- Pound to Euro rate for reference: 1.1712, down 0.98% on the day

- Euro to Pound Sterling rate for reference: 0.8539

- Pound to Dollar rate for reference: 1.2597, down 0.64%

A poor day at the office for Pound Sterling which slid to one-week lows on a combination of falling UK gilt yields and the release of industrial and manufacturing data from the ONS which was incredibly poor.

GBP was the worst-performing currency in the G10 through the mid-week session thanks to the release of some poor economic data.

We have identified the main culprit for the decline as being the rise in UK bond prices - bonds and stock markets are all rising as a rescue deal for some of Italy's struggling banks are muted.

The rising bond prices mean yields delivered by those bonds are falling and it is the strong rise in US and UK yields since the election of Donald Trump in early November that has been the linchpin of Sterling's recent outperformance.

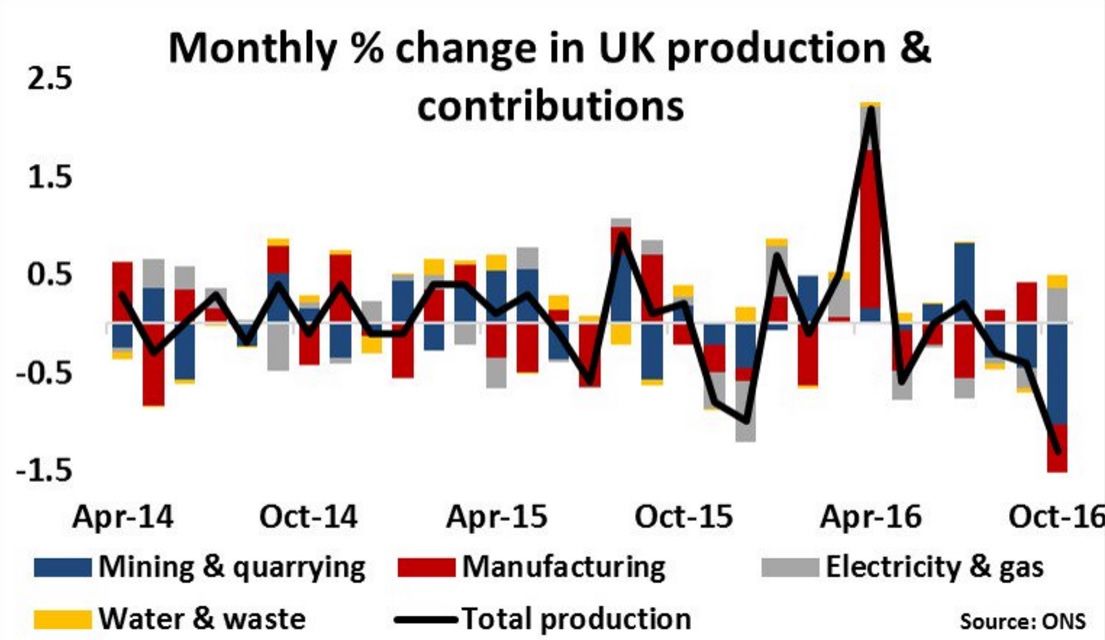

However the pressure was compounded mid-morning on news that UK manufacturing production data had fallen 0.9% on a month-on-month in October.

This is much worse than the 0.2% growth that economists were forecasting.

"Another trigger of the Pound’s decline is the UK’s disappointing manufacturing figure. The figure represents the UK’s biggest fall in output since 2012 which was partly due to the temporary shutdown of the Buzzard oil field in the North sea," says Paresh Davdra at foreign exchange brokers RationalFX.

Industrial production meanwhile slipped 1.3%, a larger decline than the +0.2% figure that was forecast.

A decline in oil & gas output contributed to some of the headline drop, shrivelling by a further 10.8% m/m and taking the cumulative decline since July to 17.8%.

Utilities and water & sewerage output provided some modest offset, expanding by 3.5% m/m and 1.8% m/m respectively.

Despite the recent improvement in manufacturing survey readings – the manufacturing PMI in September hit its highest since June 2014 and remains above its long-term average – momentum in official ‘hard’ data industrial remains distinctly underwhelming.

“Sterling’s export-supportive declines notwithstanding, an export-led boost and rebalancing away from services and the consumer still seems relatively distant on these data,” says a note from Lloyds Bank in response to the data.

Nevertheless, the recent Markit/CIPS manufacturing PMI suggests that output in the sector will bounce back in the coming months.

Latest Pound/Euro Exchange Rates

| Live: 1.1717▲ + 0.12%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1319 - 1.1365 |

**Independent Specialist | 1.1553 - 1.16 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

And mining and quarrying output should rebound as oil field maintenance comes to an end.

“But with the overall industrial sector contracting in October, industrial production will probably subtract from GDP growth in Q4, after the -0.1 percentage point contribution in Q3,” says Scott Bowman at Capital Economics.

Concerning the outlook, economist Andrzej Szczepaniak at Barclays is less optimistic and says he continues to see limited upside in industrial production and manufacturing output for the following reasons:

"First, inflationary pressures are at multi-year highs according to the latest PMI and CBI surveys. While some firms may receive an export-driven boost from GBP depreciation, the adverse impact of input prices will make things more finely-balanced; a recent EEF survey found that half of manufacturers viewed it was a risk to business rather than an opportunity.

"Further, as we enter the first half of 2017, when it is anticipated that Article 50 will be triggered, we expect firms to become more cautious in light of a lack of clarity regarding Britain’s negotiation strategy and the aimed for post-exit relationship between the UK and the EU and the rest of the world."

From a currency perspective, analyst Shaun Osborne at the Bank of Nova Scotia says traders should expect any strength in GBP from here as being temporary in nature.

The GBP/USD remains in consolidation mode but Osborne argues the failure to challenge 1.28 suggests a dip to the lower end of the upward-trending channel at 1.2435 lies ahead, "especially if intraday losses below support at 1.2640 are sustained through the close. Look to fade GBP rallies."