Exchange rate strategists at Deutsche Bank do not think the British Pound’s January rally is sustainable and have given clients five reasons to expect deep losses.

The call comes as Sterling remains above multi-week lows against both the Euro and Dollar with many analysts suggesting fatigue over the Brexit argument is setting in and the Pound has seen the worst of its post-referendum decline as a result.

The Pound has essentially absorbed the downside risks associated with Brexit and until we get some fresh bad news the currency should stabilise.

Deutsche Bank however maintain a long-held view that the Pound has further to fall and have restated that view as we head through February.

In a note seen by Pound Sterling Live, analyst Oliver Harvey lays out his case for a decline to parity in the Pound to Euro exchange rate and below 1.10 in the Pound to Dollar exchange rate.

The five reasons are:

One

Brexit negotiations are not likely to start well.

The EU will probably take a hard-line stance rather than a compliant one since elections in many of the EU’s most Eurosceptic member states are taking place this year.

The EU will not want to be seen to be going easy on the UK as this might set a president for other wavering states.

Therefore, they will not want the UK to ‘have their pie and eat’ which is the definition of a good deal.

We heard from Bank of America this week that key to Sterling's outlook is the ability to secure a transitional deal as it should ensure continuity - committment to a deal that allows extended access to the single market would aid the Pound.

Deutsche Bank do however believe the news on this front won't be good; "a transitional arrangement can only be agreed once the future relationship is clarified, i.e. towards the end of the Brexit process, too late for many firms."

Two

There are unlikely to be any alternative “fall-back” options to a hard Brexit.

Deutsche think it is unrealistic to expect the UK to be able to simultaneously negotiate a successful exit from Brussels and a good deal with another large market such as the US.

The two-year deadline would be a problem for starters given trade agreements often take over 6 years to complete.

Indeed, we have heard overnight from EU Commission Vice President Jyrki Katainen that it would take a "little miracle" to get a deal signed in two years. Yet, David Davis - the UK's Brexit minister - believes it will be done.

Lack of experienced negotiators to fight a ‘war on two fronts’ would be another problem.

In addition, although Trump has made entreaties to the UK, his 20% border tax adjustment would mean the deal would be in the US’s interest more than the UK’s.

"The benefits of a US free trade deal would also be more than offset by any Trump border tax. The UK would be the worst affected by a border tax, with exports falling 35% to the US," says Harvey.

Three

The market is over-optimistic about the probability of the Bank of England (BOE) putting up interest rates in 2017.

Higher interest rates support the Pound but Deutsche’s Oliver Harvey sees it as wildly optimistic to expect the BOE to raise interest rates at all this year.

Given the Sterling has already priced in this possibility it will probably fall as the reality sets in.

The Pound is also expensive when compared with the interest rate differential between the two countries, suggesting it may ease back over time.

Four

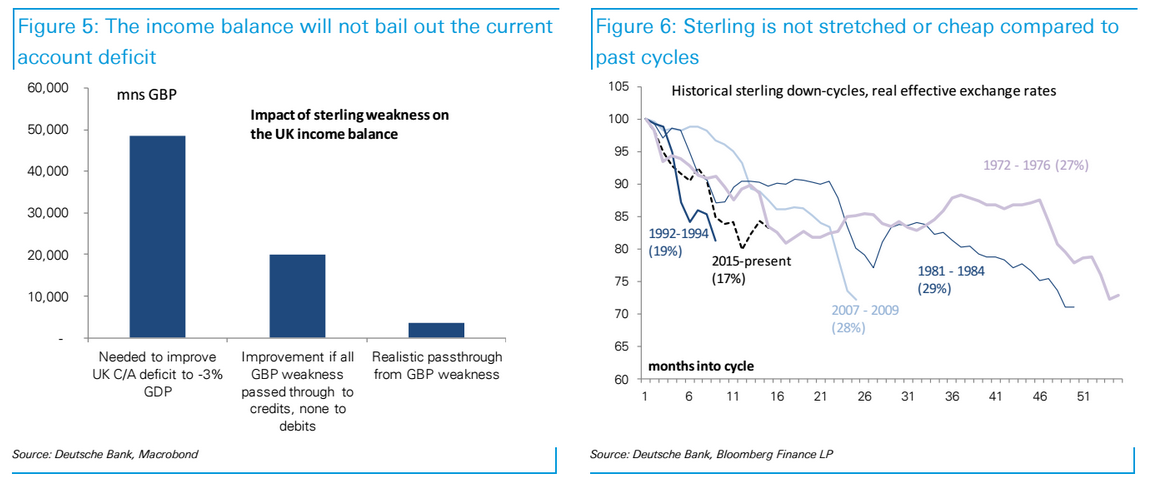

Expectations that the weak pound will help rebalance the wonky Current Account are roundly dismissed by Deutsche.

“Exports have barely responded to a weaker pound and the trade deficit has deteriorated. By contrast, pound weakness will help improve the income balance, but only on the margin,” says Harvey.

The income balance is the money sent home by UK workers abroad versus the money sent abroad by foreign workers working in the UK.

Although the income balance surplus is set to rise and support the Pound, the rise is not forecast to be significant enough to push the currency higher.

Five

Harvey argues that the Pound has scope to weaken further because it is not stretched.

“Our PPP fair value estimate of EUR/GBP is 0.85 ( vs current 0.8630), however, meaning that sterling is not cheap versus the partner with which UK trade will suffer most.

0.85 EUR/GBP equates to 1.1765 in GBP/EUR terms, while 0.8630 equates to 1.1587.

“Nor does sterling look particularly stretched relative to past cycles. On a real effective exchange rate basis, the current GBP downtrend is the smallest in recent history but not the shortest,” said Harvey.

Forecasts

Deutsche Bank's most recent FX Blueprint publication sees a deterioration in political rhetoric around Brexit as a key catalyst for further Sterling weakness.

Another catalyst is the large terms of trade shock from full exit from the Single Market.

This is consistent with GBP/USD at 1.06 and EUR/GBP close to parity respectively.