A solid run of PMI data for November confirms the UK economy should grow at a strong pace into year-end but there are signs that activity is slowing as cost pressures start to build.

UK Services PMI for the month of November read at 55.2, according to IHS Markit at the CIPS in a data release on Monday December 6.

This reading beat economist forecasts for 54.0 and was higher than the previous month’s 54.5.

The rate of expansion of total activity in the UK’s dominant services sector accelerated further to its strongest level since January.

This is an impressive feat considering forecasts made after the June EU referendum for the UK economy to fall into recession in the final quarter of 2016.

IHS Markit and the CIPS who compile the report say employment growth picked up to the fastest since April, partly fuelled by the sharpest build-up of outstanding work since July 2015.

This will be noted by the Bank of England as a sign that slack in the economy continues to close and suggests a pick-up in domestic inflation.

Such expectations will certainly see the Bank keep interest rates unchanged moving through 2017 which should support the Pound.

Indeed, the next move by the Bank is expected to involve an interest rate rise.

The weak Pound was reported to be a factor boosting international demand, while firms also reported marketing efforts and new products.

Several factors are bearing down on the economy which will have businesses and consumers concerned.

“The ongoing battle with currency fluctuations, a weak pound and the impact of inflation will continue to undermine company profits. Rising prices are already being passed on to consumers and this is likely to accelerate in 2017 as the full import costs of higher fuel, food, travel and labour costs make their way down the supply chain. If consumers respond by slowing their spending, the sector will have to upscale their efforts to sustain the current momentum of growth,” says David Noble, Group Chief Executive Officer at the CIPS.

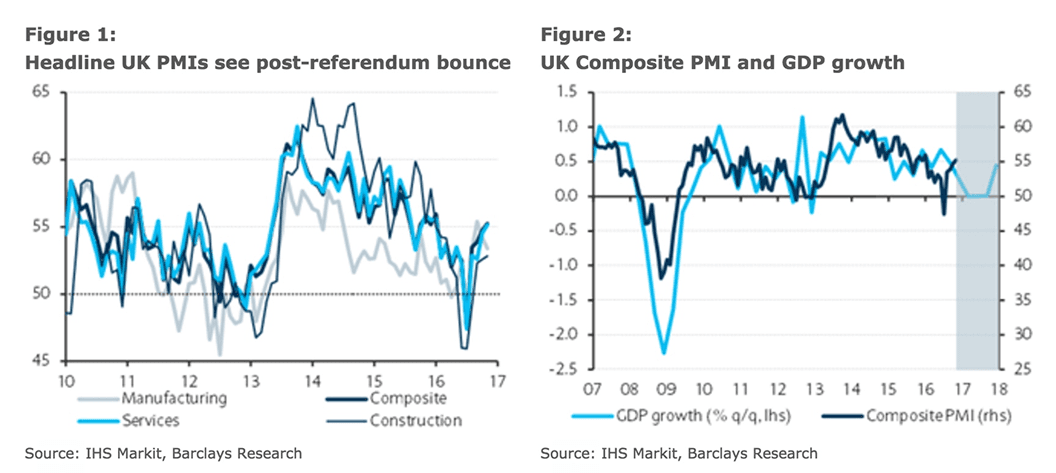

The strength in the services sector echoes the robust performance noted in the manufacturing and construction sectors.

Manufacturing PMI: Slowing, but Still Growing

The UK’s manufacturing sector continues to expand according to the November Manufacturing PMI release which came in at 53.4, down from 54.2 in October.

Rates of expansion for output and new orders both remained solid, despite growth easing further from the highs reached in September.

Underpinning the latest improvement in overall operating conditions were ongoing solid expansions of production and incoming new orders. Companies reported that domestic and export demand both remained positive growth spurs, as did new product launches, sales initiatives and efforts to clear backlogs of work.

Construction PMI: Strongest Since March

Construction PMI data read at 52.8 in November, up from 52.6 in October.

November data indicated that the UK construction sector continued to rebound from the weak patch recorded on average during the third quarter of 2016.

Business activity and incoming new work increased at the strongest pace since March, although both rates of expansion remained much softer than the peaks achieved at the start of 2014.

Greater workloads underpinned a further solid rise in employment levels and input buying among construction firms. However, average cost burdens rose sharply, with the rate of inflation the steepest since April 2011.

“November’s survey data revealed the strongest rise in overall new business volumes since March. However, lingering economic uncertainty and subdued investor sentiment meant that optimism towards the year-ahead outlook remained close to its lowest since early-2013,” says Tim Moore, Senior Economist at IHS Markit.

UK Economy Growing 0.5% in Fourth Quarter, but Nerves Over 2017 Remain

Taken alongside the manufacturing and construction PMI outturns, Monday’s reading of the services PMIs underpinned a rise in the composite index to 55.2.

“Although economic uncertainty metrics rose in November – at least as measured by some of the indicators that the Bank of England favours – it still appears likely that Q4 will post another quarter of GDP growth and could slow only mildly from the 0.5% q/q pace recorded for Q3,” reads an analysis from Lloyds Bank.

Analyst Ruth Gregory at Capital Economics agrees with the call for 0.5% growth for the fourth quarter.

“The all-sector PMI is consistent, on the basis of past form, with quarterly GDP growth of 0.5% in Q4, in line with Q3’s rate.”

Daniel Vernazza at UniCredit Bank in London says the UK economy hasn't so much as batted an eyelid at the EU referendum vote:

"Given the composite PMI averaged 51.3 in 3Q16, the PMIs suggest the fourth quarter is looking even better than the third quarter.

"And, based on the historical relationship between official GDP growth and the composite PMI, the PMI points to GDP growth of around 0.5% qoq in 4Q16. If so, it would match the growth rate in 3Q16, suggesting the economy has barely slowed following the Brexit vote. We expect growth in the region of 0.3%-0.5% qoq in 4Q."

This week’s hard activity indicators for industrial production (Wed) and construction output (Fri) will give a further steer on trends in Q4.

“With the results from all three sectors, all the signs are there for this ongoing growth to continue – at least in the short-term. But, as the risk environment becomes more challenging and volatile, with Brexit negotiations, and other socio-political events in the coming months that could influence currency fluctuations, trade agreements, the availability of jobs, and business confidence, the sector could weaken and become exposed to these challenges.”

However, analysts at Barclays note that cost pressures are starting to grow and this should temper growth moving forward.

While output remains decent, broadly in-line with its long-term average, new orders fell on the month, potentially a sign that firms are turning more cautious in light of intense inflationary pressures as input and output prices remain near multi-year highs.

"This caution is further underscored by the marked month-on-month drop in services firms’ business expectations (Figure 10), bringing it to its lowest point since December 2012 if we exclude the drop in July immediately following the EU referendum. On the whole, we believe that it will be difficult to see the recent momentum in output being sustained, particularly in face of the aforementioned inflationary pressures," says Andrzej Szczepaniak at Barclays in London.