount of data on tap.

Pound Sterling is not subject to any releases but the Euro will be exposed to the preliminary release of inflation numbers for December - in short, should inflation come in stronger than economists are expecting the Euro could well extend its recent run of good form.

Markets are positioned for a reading of 1.4% on a month-on-month basis in December, down on November's 1.5%.

This should take the annualised figure up to 1.0%.

Disappointment could well see the Euro fade into the weekend.

Inflation matters as it is a key gauge of economic performance at the European Central Bank - the ECB has for years now been trying to stimulate inflation back towards its 2.0% target by deploying a number of measures such as cutting interest rates to record-low levels and printing large sums of money.

A side-effect of this stimulatory effort has been a weaker Euro.

The ECB is betting inflation is creeping back to the 2.0% target and as such the ECB has indicated it is to start reducing stimulus, something that saw the Euro rally in 2017.

Hence, today's data should inform markets as to how effective the ECB's policies which will in turn impact on timing of ECB policy and, by extension, the Euro.

Ahead of the release, analysts with Lloyds Bank say CPI data for December is likely to show that inflation remains below the European Central Bank’s inflation target of ‘close to but below 2%’.

Already released data for some Eurozone economies, including Germany and Spain, showed a modest deceleration in annual headline inflation in December compared to November.

"We also expect the Eurozone average to have fallen to 1.3% from 1.5%. This may reinforce expectations that the ECB will continue to take a cautious approach in moving towards less stimulatory monetary policy," says Robin Wilkin, an analyst with Lloyds Bank.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.