Pound Sterling will look to extend its advance against the Euro and US Dollar this week but the outcome of the three much-watched PMI data releases will be key.

- Pound to Euro exchange rate today (2-10-16): 1.1548

- Euro to Pound Sterling exchange rate today: 0.8665

- Pound to Dollar exchange rate today: 1.2980

The UK currency outperformed both the Euro and Dollar in the week ending September 30th aided by the release of a tranche of better-than-forecast data that allowed the domestic currency to end the month on a positive footing.

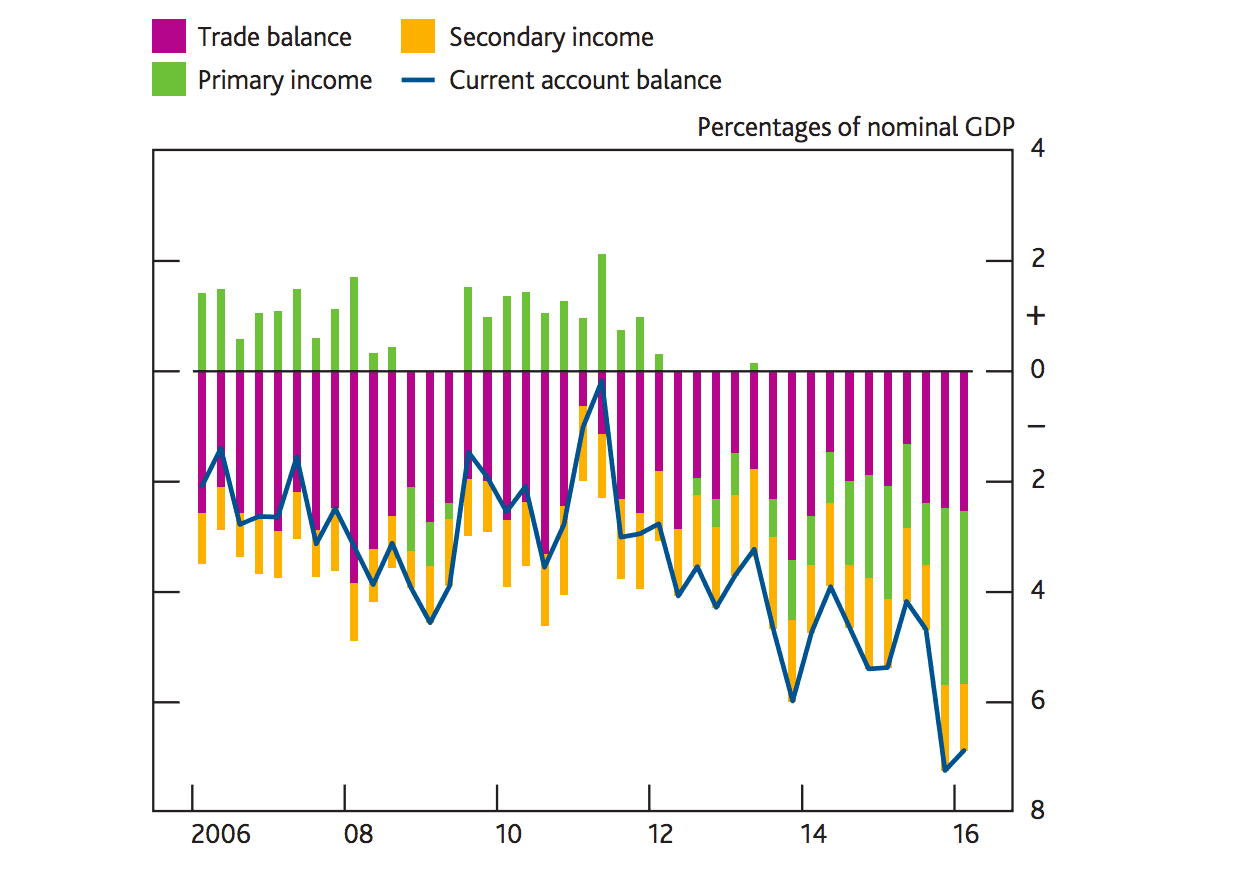

GDP, Business Investment, Index of Services and Current Account data were all released on the final day of the month.

Business Investment was shown to have increased 1% on a quarterly basis from £43.4 billion to £43.8 billion, well ahead of the 0.5% increase expected.

Yes, this is not pure post-referendum data but it does confirm a notable resillience amongst British businesses.

We have however anecdotal evidence that business investment is being delayed since the Brexit vote until some clarity as to the UK’s future relationship with the European Union is made clearer and we would expect the data to deteriorate over coming quarters.

The Bank of England have also expressed concern that delayed investment will show itself in future data releases and have used these fears to justify the interest rate cut they delivered in August.

That business investment enters the post-referendum period on such a solid footing was welcomed by currency traders who bought Sterling.

The UK’s current account deficit was £28.7 billion in Quarter 2 (April to June) 2016, up from a revised deficit of

£27.0 billion in Quarter 1 (January to March) 2016.

This is better than the £30.5BN deficit forecast by analysts and Sterling's reaction shows investors welcomed the outcome.

The widening in the current account deficit was mainly due to a widening in the deficits on trade and secondary

income, partially offset by a narrowing in the primary income deficit.

The UK’s current account deficit for Q2 was also reported and didn’t necessarily fit the pattern of better news. It revealed a deficit of 5.9% of GDP, wider than the 5.7% in Q1, clearly still large but inside the 7% of GDP at the end of 2015.

This is essentially the UK’s bank account with the rest of the world and because the UK is a net importer the country is a debtor it is in deficit.

However, inward investment flows tend to keep Pound Sterling elevated.

When these flows dry up the Pound comes under notable pressure, as has been the case this week with global investors turning nervous over the fall in the Deutsche Bank share price.

If the UK had a positive current account balance the currency would be stronger, and more stable some argue.

We will look for signs that the current account situation is improving over coming months thanks to an increase in exports.

The weaker Sterling should be playing a positive effect on export order books.

“The recent depreciation should also support exports. It will raise exporters’ profit margins, and could encourage new and existing exporters to expand production,” say the Bank of England in their August Quarterly Inflation Report.

Indeed, the Bank sees the Current Account deficit striking:

“While the current account deficit remained very wide at 6.9% of GDP in 2016 Q1, it is projected to narrow over the near term.

“That narrowing reflects both improvements to the trade balance - the nominal value of exports minus imports - and the value of net investment income flows.

“As UK residents hold more foreign currency assets than they have foreign currency liabilities, the depreciation will have increased the sterling value of the net international investment position.”

The revision to Q2 GDP saw economic growth upgraded to 0.7% from 0.6% previously.

“Sterling strengthened to its highs for the day against the Euro and the U.S. Dollar following an upward revision to second quarter GDP that showed the economy grew 0.7% from the first quarter. This highlights how the UK economy continues to show strong growth, despite lacklustre growth in the U.S. and the Eurozone," says Andy Scott at HiFX in London.

Finally, the Index of Services was touted by some analysts as being the key release.

The release came in at 0.6%, double the 0.3% forecast by economists.

The UK services sector account for over 80% of the economy, therefore developments here are critical.

"Most eye-catching news is of the rate of expansion in the services sector in July. The Index of Services for July grew by 0.4% m/m, well ahead of the consensus expectation of 0.1% m/m. There is now clear upside risk to our Q3 GDP estimate of -0.1% q/q," says Sam Hill at RBC Capital.

GBP clearly welomed this outcome.

However, HiFX's Scott warns that the currency is likely to remain under pressure but remain above key supports:

"The UK has yet to even begin it’s divorce with the EU and many uncertainties lie ahead. This is keeping Sterling under pressure and bets that it will fall further near record highs.

"We expect good support for Sterling at its post-Brexit low of 1.28 against the U.S. Dollar and 1.1450 against the Euro and that U.S. and Eurozone uncertainties will start to present some better opportunities for sellers of Sterling in the months ahead."

Chance of a November Interest Rate Cut Recedes

All the data released on September 30th will be channelled into expectations for a November interest rate cut at the Bank of England.

Whenever the prospects of such an occurance increase, the Pound falls, as was the case when BoE member Shafik told an audience this week that in her opinion further rate cuts were warranted.

Analyst Andrezj Szczepaniak at Barclays believes today's data rows the debate in the opposite direction.

"More resilient output than anticipated immediately after the referendum, coupled with August and September surveys showing improving firm and household sentiment, suggest that upside risks to our Q3 16 GDP forecast appear to be materialising.

"While we maintain our call for a cut of 20bp in the Bank Rate at the November 2016 MPC meeting, given the risks to our growth profile highlighted above, we acknowledge the likelihood of a cut decreases marginally."

That said, Barclays note we only have one month of official data, and we will have to wait until the preliminary release of Q3 16 GDP on 27 October 2016 which will comprise official data for July and August as well as ONS estimates for September before firming their call on November.

Markets Turn Notably Negative on Sterling Once More

The US Commodity Futures Trading Commission's (CFTC) much-watched data on the currency trading community shows speculative investors have added significantly to net short GBP positions (up USD2.3bn in the week).

“Net GBP shorts peaked in August but the jump in positioning suggests a significant deterioration in GBP sentiment over the past week,” says Eric Theoret at Scotiabank.

The CFTC produces market reports to provide information to industry participants and the public about the futures and options markets.

The CFTC’s latest Commitments of Traders (COT) report covers up to the 27th of September and is regarded as the best available data on market sentiment.